Главный вопрос, который волнует всех инвесторов – вызовет ли реструктуризация греческого долга срабатывание CDS.

90% всех греческих облигаций регулируется греческим законом, а 10% английским.

Греческий закон требует, чтобы все 100% инвесторов согласились с условиями, иначе будет дефолт. А это почти невозможно.

Citigroup об этом более подробно

Legal Characteristics of Greek Government bonds

After the question of whether or not a restructuring will occur and when, the next most important question for most investors is whether or not it can be done in such a way as to not trigger CDS. Lee Buchheit3 has indentified several aspects of Greek debt that are relevant. In particular, the large amount of domestic debt without features such as cross defaults and negative pledges should facilitate a number of restructuring options.

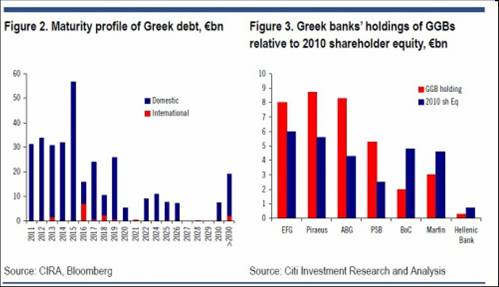

There are €327bn of outstanding Greek government bond debt, of which €9.8bn are treasury bills. Of the total, less than 2% is in dollars, yen, Swiss francs or other foreign currency. From a legal standpoint, the most striking feature is that 90% of the total bonds are governed by Greek law with the majority of the remainder under English law. Figure 2 illustrates that a large portion of the international debt is only due after 2016. These factors have significant implications for Greece’s options if they decide to go down the restructuring route.

Greek law bonds have no Collective Action Clauses (CACs) which mean that voluntary restructurings require 100% of investors to accept the new terms in order to avoid triggering a default, an almost impossible hurdle. Greek sovereign bonds issued under English law prior to 2004 have CACs which permit 66% of bondholders consent to modify terms that would bind all holders. Post 2004 75% of bondholders consent is required but the scope of potential revisions is broader.

The situation is similar for negative pledges which are only found in English law debt. The clause requires Greece equally and ratably to secure each of the bond issues if ever it creates a security interest over its revenues, properties or assets to secure any external indebtedness. This is normally applied to foreign currency borrowings and only really makes sense prior to Greece joining the Euro. Therefore, negative pledges in euros only really apply to bonds issued after 2004, a relatively small percentage.

Equally, cross-acceleration, cross-default and moratorium event of default clauses only apply to international debt denominated in currencies other than euros. Therefore bondholder remedies such as acceleration are only relevant to a very small percentage of debt issued before 2004.

Given that the percentage of bonds with difficult clauses is relatively small, Greece could presumably offer some form of tender, additional collateral or waiver for them. This opens up a number of possibilities. For example, it would be able to collateralize a future Euro-denominated issue of securities in a European version of Brady bonds. Or alternatively, obtain a partial guarantee of the new instruments from a creditworthy party as the Seychelles did recently.

На рисунке показан профиль погашения греческого долга.