Заседание 11-12 декабря будет гораздо более интересным. Мы ожидаем, что программа QE увеличится с 40 млрд. долларов до 85 млрд. долларов для того, чтобы сохранить темпы покупки активов постоянной даже после завершения операции Твист. Сдвиг в сторону основанной на событиях установки целей (вместо теперешних целей, основанных на календарных датах – середина 2015 года) и заключение прогноза-консенсуса для экономики также будет рассматриваться, хотя мы не беремся прогнозировать результат по этому вопросу.

Таким образом, GS дает установку на дальнейшую слабость доллара вплоть до 12 декабря.

Это очень важно, поскольку от позиционирования относительно USD зависит позиционирование RORO ( значение этого термина смотрите здесь RORO (вью рынка)).

К этому можно еще добавить рекомендацию того же Goldman Sachs шортить 10-year US Treasuries

Голдман часто дурит своих клиентов, но здесь, по-моему, не тот случай.

Потом, значение имеет не то, окажется ли Голдман прав или нет, а то, какое значение для рынков это имеет прямо сейчас.

Голдман имеет большое влияние на умы крупных инвесторов ( к ним я также отношу валютных дилеров крупных корпораций, управляющих суверенными фондами и менеджеров валютных резервов), и мы видим отголоски этого влияния в реакции валютного рынка.

А то, в каких валютах крупные инвесторы паркуют свои активы, непосредственно определяет RORO.

EURO/USD: несмотря на повсеместно по еврозоне плохие данные PMI, после коррекции на этих данных на 70 пунктов, после разочарования от ФОМС (единственным позитивным событием для EURO вчера стало выступление Драги) на сегодня уже превысил вчерашний максимум и выглядит сильным.

Произошло это несмотря на то, что цены на нефть падают 4-й день подряд. Цены на нефть тоже оказывают влияние на курс EURO/USD.

AUD/USD после вчерашнего PMI Китая от HSBC сохранил силу до конца дня и закрылся выше 200-дневной средней.

Я не очень сильно по-бычьи настроен - слегка. Такой настрой можно назвать «скорее бык, чем медведь».

Я вижу серьезные негативные факторы для RORO. Но результат сравнения позитивных и негативных факторов дает небольшой перевес в сторону позитивных факторов с тенденцией роста этого перевеса в ближайшие недели.

Поэтому я «скорее бык, чем медведь».

На мой взгляд, к середине сентября набралась некоторая перепроданность USD, которая в течение месяца постепенно устранялась. Возможно, к текущему моменту она почти полностью исчезла и сейчас у EURO/USD есть определенные шансы подрасти в ближайшие 2 месяца до 1,32-1,33 без явных драйверов для роста.

Существует немаленькая вероятность, что EURO/USD продолжит двигаться в узком коридоре 1,28-1,32 вплоть до 12 декабря.

Сейчас EURO/USD находится посередине этого коридора, и это не лучшее время для совершения сделок.

Есть также некоторые события, которые могут оказаться позитивными для EURO: например, обращение Испании за помощью.

Гораздо труднее что-то определенное сказать относительно S&P500.

В последнее время мы наблюдаем некоторое расцепление между ростом американского рынка и слабостью доллара. Одно для меня очевидно – S&P500 стоит чересчур дорого относительно финансовых показателей компаний, входящих в индекс.

И хотя я ожидаю, что в этом году индекс S&P500 превысит в какой-то момент 1500 пунктов, но даже сейчас еще возможна коррекция от текущих уровней на 20-30 пунктов вниз.

Проходящая сейчас компания квартальных отчетов тянет фондовые индексы вниз. Но после ее завершения, а в ближайшие 10 дней большинство самых крупных компаний отчитаются, они могут опять воспрянуть.

Сегодня после завершения американской торговой сессии отчитывается крупнейшая компания в мире Apple, и реакция рынка может оказаться достаточно серьезной.

Последние отчеты компании приносили положительные сюрпризы. Как будет на этот раз?

USD/JPY прорвал 80. Если пара, которую я шорчу, сумеет закрепиться выше 80, то это будет еще одним свидетельством, что RORO сдвигается в сторону покупки риска.

Я понимаю, что мой вью рынка выглядит нечетким, но, что поделать, таковой мне представляется ситуация на рынке. Я тщательно старался расставить акценты должным образом.

На рынке сформировался консенсус относительно того, что в среду мы увидим запуск программы QE3.

Рассматриваются различные варианты: покупка MBS, покупка композиции MBS и казначейских бумаг, продолжение операции «Твист», удлинение периода очень низких процентных ставок.

Возможности Феда в определенном плане ограничены: не буду повторять эти нюансы - подробности здесь

16 июня по поводу предстоящего заседания ФОМС высказался главный экономист Goldman Sachs Ян Хатциус.

Мы ожидаем, что ФОМС осуществит операцию количественного смягчения на заседании, которое пройдет на следующей неделе. Наш базовый вариант предполагает новую программу покупки активов, которая приведет к увеличению баланса Федрезерва, но также возможны расширение операции «Твист» или дальнейший сдвиг периода низких краткосрочных процентных ставок в заявлении ФОМС за пределы текущей формулировки «конец 2014 года».

Последняя мера из списка Хатциуса (увеличение периода низких процентных ставок) является составным элементом программы «Твист». Банки, которые покупают краткосрочные бумаги Казначейства США, должны быть уверены, что в обозримом будущем не произойдет повышения их доходности (цены на облигации при этом падают).

Три члена ФОМС на позапрошлой неделе недвусмысленно высказались в пользу QE: Локхарт, Вильямс и заместитель Бернанке Джанет Йеллен.

Йелен подготовила большую презентацию, обосновывающую необходимость запуска QE3.

Нынешний состав ФОМС является «голубиным». Всего один член ФОМС (Лэкер) постоянно выступает за более жесткую политику. Поэтому вероятность запуска программы QE3 на заседании Федрезерва в среду вполне реальна.

НЕ СЛУШАЙТЕ, ЧТО ГОВОРИТ ЙЕЛЛЕН, СЛУШАЙТЕ ТОЛЬКО ДАДЛИ И БЕРНАНКЕ

Йеллен всегда говорит о том, что экономике нужен QE.

В то же время в недавнем выступлении самого Бернанке в конгрессе никаких намеков на QE3 не прозвучало.

Другой влиятельный член ФОМС, глава ФРБ Нью-Йорка Дадли еще 24 мая считал, что на монетарном фронте ничего предпринимать не надо.

Earlier today, New York Fed Chairman Bill Dudley told CNBC that he did not feel that another round of quantitative easing would be necessary, on the recent strength in the U.S. economy.

My view is that, if we continue to see improvement in the economy, in terms of using up the slack in available resources, then I think it's hard to argue that we absolutely must do something more in terms of the monetary policy front.

Дадли доволен тем, как идут дела в американской экономике и не видит смысла в новом раунде количественного смягчения.

Дадли не волнует дефляция в «японском стиле».

What's changed for me [from last year] is that I'm a little bit more confident that the economy's going to keep growing. I'm a little bit less worried about a Japanese-style deflation outcome. And that was really the reason that, for me personally, motivated the need for further monetary policy action.

Таким образом, второй по значимости человек в Федрезерве четыре недели назад ясно давал понять, что никакого QE3 в июне не будет. Притом, Дадли никогда не был ястребом.

Изменили ли последние данные по занятости решительным образом его взгляды? У меня есть сомнения в этом...

СКОРЕЕ ВСЕГО, КОНСЕНСУСА ПО ЭТОМУ ВОПРОСУ СРЕДИ ЧЛЕНОВ ФОМС ПОКА НЕТ, И ВСЕ РЕШИТСЯ В СРЕДУ – НЕПОСРЕДСТВЕННО НА САМОМ ЗАСЕДАНИИ.

Мое мнение: QE3 не будет, но в заявлении Комитета будут сильные вербальные интервенции в пользу QE.

МЫ ЭТО НЕ ВСЕГДА ЗАМЕЧАЕМ, НО ФЕДРЕЗЕРВ, ТАК ЖЕ КАК И ДРУГИЕ ЦЕНТРАЛЬНЫЕ БАНКИ В ПОСЛЕДНЕЕ ВРЕМЯ АКТИВНО ИСПОЛЬЗУЕТ МЕТОД «ВЕРБАЛЬНЫХ ИНТЕРВЕНЦИЙ».

Это когда центральный банк обещает что-то предпринять, и обещания оказывают на рынки нужное воздействие (временное), как будто он что-то действительно предпринял в этом направлении.

Помимо прочего, использовав сейчас возможность QE, Бернанке лишит себя эффективного средства реагирования на ухудшение дел в экономике по крайней мере на ближайшие 6 месяцев. Об этом тоже не следует забывать.

Поэтому у меня большие сомнения в том, что на ближайшем заседании ФОМС Федрезерв запустит новую программу QE3.

Michelle Meyer, старший экономист Bank of America/Merill Lynch недавно в интервью Bloomberg TV также заявила, что их команда не видит в ближайшем будущем нового раунда QE.

Мы не думаем, что на следующей неделе мы увидим действие со стороны Федрезерва, но мы думаем, что будет очень «голубиное» заявление. Мы также думаем, что Федрезерв установит ориентир для следующего раунда количественного смягчения. Мы думаем, что следующий раунд наступит либо на заседании 1 августа, либо на заседании 13 сентября.

Существует также целый ряд моментов, которые препятствуют запуску QE3.

1.Бежевая книга свидетельствует, что в американской экономике все обстоит не так уж и плохо.

The basic gist: Things aren't amazing, but they're not collapsing.

Economy showed a 'moderate pace' of expansion.

Prepared at the Federal Reserve Bank of Dallas and based on information collected on or before May 25, 2012. This document summarizes comments received from business and other contacts outside the Federal Reserve and is not a commentary on the views of Federal Reserve officials.

Reports from the twelve Federal Reserve Districts suggest overall economic activity expanded at a moderate pace during the reporting period from early April to late May. Activity in the New York, Cleveland, Atlanta, Chicago, Kansas City, Dallas, and San Francisco Districts was characterized as growing at a moderate pace, while the Richmond, St. Louis, and Minneapolis Districts noted modest growth. Boston reported steady growth, and the Philadelphia District indicated that the pace of expansion had slowed slightly since the previous Beige Book

Основной смысл: дела идут не блестяще, но в то же время и кризиса нет.

Экономика показывает умеренные темпы роста. Это ставит под вопрос новый раунд количественного смягчения.

2.Запуск QE3 имеет определенные политические препятствия.

Reinhart thinks the Fed will try to do the right thing, but there is one headline that Ben Bernanke is most worried about seeing.

“The headline they most worry about is ‘The Fed acts to help the incumbent.’ ”'

Bernanke will try and do what is right for policy, but actions made between now and the election will be looked at through different lenses.

The last thing Bernanke wants to be is the Fed boss that blew Fed independence, by taking some action that invites more oversight and control from Congress.

Рейнхарт считает, что Бернанке собирается делать правильные вещи, но одно обстоятельство должно вызывать у него беспокойство.

Действия, предпринимаемые им сейчас – за несколько месяцев до выборов – будут рассматриваться в различных плоскостях.

Бернанке не хотел бы стать тем руководителем Федрезерва, который привлек бы своими действиями особое внимание конгресса и поставил бы под угрозу независимость Федрезерва.

Поэтому Бернанке будет проявлять чрезвычайную осторожность.

3.Федрезерв до сих пор использовал инструменты количественного смягчения в ситуациях, когда это было действительно необходимо. Про текущую ситуацию этого нельзя сказать.

Инфляция, только начала снижаться, дела в экономике идут еще пока относительно неплохо, фондовые рынки стоят высоко. Между прочим, операция «Твист» еще не закончилась.

4.Есть сомнения, что в текущей ситуации программа будет иметь существенный эффект

На этом вопросе остановлюсь подробнее.

СИСТЕМНЫЙ УХОД ОТ РИСКА ОСЛАБИТ ВОЗДЕЙСТВИЕ ПРОГРАММЫ QE

В чем особенность текущей ситуации?

В еврозоне происходит сильный кризис, европейская валюта находится под постоянным давлением, что вызывает бегство в безопасные активы, главным образом в американские и и японские облигации, которые находятся на рекордно низких уровнях доходности.

Некоторые аналитики считают, что даже в случае нового раунда QE эти доходности могут остаться на таком же низком уровне.

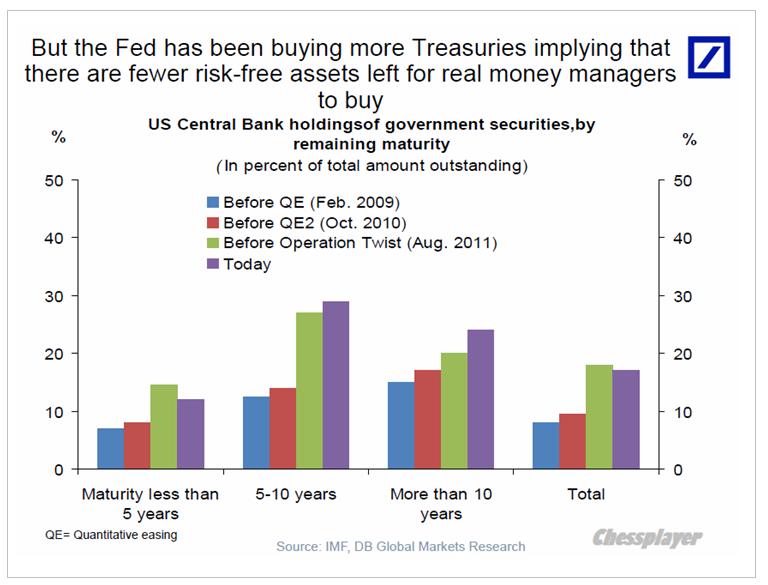

С момента первого раунда QE композиция и размер баланса Федрезерва изменились драматичным образом. Теперь Федрезерв владеет существенно большей частью US Treasuries, чем раньше.

Torsten Slok из Deutsche Bank пишет:

Помимо прочего, покупая государственные облигации центральные банки (Федрезерв, ЕЦБ, Банк Англии, Банк Японии) уменьшили предложение безрисковых активов, которые управляющие реальными деньгами менеджеры имеют возможность купить. Так, например, Федрезерв в настоящий момент держит на своем балансе порядка 30% всего имеющегося количества 5-10 year US Treasuries.

Вывод: УВЕЛИЧИВШИЙСЯ СПРОС НА БЕЗРИСКОВЫЕ АКТИВЫ И УМЕНЬШИВШЕЕСЯ ИХ ПРЕДЛОЖЕНИЕ ВКУПЕ СО ЗНАЧИТЕЛЬНЫМИ ДОЛГОСРОЧНЫМИ РИСКАМИ ЗАМЕДЛЕНИЯ ГЛОБАЛЬНОГО РОСТА ПОДРАЗУМЕВАЮТ, ЧТО ПРОЦЕНТНЫЕ СТАВКИ, ВЕРОЯТНО, ОСТАНУТСЯ НА НИЗКОМ УРОВНЕ ЕЩЕ В ТЕЧЕНИЕ МНОГИХ ЛЕТ.

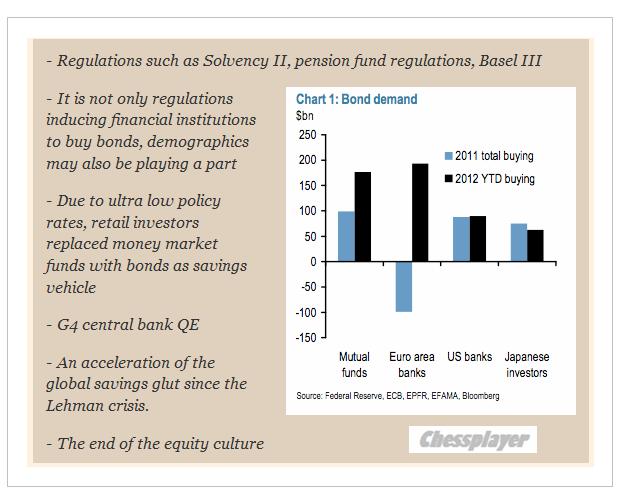

Команда Flows and Liquidity (денежные потоки и ликвидность) из JP Morgan дает еще 5 причин, помимо количественного смягчения, почему ставки доходности будут оставаться низкими в обозримом будущем:

Новации в области регулирования: Solvency II, новые нормы для пенсионных фондов, Basel III

Не только регулирование стимулирует финансовые институты к покупке облигаций, демография также играет роль

Вследствии политики сверхнизких процентных ставок, розничные инвесторы заменяют фонды денежного рынка облигациями как средством сбережений.

Ускорение перенасыщения средствами сбережения с момента кризиса Лемана

Конец «культуры акций»

На рисунке внизу показаны объемы покупок крупными группами инвесторов облигаций в 2011 и 2012 годах

Таким образом, как считают эти аналитики, даже новый раунд QE может не привести к росту доходности US Treasuries.

Соответственно, это будет препятствовать ослаблению доллара и росту цен на рискованные активы.

Таким образом, в текущей рыночной фазе новый раунд QE может оказаться неэффективным – он будет «съеден» системным уходом от риска.

Члены ФОМС это прекрасно сознают и это обстоятельство будет ими принято во внимание.

Китай показал в феврале самый большой торговый дефицит за 20 лет.

China has posted a massive trade deficit for February.

The cause was very weak exports, which fell 23.6% month-over-month. The Lunar New obviously had a lot to do with that.

For the combined January-February period -- which attempts to blend out the impact of the Lunar New Year crossing two weeks and coming at different times each year -- export growth of 6.8% since the year 2000 (excluding 2009, of course).

On the bright side, import growth of 39.6% year over year was far better than the decline of 15.3% in January... this may be a harbinger of a new pickup in exports.

In light of the Chinese trade deficit, the Aussie trade deficit, and the Japanese trade deficit, you might be asking as some are: Who has the trade surplus? The answer, we're guessing, is: The oil states.

Кто спрашивается в таком случае находится в профиците? Государства – поставщики нефти.

Китай продолжил накапливать резервы черного золота в свете предстоящей эскалации конфликта вокруг Ирана.

Экономист Goldman Sachs Ян Хатциус оптимистичен относительно рынка труда, но совсем не так оптимистичен относительно ВВП.

Hatzius is not bullish on GDP.

Why is our forecast for GDP growth still so muted? Apart from weather and seasonal issues, which are probably less important for the GDP data than for the labor market and the CAI, there are two reasons. One is that indicators of final demand still look quite soft. Final demand (GDP less inventories) grew just 1.1% in Q4 and an estimated 2% in Q1.

The other issue is oil. Our models say that a 10% seasonally adjusted gasoline price increase—roughly what we have seen since the second half of 2011—should take an average of 0.4 points off annualized growth over the following year. That's not yet a huge effect, but it is the sort of magnitude that starts to matter from a forecasting perspective. We also don’t think that the low level of natural gas prices will offset much of the increase in gasoline prices; as we showed recently, household and business expenditures on natural gas, evaluated in terms of the commodity cost, are only one-ninth as large as expenditures on oil and oil products as of 2011. This means that changes in oil (and especially gasoline) prices are nine times more important than proportional changes in natural gas prices.

Хуссман выдвигает пять причин, почему рынок должен начать снижаться в ближайшие пять дней.

Hussman's bearishness is well known, but the article by Randall W. Forsyth boils down Hussman's bearishness to five criteria:

• the Standard & Poor's 500 trading at more than 8% above its 52-week exponential moving average

• the S&P 500 up more than 50% from its four-year low

• the "Shiller P/E," based on the cyclically adjusted trailing 10-year earnings, developed by Yale economist Robert Shiller, greater than 18; it's currently 22

• the 10-year Treasury yield higher than six months earlier

• the Investors Intelligence's bullish advisory sentiment over 47%, and bearishness under 25%; in the latest data, the numbers were 47.9% bulls and 26.6% bears

Apparently all those conditions are nearly in place now, as they were in 1987, 2000, and 2007.

Meanwhile, Zimmerman agrees with all that, plus he cites the inevitability of a market decline owing to rising taxes, austerity, too much bullishness, and gas prices. He sees a "perfect storm" manifesting itself within days.

Главная идея этого комментария: мы видим большие шансы, что ФОМС возобновит количественное смягчение в конце этого года или в начале 2012 года

В виду отсутствия времени комменты на русском будут очень краткими.

From Jan Hatzius: QE3 Now Our Base Case

Summary

We now see a greater-than-even chance that the FOMC will resume quantitative easing later this year or in early 2012. We have changed our call because today's statement suggests that the committee's reaction function to incoming economic news is more dovish than we had previously thought. Although Fed officials still expect a gradual decline in the unemployment rate, they made a conditional commitment to keep the funds rate unchanged "at least through mid-2013" and implied that they would employ additional policy tools in case their economic forecast deteriorated further. This would probably mean more QE if their forecast converged to our own modal view of a flat-to-higher unemployment rate through the end of 2012, let alone our downside risk case of a renewed recession.

Full note:

It's official: the federal funds rate is highly likely to stay at its current near-0% level until 2013 (or later). Although this has been our forecast all along, today's FOMC statement was nevertheless more dovish than we had anticipated in two respects:

1. The policy commitment to keep the funds rate at "...exceptionally low levels...at least through mid-2013" was more aggressive than we had anticipated. Some commentators today expressed disappointment that this is still a conditional commitment, i.e., Fed officials kept an "out" if growth is much stronger and/or inflation much higher than expected. But that was not a surprise. The surprise was the fact that there is a date at all (for the first time ever in the history of Fed communications) and even more so the fact that the date is almost two years in the future.

Сюрпризом был тот факт, что был указан срок сохранения низких ставок ( впервые в истории заявлений Феда), и еще большим сюрпризом был факт, что этот срок уходит в будущее почти на два года.

2. The easing bias in the last paragraph of the statement was more explicit than we had anticipated: "The Committee discussed the range of policy tools available to promote a stronger economic recovery in a context of price stability. It will continue to assess the economic outlook in light of incoming information and is prepared to employ these tools as appropriate." The phrasing somewhat echoed the promise in the September 2010 statement "...to provide additional accommodation if needed...", which sealed the deal for QE2. In our view, the committee's explicit easing bias suggests that the threshold for additional easing in terms of downward revisions to the committee's forecast is relatively low.

Явный намек Комитета на количественное смягчение предполагает, что порог для начала QE в рамках пересмотра прогнозов в сторону понижения является относительно низким.

The implication is that the committee would probably ease policy further if its economic forecast converged to our own, more downbeat view. While the committee still expects a gradual decline in the unemployment rate, our own modal forecast is a flat-to-higher rate through the end of 2012. In addition, we see a recession risk of about one in three, and if there was indeed a recession the committee would of course ease further.

Кроме того, мы видим риск рецессии примерно 1 к 3, и если рецессия действительно случиться, то ФОМС безусловно предпримет меры по смягчению.

If there is additional easing, it would likely take the form of QE. After all, "these tools" mentioned in the statement presumably need to be more powerful--or at least not much less powerful--than the action taken today in order to avoid a sense of anti-climax. This means that they are unlikely to consist of small incremental steps such as a commitment to keep the balance sheet large, a gradual shift of the securities portfolio into longer maturities, or a cut in the interest rate on excess reserves from 25 basis points (bp) to zero. This leaves the stronger options, which include QE as well as even more aggressive forms of easing such as rate caps (a form of QE in which the Fed promises to buy as many securities as needed to hit a longer-term yield target), a price level or nominal GDP target, or interventions in non-government securities markets (for which funding from Congress would be needed). Of these, "conventional" QE is very likely the option with the lowest hurdle, and the first one to be deployed.

Хатциус считает возможным развертывание даже более серьезных мер QE, чем обычная покупка долгосрочных казначейских бумаг.

Although QE3 is now our base case, it is not a certainty. We see three main ways in which our revised call could turn out to be incorrect. First, of course, the economy may turn out to be stronger than our forecast. In this case, Fed officials would not need to revise down their forecast, and would probably not ease further.

Second, inflation might pose a higher hurdle to additional easing than we have allowed. There are only tentative signs of deceleration in core inflation, and inflation expectations show few signs of breaking lower despite the recent weakness in the economic data and risk asset prices. This is a risk to our view, although the stickiness of inflation expectations might already reflect an assumption by the market that the Fed will ease, in which case inflation expectations would fall sharply if the Fed failed to deliver.

Third, the anti-Fed backlash late last year might argue against further QE. That is possible, but the problem might be reduced via a slight tweak in the policy's design. That is, Fed officials might choose to specify the policy not as a large-and-scary upfront number but a smaller monthly flow of purchases. Although the substantive differences are small--e.g. a $600bn purchase over eight months is basically the same as a $75bn-per-month purchase that is expected to last eight months--the cosmetics of the flow approach might be more appealing. Moreover, it would also be more flexible because the committee would revisit the program from meeting to meeting.

Хотя QE3 теперь наш базовый вариант, это вовсе не то, что он обязательно случиться.

Хатциус приводит 3 случая, при которых QE не будет: улучшение в экономике, инфляция выше заданных уровней, негативная реакция на завершившиqся QE2.

Хатциус считает возможным задание ежемесячного объема покупок.

While these points could pose problems for our call, we disagree strongly with one argument against further QE that we heard frequently today--namely that the three dissents from Presidents Fisher, Kocherlakota, and Plosser indicate "the end of the line" for further Fed easing and difficulty for the chairman to get his way. On the contrary, we view Chairman Bernanke's willingness to live with the dissents as a strong signal that he and the rest of the Fed leadership view the need for renewed easing as more important than the institutional norm of consensus decisionmaking. There is no question that Bernanke will always have enough votes, and we fully expect him to use these votes to provide further support to the economy if he views it as necessary.

Хатциус не считает наличие трех выступающих против планов смягчения глав федеральных резервных банков препятствием для QE3.

Это будет совсем непохоже на то, что было в Японии

Ян Хатциус: «В истории еще не было такого момента, который можно было бы поставить рядом с текущей ситуацией».

О критериях, которые будут использовать агентства при принятии решения о понижении рейтинга.

We expect the rating agencies will use two primary criteria to evaluate the eventual debt limit agreement:

Debt limit uncertainty: Proposals that increase the debt limit for a longer period appear to have a better chance of leading to more positive rating outcomes, by reducing uncertainty regarding interest and principal payments. This implies that an increase in the debt limit of $2.4 trillion that occurs in two stages would, all things being equal, pose more risk to the US AAA rating than a single increase of $2.4 trillion.

Medium-term fiscal stabilization of debt trajectory: In order to maintain their AAA ratings and return to a stable outlook, S&P and Moody’s have indicated that a deficit reduction package of roughly $4 trillion over ten years would need to be agreed to by Congress. The primary measure of stability in debt dynamics that the rating agencies are likely to look for is stabilization of the debt-to-GDP ratio by mid-decade. This is similar to the G20 declaration in 2010 that debt-to-GDP ratios should be stabilized or in decline by 2016. In practice, this should essentially require the primary deficit to be eliminated by that time. In the US, this would imply a 6% of GDP improvement in the structural fiscal balance over five years.

The upshot is that the ratings reaction to the plan that will hopefully be enacted in coming days is likely to depend not only on the headline savings achieved, but also on the balance between the uncertainty that the chosen enforcement mechanism creates on the one hand, and the credibility that it provides to the reform process on the other hand. Unfortunately, the relative importance of these factors to the rating agencies (and S&P in particular) is unclear, as is how much other "soft" factors – such as the breadth of political support for the agreement for the agreement – will weigh in their decision.

Это будет связано также с тем, сколько неопределенности останется в ситуации с госдолгом США после повышения лимита госдолга

Какие последствия видит GS

Прежде всего GS считает, что понижение рейтинга не приведет к продажам казначейских бумаг

A downgrade should not force sale of Treasuries

If one of the rating agencies does decide to downgrade the US sovereign rating, we see three main direct effects:

Knock-on downgrades. Rating agencies are likely to downgrade the ratings of some issuers that are closely linked or directly backed by the US government. The most obvious candidates are Fannie Mae and Freddie Mac, which are under conservatorship and rely on federal financial support. Fannie and Freddie MBS benefit from an implicit guarantee but are not rated, though they could still be affected. Ginnie Mae securities on the other hand, are directly backed by the federal government, and would likely be downgraded. AAA-rated Federal Home Loan Banks (FHLBs) don't rely on federal capital or financing, but would also be downgraded in the event of a sovereign downgrade, according to S&P. AAA-rated insurers would as well, in light of S&P's policy of not rating insurers higher than sovereigns of the same jurisdiction. Highly rated bank holding companies and bank subsidiaries could also be subject to downgrade, since some benefit from ratings "lift" above the banks standalone strength; while S&P has indicated that it would not immediately downgrade any banks or broker dealers in relation to a sovereign downgrade, Moody's has indicated that it might in the event that it downgraded its US sovereign rating.

Collateral effects. The primary issue here is the repo market, since AA-rated Treasury and agency securities could face slightly higher haircuts, either as a result of a possible downgrade or as an indirect result of volatility that results from a downgrade. In the broader repo market, Treasuries are the dominant form of collateral, though in the tri-party repo market, agency MBS and CMOs comprise a greater share of the total collateral used (roughly 40%) than Treasuries (30%) and GSE debt (9%) do. In the event of a downgrade, it is reasonable to expect that the haircut on these securities might rise by up to one percentage point (the New York Fed estimates the median haircut for Treasuries and agency debt and MBS is currently 2%). Treasuries, and to a lesser extent agency securities, are also used for derivatives margining, though the aggregate amounts are much smaller. This would cause a modest contraction in available funding; 1% of an estimated $1.7 trillion tri-party repo market, of which 80% relies on government securities, would reduce funding using current collateral by $14 billion.

Capital requirements and investment mandates. In general, it is unlikely that a downgrade would result in significant pressure on regulated entities to shift assets out of Treasuries or agency securities, though it is conceivable that there may be some isolated areas where this could occur. In general, as shown in the table below, regulatory requirements often treat government securities as a separate asset class. Moreover, regulatory constraints typically would not come into play if a downgrade were only of one or two notches, to the AA+ or AA level. Likewise, a downgrade by only one rating agency is less likely to trigger such a reaction than a downgrade by two rating agencies. What happens to the significant portion of Treasury and agency securities held by foreign investors is a more complex question given a diversity of mandates – a few of these might rely on ratings – versus the deeper liquidity of the US government securities compared with any alternative investment, and the fact that a good deal of foreign holdings are the byproduct of the buildup of reserves in growth economies, particularly in Asia, that are generating large current account surpluses.

Как повлияет понижение рейтинга США на цены на активы.

With those warnings in mind, we suspect we would see the following reactions to a US downgrade:

A drop in equity markets, but probably a modest one. Equities usually but not always dropped on the day of downgrade; a further drift down of a few percent over the subsequent month was typical. But the average drop in the equity market was less than 1% on the day, and there were exceptions over both the 1-day and 1-month horizons. Part of the reason for this—and the often mild moves in other asset classes—is undoubtedly that the debt issues had long been on the market’s radar and the potential for a downgrade was known, though we had trouble finding a clear pattern in the behavior of equities in the months leading up to the downgrade.

Some weakening in the currency. The yen dropped by more than 1% versus the dollar on two of the downgrade episodes; moves in the other cases were very small. Given the large foreign holdings of Treasuries, it would not be surprising to see a somewhat bigger effect on the dollar in the event of a US downgrade, although we would be surprised by a move of more than a few percent. The effect on the currency could also be mitigated by repatriations of foreign assets to increase cash holdings.

A steepening of the yield curve and a cheapening of Treasuries relative to OIS. The Japan, Canada, and Spain episodes showed no clear pattern in ten-year yields or spreads to US Treasuries. This may be because downgrades imply two opposing forces: a heightened premium for holding government debt, which pushes yields higher, but more pressure for fiscal austerity, which would slow growth (at least in the near term) and pushes yields lower. This tug-of-war was evident earlier this year when Standard & Poor’s changed its US rating outlook to negative: ten-year Treasury yields ended the day little changed. Standard & Poor’s has indicated an expectation of a 25-50bp increase in “long-term” US interest rates in the event of a downgrade; this is certainly possible at the very long end of the curve,, but we suspect the impact on the ten-year note would be smaller, at least initially. One clearer implication is a curve steepening, since the impact of austerity is disproportionately felt at the front end of the curve whereas the heightened risk premium is most significant at the long end. This effect could be reversed (i.e., more front-end weakness) if the US were to go into a "technical default," but we view this as a very remote scenario. Relative to the expected path of short-term interest rates (i.e., OIS), we would expect Treasuries to cheapen somewhat further (currently, 10-year Treasuries trade 20bp above corresponding maturity OIS).

Some weakness in the financials sector. In the event of a US sovereign downgrade, S&P has indicated that AAA insurers, the GSEs, and the Federal Home Loan Banks would be downgraded as well. Although a recent S&P statement suggested that “banks and broker-dealers wouldn’t likely suffer any immediate ratings downgrades,” an increased premium on sovereign debt could result in some indirect impact on debt and equity of financial firms beyond those insurers directly affected.

Все это важно, но у меня нет времени переводить.

Если понижение рейтинга случится в ближайшие 3-4 недели, - пишет Ян Хатциус, то это повлечет за собой:

Падение рынков акций, хотя, возможно, и умеренное

Некоторую слабость в валюте

Кривая доходностей увеличит кривизну, а трежеря станут дешевле, чем overnight indexed swap (OIS)

От вчерашней речи Бернанке на международной конференции в Атланте ждали сигналов о дальнейшей политике Федрезерва, но речь не вполне оправдала ожиданий. Как метко заметил главный экономист Goldman Sachs Ян Хатциус, краткий вывод, который можно сделать из речи – «мы находимся в зоне бездействия Феда».

По доллару голдманисты тоже шарахаются из стороны в сторону...Похоже, ребята запутались в последнее время: вряд ли стоит им доверять.

В действиях Голдмана усматривается политическая установка от властей. Инвесторы сейчас относятся с недоверием как к доллару, так и к UST. Монетарным властям Америки важно, чтобы в ситуации неопределенности с бюджетом не началось бегство из доллара и казначейских бумаг; особенно учитывая последние заявления китайских официальных лиц.

Но основной тезис Яна Хатциуса в комментариях речи Бернанке бесспорен: для новой программы покупки активов (QE3) необходимо «дальнейшее заметное ухудшение перспектив экономики». Здесь они имеют в виду не только темпы роста ВВП, но и фондовые рынки. Это можно расценить как сигнал к коррекции как минимум в район 1250 пунктов по индексу S&P500 (туда можем дойти очень быстро).

После выступления Бернанке весь вчерашний дневной рост сошел на нет и американский рынок акций опустился к минимумам июня. Теперь представляется очень вероятным движение к 1250 пунктам по индексу S&P500 с промежуточной остановкой в районе 1276 пунктов.

Интересный вопрос теперь возникает: насколько необходимо упасть американскому рынку акций, чтобы у Бернанке появились основания для начала новой программы количественного смягчения QE3?

1250 пунктов представляется для этого слишком малым. Наверно, как минимум, это должно быть 1130 пунктов по индексу S&P500. А может быть ниже: 1010-1040?

От вчерашней речи Бернанке на международной конференции в Атланте ждали сигналов о дальнейшей политике Федрезерва, но речь не совсем оправдала ожиданий. Как метко заметил главный экономист Goldman Sachs, краткий вывод, который можно сделать из речи – «мы находимся в зоне бездействия Феда».

Последний и основной абзац речи, в котором собраны все основные тезисы:

Хотя движение идет в правильном направлении, экономика все еще имеет производство на уровнях заметно ниже ее потенциала; следовательно, мягкая экономическая политика все-еще необходима. Пока мы не увидим устойчивый период сильного создания рабочих мест, мы не можем считать, что восстановление установилось правильным образом. В то же время, долгосрочное здоровье экономики требует, чтобы Федрезерв был бдителен в сохранении с таким трудом завоеванного доверия в обеспечении ценовой стабильности. Как я уже объяснял, многие члены ФОМС считают, что недавний рост инфляции был проходящим и ожидают, что инфляция останется умеренной в среднесрочном периоде.

Однако если этот прогноз окажется неверным, и в частности, если появятся сигналы, что инфляция стала на более широкую основу или что долгосрочные инфляционные ожидания стали менее твердыми, Комитету придется ответить на это необходимыми мерами. При всех обстоятельствах, наши действия будут направлены на цель поддержания восстановления в производстве и на то, чтобы занятость помогла обеспечить инфляцию на том уровне, который бы соответствовал мандату Федрезерва.

Прежде всего следует отметить, что в речи появилось это магическое слово – бдительность (vigilant), которое является своего рода намеком на более жесткую монетарную политику.

Об ужесточении говорить пока не приходится, но рынки восприняли эти слова как четкий сигнал, что продолжения количественного смягчения в ближайшее время ждать не приходится.

Fed Chairman Bernanke's speech at the International Monetary Conference acknowledges slower growth but views this as at least partly due to temporary factors. Easy monetary policies “are still needed” given the economy continues to perform “well below its potential.”

1. Fed Chairman Bernanke began his remarks by acknowledging the "slower than expected" growth so far this year. He specifically cited supply chain disruptions stemming from the Japanese earthquake and tsunami as a factor slowing growth in Q2. However, despite the "frustratingly slow" pace of recovery thus far, Bernanke sees growth as "likely to pick up somewhat in the second half of the year" as manufacturing activity normalizes and gasoline prices ease a little.

2. Noting the headwind from fiscal drag, Bernanke emphasizes the need to “move quickly to enact a credible, long-term fiscal consolidation plan.” His wording makes clear that he sees a strong case for rapid decisions and action, but a tightening that is gradually phased in so as not to be “self-defeating”. Such a plan could also provide short-term benefits if it improved confidence and/or lowered long-term borrowing rates. In the question and answer session following the speech, Bernanke ducked a question asking him to choose between near-term stimulus and long-term tightening, repeating that he saw the problem as fundamentally long-term in nature.

3. Bernanke notes "the recent increase in inflation is a concern" but suggests that "there is not much evidence that inflation is becoming broad-based or ingrained in our economy". Given that gasoline prices account for most of the pickup in inflation, Bernanke takes the view that "developments in the global market for crude oil...rather than factors specific to the US economy" are the main driver of higher inflation in recent months. Bernanke goes on to argue that the sharp increase in commodity prices in recent years is primarily driven by strong gains in global demand alongside constrained supply, rather than the byproduct of easy Fed policies. In any case, he expects considerable labor market slack and stable long-term inflation expectations to keep US inflation restrained going forward.

4. No surprises in the commentary on monetary policy: "QE2" is to wind down at the end of the month, but reinvestment of principal payments on the Fed's securities holdings will continue. In Bernanke's words: "Although it is moving in the right direction, the economy is still producing at levels well below its potential; consequently, accommodative monetary policies are still needed. Until we see a sustained period of stronger job creation, we cannot consider the recovery to be truly established." That implies a fairly high bar for any monetary tightening. At the same time, there is of course no mention of the possibility of another asset purchase program--this would require a notable further deterioration in the outlook to be considered seriously. In short, we remain well within the “zone of inaction” for the Fed.

5. In the question and answer session following the speech, Bernanke attributed recent weakness in the US dollar partly to the relaxation of risk aversion following the crisis, and partly to the “quite weak cyclical position” of the US economy relative to many trading partners (especially emerging markets). In his view, the best way for the Fed to support the dollar “in the medium term” is to keep inflation stable and help the US economy recover.

Самый важные здесь пункты 4 и 5.

QE2 должна быть свернута в конце месяца, но реинвестирование средств от погашаемых MBS будет продолжаться. Это предполагает достаточно высокий барьер для ужесточения монетарной политики. В то же время, конечно, нет и упоминания возможности новой программы покупки активов - для этого потребуется дальнейшее заметное ухудшение перспектив экономики, которое будет оцениваться как серьезное. Если в нескольких словах, мы находимся в зоне бездействия Феда.

В вопросах и ответах по завершении выступления Бернанке приписал недавнюю слабость в долларе США частично ослаблению отвращения к риску, которое последовало вслед за кризисом, и частично слабой циклической позиции американской экономики относительно многих торговых партнеров ( в особенности развивающихся рынков). На его взгляд , лучший путь для Феда – поддержка доллара в «среднесрочный период», чтобы сохранить инфляцию стабильной и помочь восстановлению американской экономики.

Zero Hedge регулярно публикует прогнозы от Goldman Sachs, отдавая дань глубокого уважения главному дилеру мирового финансового казино. Питомцы GS занимают ключевые посты в государственных финансовых структурах Нового и Старого Света. Уильям Дадли – бывший главный экономист GS, нынче заместитель Бернанке и глава ФРБ Нью-йорка, который, как известно, играет исключительную роль в проведении монетарной политики Федрезерва. Другой главный экономист GS – европейского подразделения, стал недавно членом совета директоров ЦБ Великобритании.

Goldman Sachs является наиболее «инновационной» компанией на Уоллстрит и создал много очень интересных финансовых схем, о которых я планирую рассказать в ближайшем будущем.

А пока о том, что они думают о росте экономике и будущей монетарной политике.

Во-первых, он извиняется, что его предыдущий прогноз относительно роста экономики США не оправдался. Справедливости ради надо сказать, что имеющие конкретную практическую ценность их прогнозы (евро, S&P500) оказались правильными.

Just out from Goldman Sachs

1. Six months ago, we adopted the view that the economy was transitioning to a more self-sustaining recovery and predicted sequential real GDP growth of 3½%-4% (annualized) in 2011-2012. There were three reasons for our shift: a) a pickup in “organic” growth—GDP excluding the estimated impact of fiscal policy and inventories—to more than 4% in late 2010; b) visible signs of progress in private sector deleveraging, and c) another round of fiscal and monetary stimulus.

2. It hasn’t happened. In fact, organic growth seems to have slowed anew to a below-trend pace in the first half of 2011. Moreover, our Current Activity Indicator (CAI)—a statistical summary of 24 weekly and monthly indicators of economic activity—has slowed from an average of 3.7% in the first quarter to 1.6% in April and a preliminary 1.1% in May. If we take the CAI at face value—and it comports quite well with our judgmental sense of how the data have rolled in—that implies a growth slowdown of about 2½ percentage points in recent months.

3. What accounts for this weakness? The Japanese supply chain disruptions are clearly responsible for some of it, but we think that they explain only about 1 percentage point of the deceleration. (This sounds bigger than the 0.6-point drag on Q2 GDP growth that we have estimated previously, but note that a 1-point deceleration in sequential growth in April and May would be consistent with about a 0.6-percentage point deceleration in Q2 as a whole.) The oil price shock is also clearly important but at least by our estimates does not explain the size of the remaining slowdown. The implication is that we are looking at either a weaker underlying growth pace or a greater vulnerability to shocks than we had been assuming.

4. We are still reluctant to take the deceleration entirely at face value, partly because many of the signs of “healing” in the private sector that encouraged us in late 2010 are still visible. The household debt service burden has come down sharply, household credit quality continues to improve, bank lending standards are easing, and financial conditions remain accommodative. Also, we disagree somewhat with the negative tone of much of the recent housing market coverage in the media, including two front-page articles in the New York Times and the Wall Street Journal last week on the renewed slide in home prices. It’s true that overall home prices have slipped to fresh lows. But that wasn’t really a surprise; in fact, we and many other housing market observers had expected renewed downward pressure on prices in 2011 given the still-high levels of excess supply. Moreover, according to the CoreLogic house price index, all of the renewed weakness has come in distressed transactions, while prices of non-distressed homes are actually up slightly in 2011 to date on a seasonally adjusted basis. So it is possible that the recent house price weakness simply reflects a greater effort by banks and GSEs to clear out distressed inventory. That would be a sign that the adjustment process has advanced, and not necessarily a cause for alarm.

5. What would be the policy response to a sustained slowdown? We do not expect much. On the fiscal side, we currently assume fiscal restraint of about 1% of GDP in 2012. This is based on the notion that Congress will implement modest discretionary spending cuts, and that the remaining provisions of the 2009 stimulus package as well as part of the late-2010 bipartisan fiscal deal are left to expire. The most stimulative outcome we can imagine is that all of the 2010 provisions—the payroll tax cut, the unemployment benefits, and the depreciation bonus—are extended, but even that assumption would leave some restraint. And it is also possible that the restraint will be larger than our baseline assumption, via deeper discretionary spending cuts and/or a full expiration of the 2010 provisions. Like it or not, fiscal stimulus no longer has strong advocates in Washington, so its time has very likely passed at this point.

6. This puts the onus on monetary policy. And sure enough, markets that not long ago were predicting rate hikes are now starting to debate QE3. But we believe that the Fed’s “zone of inactivity” is much wider than these wild swings might suggest. The hurdle for rate hikes is high, and we feel good about our long-standing view that the funds rate will remain at its current near-zero level until 2013. But the hurdle for QE3 is also high, and indeed much higher than it was for QE2. First, the perceived cost of QE3 is higher because inflation has accelerated. This reflects the fact that at least some of the weakness in growth this year is due to higher commodity prices, i.e. akin to a supply shock. Second, the perceived benefit from QE3 is lower. Fed officials viewed QE1—defined as the overall balance sheet extension that started in late 2008 and ended in early 2010—as a resounding success, and that was probably one reason why they were fairly quick to climb aboard QE2. But they are much less confident that QE2 made a big difference; while it probably did help financial conditions ease and the economy grow a bit more quickly than it otherwise would have done, it’s hard to argue that the effect was large. That has to color their expectations for what QE3 might deliver. And third, the backlash against QE2 both domestically and abroad was greater than Fed officials had anticipated, and they are not keen to subject themselves to another round of similar criticism.

7. So what is the hurdle for QE3? It probably requires either a meaningful rise in the unemployment rate or flat unemployment coupled with a sharp fall in core inflation and inflation expectations. In contrast, if we just trudge along at a trend or slightly below-trend growth rate and inflation stays near its current pace, neither fiscal nor monetary policy are likely to provide fresh support. Such an outcome might not be so bad from the perspective of the equity market, which already seems to be discounting a fairly weak growth pace. But it would be quite bad for the real economy, not least because it would raise the risk that a significant portion of the increase in unemployment—which still looks cyclical rather than structural at this point—will ultimately become “ingrained” via a loss of skills among the long-term unemployed.

Основные мысли:

Препятствия для повышения ставок велики и мы чувствуем себя очень уверенно в отношении нашего долгосрочного взгляда, что ставка по фондам остнется на текущем, близком к нулю уровне до 2013 года. Но препятствия для QE3 тоже велики, и в действительности они гораздо выше, чем это было для QE2.

Ощущаемая выгода от QE3 меньше.

Отрицательная реакция на QE2 внутри страны и за рубежом оказалась больше, чем Фед того ожидал и теперь они не сильно желают стать предметом еще одного раунда подобной критики.

Так что служит препятствием для QE3? Возможно, оно потребует либо существенного роста безработицы, либо безработица останется неизменной, но произойдет резкое падение в базовой инфляции и инфляционных ожиданиях.

Американцы вторую сессию подряд отторговали практически в ноль. Рынок не растет, т.к. впереди вершина и это разворотная (коррекционная) модель и не падает, поскольку все уже привыкли к бесконечному росту. Любые новости интерпретируются в пользу роста.

Вчерашняя статистика тому пример; как негативные данные можно интерпретировать в пользу роста.

Индекс деловой активности в непроизводственной сфере вышел хуже ожиданий: 57,3 вместо 59,8. Снижение объяснялось сильным падением индекса деловой активности: падение с 66,9 до 59,7 – сильнейшее падение с конца 2008 года. Эта компонента очень тесно коррелирует с ростом ВВП, - объясняет Ян Хатциус из GS, - снижение ВВП увеличивает вероятность продолжения количественного смягчения..

В результате видим условный рыночный рефлекс – резкое ослабление доллара и рост commodities и S&P500. Золото превысило 1450 долларов, а серебро 39 долларов.

Рынок при этом проигнорировал вышедший буквально перед этим совершенно драконовский проект сокращения затрат бюджета от республиканцев.

Не в первый раз подмечаю, что Ян Хатциус выступает в роли этакого дирижера рынка. В критические моменты его комментарии появляются очень быстро, буквально в течение 30-40 минут и оказывают сильное влияние на рынок. Он продолжает убеждать рынки, что QE2 получит продолжение , и рынки верят ему, а не 4-5 управляющим региональными банками Федрезерва. Как-то это странно...

Хотя почему странно? Ян Хатциус – главный экономист Goldman Sachs. А кто его предшественник? Уильям Дадли – глава ФРБ Нью-Йорка, ключевого в системе Федрезерва – банка, который отвечает за проведение монетарной политики Федрезерва. Контакт между ними наверно полный...

Если завтра смотрящий за рынком Ян Хатциус скажет, что сейчас все полетит в тартарары, то все полетит в тартарары.

В мировом финансовом казино игра идет краплеными картами, и они всегда будут в выигрыше. А если случится кризис, то государство опять придет им на помощь.

Джесси Ливермор писал, что манипуляции на рынке возможны только на коротком промежутке времени. Наверно сейчас это правило уже устарело, и манипуляции возможны и на протяжении длительного времени.

Коррекция на американском рынке уже назрела, поводов хоть отбавляй, но меня немного смущает, что индекс S&P500 еще не дошел 6 пунктов до вершины; как правило, они четко отрабатывают цели (это же роботы!). Поэтому вероятнее всего, что они потопчутся, потопчутся, а потом выстрелят вверх, но несильно, а затем уже с осознанием выполненной миссии начнут коррекцию.

Коррекция сейчас целесообразна со всех точек зрения, даже с точки зрения кукловодства. 27 апредя состоится заседание ФОМС, и к этому моменту желательно показать, что без QE никак не обойтись. Вчерашние минутки с последнего заседания ФРС показали, что мнения членов ФОМС уже заметно разделились по этому вопросу.