В пятницу опять стали разгораться опасения насчет Греции. Настоящие они или искусственные – трудно сказать. Как я уже писал, невозможно понять, что там толком происходит. Очень много всякой дезинформации и чепухи льют нам на уши.

Информационный фон выглядит следующим образом: в то время как официальные лица ЕЦБ отклоняют возможность реструктуризации греческого долга, некоторые министры финансов ЕС постепенно склоняются к возможности некоторого рода реструктуризации, как последнего шага.

Германский министр финансов заявил, что дальнейшая помощь (речь идет об удлинении сроков заимствования) возможна, если подтвердится, что частные инвесторы, прежде всего банки, не выходят из греческих долгов и не оставляют всю ответственность европейским налогоплательщикам. Говорит германский министр, что будто действует во благо налогоплательщиков, но на самом деле любая реструктуризация нужна именно для того, чтобы дать возможность банкам максимально вывести деньги из токсичных активов, каковыми являются греческие долговые бумаги. Шансы избежать дефолта у Греции равны 1:10000 по оценке авторитетного Друкенмиллера.

Греческий консервативный журнал "Kathimerini" сообщил, что Греции хватит денег только до 18 июля, и если до конца июня новый транш помощи в 12 млрд. евро не будет выделен, то наступит банкротство.

Доллар в пятницу укрепился почти на 1%, и большая часть этого укрепления была связана с евро. US Treasuries неожиданно продолжили ралли и приблизились к максимумам с начала декабря прошлого года. Но у меня большие сомнения, что доходность 10-летних UST сможет зайти под 200-дневную среднюю скользящую на 3,08 %.(-2,3%). Это противоречило бы фундаментальным условиям, да и наверно долгосрочному тренду. Индекс S&P500, на мой взгляд, сейчас не должен уйти ниже 1290 пунктов. Да, ралли было длительным и американские акции выглядят перекупленными, но ликвидность чересчур велика и деньги необходимо во что-то вкладывать.

Да и сама мягкая реструктуризация долгов Греции - а речь идет только о такой реструктуризации, не должна быть негативной для рынков.

Нынешняя реакция рынков на мой взгляд является рефлексивной... и возможно результатом манипуляций.

Вчера US Treasuries bonds выдали разворотную свечу. Случайно или нет, но это совпало с появлением новых рекомендаций от Goldman Sachs по американским бондам и доллару. Теперь GS показал, что он настроен по-медвежьи по отношению и к тем и к другим. И 10-year и 5-year вчера оттолкнулись от 200-дневной средней скользящей (200 MA) и теперь должны протестировать 50-дневную (50 MA).

Неопределенность относительно лимита госдолга, также как и его увеличение, которое рано или поздно произойдет, отражается негативно на US bonds и долларе.

Если взглянуть на график, то хорошо видно, что с начала года 10-year US bonds торгуются в диапазоне доходности 3,1-3,6%. Очень вероятно, что вчера они оттолкнулись от нижнего края этого диапазона. Как бы это не было непатриотично с их стороны, но здесь на нижней границе слишком много сильных игроков (PIMCO, Джим Роджерс, теперь еще и GS) продают и даже шортят US Bonds.

Скорее всего, дело не ограничиться тестированием 50 MA, и в течение месяца-полутора мы увидим доходность опять в районе 3,6%, новые минимумы по индексу доллара и, возможно, новые максимумы по индексу S&P500.

Шансы на то, что коррекция закончилась, на мой взгляд уже больше 50%. Техническим подтверждением станет пробитие в ближайшее время трендовой линии в районе 1342-1345 пунктов по фьючу S&P500.

Сегодня утром вышли очень негативные данные по Японии: ВВП и промышленное производство. Это привело к тому, что азиатские индексы снижаются; но реакция фьючерса S&P500 на это минимальна.

В Европе и Америке на сегодня нет поводов для коррекции и это создает хорошие предпосылки для возникновения трендового дня вверх в рискованных активах.

Власти США и Китая оказывают влияние на Евросоюз, чтобы те скорее решили вопрос с Грецией. Поскольку о полномасштабной реструктуризации и речи не может быть, то таким решением может стать только «мягкая» реструктуризация, или другими словами перепрофилирование долга (увеличение сроков и снижение процентов).

Помехой к такому решению проблемы является отсутствие на переговорах главы МВФ, который сейчас находится в американской тюрьме. После прошения об отставке и его смене вопрос о Греции будет достаточно быстро решен. Это может произойти уже в мае и приведет к новому ралли в евро и рискованных активах.

During the past year, Strauss-Kahn has been a decisive advocate of the bailouts, influential in the Greek emergency through his close relationship with socialist prime minister George Papandreou. Merkel surprised the rest of Europe last year by insisting the IMF play a central role in the bailouts, with the fund putting up a third of the €750bn rescue pot.

Страсс-Кан был решительным защитником помощи Греции благодаря его тесным связям с премьер-министром Греции Джорджем Папандреу ( и тот и другой социалисты). Треть помощи, выделенной Греции, поступает от МВФ. Поэтому присутствие главы МВФ было принципиально важно.

Отсутствие Страсс-Кана помешало принятию решений по Греции.

While Greece was expected to plead for more help last night, no decisions were expected for several weeks. The European commission said new "arrangements" were possible, with the options including a combination of cutting the interest rate on the bailout money, extending the repayment terms and topping up the loans by up to €60bn. But the emphasis in Brussels and EU capitals was on first urging greater austerity on Athens. Papandreou has been told he will have to show convincingly that he is committed to selling off Greek public assets through a radical privatisation programme before the eurozone will return to his rescue.

"We will discuss Greece but not conclusively," said Jean-Claude Juncker, Luxembourg's prime minister and president of the eurozone grouping. "We will be informed by the IMF, the European Central Bank and the European commission and then we will see."

Для выделения нового пакета помощи Греция должна продемонстрировать свои усилия по экономии.

This troika has been in Greece for the past week assessing the government's adherence to the savage programme of spending cuts and is said to be unhappy with what it has found. The next tranche of the bailout, €12bn, is due to be disbursed next month but there are threats it could be withheld.

The threats prompted Greek media reports at the weekend that pensions and teachers' and civil servants' wages could go unpaid next month if the money did not arrive. But eurozone governments have repeatedly emphasised in the past fortnight that Greece will not be allowed to default on its mountain of debt, making it unlikely that the €12bn will be retained.

Если транш в 12 млрд.евро не будет переведен в следующем месяце, то это приведет к невыплате пенсий, а также зарплат учителям и гражданским служащим.

Чтобы не допустить дефолт, эти средства будут с большой вероятностью переведены.

Diplomats in Brussels and German officials made it clear the US and China were stepping up pressure on the EU to resolve the Greek dilemma, exasperated by the mixed signals from European capitals that have led to turmoil on markets and fresh questions about the euro's viability. An emergency, supposedly secret, meeting in Luxembourg 10 days ago of the French, German, Spanish and Italian finance ministers, which sparked a panic about a possible Greek default, was said to have been the direct result of transatlantic pressure.

At meetings of global finance officials in Washington last month, according to diplomats in Brussels, the Americans, Chinese and Canadians voiced their irritation with European indecision and demanded action to calm the markets.

"The US, Canada, and Beijing told the EU: You've got to get this done to stop the speculation," a diplomat said.

Америка и Китай оказывают сильное давление на власти ЕС и требуют решить греческую дилемму.

Вчера заговорили о мягкой реструктуризации греческого долга

A "reprofiling" or "soft restructuring" of bonds held by private investors, defined as a voluntary loan "extension", was floated by Jean-Claude Juncker, Luxembourg's prime minister and president of the eurozone finance ministers, after a Brussels meeting.

However, he stressed that Greece would have to implement further painful welfare and labour reforms, alongside more privatisations, before European leaders would contemplate such drastic action.

"Greece will have to implement huge reforms ... to rapidly privatise many public entities... then we'll have to see whether we can't proceed to a soft restructuring," Mr Juncker said. "I am strictly opposed to a large restructuring."

Пока это оговаривается таким количеством условий, что может не приниматься всерьез. Пока...

His comments exposed deep divisions in Europe over a second Greek bail-out, on top of the original €110bn package. German Chancellor Angela Merkel indicated on Monday she would oppose any "reprofiling", saying: "It would raise doubts about our credibility if we simply were to change the rules in the middle of the first programme." French finance minister Christine Lagarde added: "Restructuring, reprofiling – off the table."

Greek deputy foreign minister Spyros Kouvelis, though, told Reuters his country is willing to engage in talks on a "soft" restructuring. Irish finance minister Michael Noonan went further and called for rates on the bail-out loans to Ireland, Portugal and Greece to be reduced or risk the programmes' "failure".

Заявления Юнкера вызвали большие разногласия среди политиков. Германия и Франция против. Ирландия и Греция – конечно, за.

While Juncker's and Rehn's statements marked a significant shift in official comment on Greece's predicament, there was apparent disagreement among other senior officials about whether such a move was the right thing to do, although that may have reflected the confusing array of phrases used.

"Restructuring, rescheduling -- off the table," French Economy Minister Christine Lagarde said late on Monday, after Juncker had hinted at a "reprofiling" of Greek debt, a way of extending the maturities on its loans without going through a more fundamental restructuring process.

"A restructuring or a rescheduling, which would constitute a default situation, what we would call a credit event, are off the table for me," she said.

European Central Bank governing council member Ewald Nowotny told Austrian radio that a "soft restructuring" was not on the cards, insisting that Greece needed to shore up its finances.

While all EU officials have rejected the idea of a full-on default, they have now introduced at least three terms to refer to the possibility of some alteration in the repayment schedule of Greek debt: restructuring, rescheduling and reprofiling.

From the financial markets' point of view, there may be little difference among them. The manager of a debt fund in the United States joked that the only time he had heard the word "reprofiling" used was in reference to a nose job.

But sovereign debt analysts draw a distinction between restructuring, which involves enforced losses, and "reprofiling," when bondholders are asked to exchange short-term debt for longer-dated bonds with a similar coupon, thereby altering the profile of the yield curve and effectively giving the debtor more time to repay the loan.

If a "reprofiling" or "soft restructuring" is done in coordination with bondholders, rather than forced upon them, it may not trigger a "credit event" and would therefore avoid the prospect of insurance contracts on debt having to pay out.

The repercussions would still be widespread. Around 70 percent of Greek government bonds -- worth around 215 billion euros -- are held abroad, mostly by French, German and American banks and by the European Central Bank.

A "reprofiling" would mean a delay in repayment, which may in turn cause knock-on credit problems.

В то время как официальные лица ЕС отвергают идею полномасштабного дефолта, они применяют по крайней мере три термина относительно изменения условий платежей со стороны Греции: реструктуризацию, изменение графика платежей (rescheduling), и перепрофилирование.

Реструктуризация включает в себя «принуждение» держателей облигаций к потерям. При перепрофилировании ил по другому «мягкой реструктуризации» держателей долговых бумаг просят заменить краткосрочный долг на облигации с большим сроком погашения; при этом меняется форма кривой доходности и заемщику дается больше времени на выплату долга.

Важно, что при этом не происходит «кредитного события», и не приходится выплачивать компенсации по страховым контрактам на долг.

С точки зрения финансовых рынков в этих терминах мало различий. Их интересует, приведет ли это к уходу от риска, насколько затронет крупные финансовые институты, вызовет ли распродажу активов.

Здесь дано простое и понятное объяснение причин, почему возникли проблемы Греции, Португалии, Ирландии:

The weaker countries, on the fringes of the single currency area, have not been able to cope with the disciplines involved in giving up control of their interest rates and their currencies, with the problem going much wider than the three countries – Greece, Ireland and Portugal – that have sought bailouts. Spain's housing boom and bust was the result of the pan-European interest rate being too low; Italy's increasing lack of competitiveness stems from a lack of exchange-rate flexibility.

It was also clear from the outset that the structure of monetary union would result in struggling countries being subjected to deflationary policies. Since the eurozone is not a sovereign state there is no formal mechanism for transferring resources from rich parts of the monetary union to the poor parts. Nor, given language barriers and bureaucratic impediments, is it easy for someone made unemployed in Athens to get a job in Amsterdam. Instead those countries seeking to match Germany's hyper-competitive economy have to cut costs, through stringent curbs on wage increases and fiscal austerity.

С самого начала было понятно, что структура монетарного союза приведет к дефляционному сценарию для отдельных, не самых сильных и дисциплинированных стран. Так как еврозона не суверенное государство, здесь нет механизма передачи ресурсов от богатой части монетарного союза к его бедной части. Речь идет как о финансовых, так и о материальных и людских ресурсах. Попытка выбраться из дефляционной ловушки путем бюджетной строгости никак не может выправить ситуацию.

Прошлой весной запустили первый план оказания помощи Греции (план А). Почему из этого ничего не получилось?

It's not difficult to see why this has happened. Those who put together Greece's programme underestimated the extent to which public spending cuts and tax increases would hamper the growth potential of the economy, particularly given the lack of scope for the currency to fall. Historically the IMF's structural programmes for troubled developing countries have involved devaluation, so exports became cheaper; but Greece's membership of the single currency has meant there has been no external safety valve to compensate for the domestic squeeze.

Greece needs to have the scope to grow its way out of its debt crisis. Failing that, the rest of the eurozone has to be prepared to stomach not just a second, but a third and perhaps even a fourth bailout so Athens can keep up with its debt repayments. Hence the drumbeat of speculation that Greece would be better off defaulting, or leaving the eurozone altogether.

Девальвация национальной валюты всегда являлось основным средством борьбы с кризисом, подобным греческому. Но в данном случае членство в союзе с единой валютой лишило Грецию возможности компенсировать сжатие экономики открытием клапана, связающего ее с мировой экономикой.

Теперь хотят запустить план В – реструктуризация или перепрофилирование. Но и тот и другой не решит проблем.

There is no suggestion that the Greek government is planning anything of this nature. Default and devaluation pose big risks, particularly since the debts would have to be in a redenominated currency (like the drachma) that creditors would deem to have junk status. In the short term, Greece's economic and financial crisis would almost certainly deepen. Athens would prefer the EU to provide a second bridging loan and to reschedule its debts over a longer period so the interest payments become less onerous.

But that is at best a stopgap solution, because it does nothing to address the structural weaknesses of the eurozone. For this, there are really only two solutions. The first is to turn monetary union into political union, creating the budgetary mechanisms to transfer resources across a single fiscal space. That would fulfil the ambitions of those who designed the euro, and would recognise that the current halfway house arrangement is inherently unstable.

The second would be to admit defeat by announcing carefully crafted plans for a two-tier Europe, in which the outer part would be linked to the core through fixed but adjustable exchange rates. Neither option, it has to be said, looks remotely likely, although the collapse of Lehmans shows the limitations of the current muddling-through approach.

Никакая реструктуризация не решает проблемы структурных различий еврозоны.

Автор статьи видит два способа решить проблему Греции, ни один из которых не устроит европейскую элиту.

Первый: превратить монетарный союз в политический: создать механизм перемещения ресурсов

Второй: признать поражение путем объявления о создании двухслойной Европы, в которой внешний слой был бы связан с ядром с помощью регулируемого обменного курса.

Вчерашние данные статистики в США не стимулировали покупки акций. Первые три часа шли активные распродажи и S&P500 сделал очередной минимум (1318,5). Однако к концу сессии S&P500 почти вернулся к закрытию предыдущего дня, нарисовав таким образом разворотную модель под названием «молот».

Наиболее успешен среди американского рынка акций был банковский сектор (филадельфийский индекс банковского сектора BKX показал 1,65%). Вчерашний день был самым успешным торговым днем для акций банков с начала марта. После вчерашнего сильного толчка теперь индекс BKX обязан как минимум протестировать 50-дневную скользящую среднюю (+2,2%). Дальнейшее движение индекса банковского сектора покажет нам дальнейшую тенденцию. Банковский сектор часто является опережающим индикатором всего рынка. Есть определенные шансы, что коррекция на этом закончилась и рынок на ближайшие недели перейдет в боковое движение.

Dow был менее успешен, чем S&P500, и показал снижение в 0,55%. И тот, и другой американские фондовые индексы тестировали вчера 50-дневную скользящую среднюю, но закрылись выше ее.

Для приостановки движения вниз сейчас появилось несколько позитивных фундаментальных факторов.

Первый – азиатский, из Китая. Китайские официальные лица в последнее время все чаще говорят о том, что инфляцию удалось побороть, и цикл повышения процентной ставки и резервных требований закончился. Главное, что практически прекратился рост цен на недвижимость, а в крупных городах они даже снижаются (в марте в Пекине и Шанхае был настоящий обвал цен).

Второй фактор: вчера закончился неудачей очередной раунд переговоров по бюджету между американцами и демократами. Это является негативным для доллара: индекс доллара сегодня снижается третий день подряд и это тоже способствует возврату аппетита к риску.

Теперь переговоры возобновятся более чем через месяц - в конце июня и у законодателей будет всего 1,5 месяца на то, чтобы прийти к соглашению и увеличить лимит госдолга до 2 августа. Не факт, что это им удастся и технический дефолт по госдолгу США не выглядит таким уж невозможным.

Третий фактор: вчера официальные представители Евросоюза впервые заговорили о возможности мягкой реструктуризации для Греции. Мягкая реструктуризация предусматривает небольшое списание долга Греции и продление сроков погашения других ее обязательств. Важно, что многими игроками на валютном рынке подобный вариант решения греческой проблемы теперь стал рассматриваться как позитив для еврозоны и евро.

Все это естественно призвано не решить реальные проблемы, а всего лишь слегка загасить недовольство и волнения внутри страны

Не зря позавчера «смотрящий за рынком» Goldman Sachs выдал новые рекомендации: рост eurousd и возврат к покупке рискованных активов. Учитывая их влияние на монетарные власти США, скорее всего сейчас те оказывают влияние на власти ЕС и Германии с целью временного решения греческой проблемы.

Ожидаю, что начавшийся вчера отскок продолжится сегодня и и завтра по крайней мере до начала американской сессии. Дальнейшее будет зависеть от развития ситуации вокруг Греции. Пока реструктуризации мешает главным образом позиция Германии. Если Ангела Меркель перестанет противиться реструктуризации греческого долга, и переговоры начнутся, то это вызовет новое ралли евро и рискованных активов.

Сейчас много информации проходит по Греции: как будет проходить возможная реструктуризация, какие последствия будет иметь для еврозоны, банковской системы и т.д. Возможно кому-то это окажется полезным, поскольку на следующей неделе эта тема будет в центре внимания (уже в понедельник состоится встреча министров финансов ЕС).

Здесь подборка информации на эту тему на английском языке, кое-где с комментариями на русском.

Руководство Рубини по реструктуризации греческого долга

The path of Greek public debt is manifestly unsustainable. Fiscal austerity and structural reforms are necessary but will not suffice. In the best-case scenario—incorporating a 10% of GDP fiscal adjustment and structural reforms—Greek public debt to GDP peaks around 160% before “stabilizing.” It is more likely that the debt ratio will exceed 160% and, left untended, will render market access both before and even after 2013 severely limited (or effectively non-existent).

There are multiple approaches to an orderly debt restructuring, with varying degrees of debt relief for the sovereign, additional official financing and systemic risk for the eurozone (EZ). We assume only domestic public debt—95% of the public debt stock—would be restructured.

In our view, the best approach for all stakeholders is akin to a Brady par bond option, an exchange offer in 2011 with potentially significant maturity extension, no face-value reduction and moderately reduced coupons. The public debt would remain very high but would be more sustainable as refinancing risk and the interest bill would be cut. We also suggest variations on this theme that would affect the balance of interests of Greece and private and official creditors.

Credit enhancements—as in the Brady bonds—may or may not be added to act as sweeteners for rating- or capital-constrained creditors like banks, subject to a key caveat: Principal collateral would be expensive, given the large nominal stock of debt and prevailing low interest rates on “risk-free” public debt. It is not yet clear what the source of funding for any substantial principal collateral would be, short of a transfer from other EZ member-states, or more official lending.

Greece’s debt problem is a globally systemic pivot: All stakeholders—Greece, the EZ and indeed all global financial markets—are better served by a pre-emptive and orderly, market-oriented debt exchange rather than sticking with a misbegotten and clearly failing Plan A ... The current approach, Plan A, in effect bails out private creditors who exit early or have short maturities, but exposes continuing creditors, by extension the reputation of the debtor and EZ and global financial stability to three rising risks: Subordination as the debt is transferred to increasingly senior creditors like the IMF, EFSM/EFSF/ESM and ECB; the rising threat of a disorderly outcome as an unsustainable fiscal adjustment, far from enhancing debt payment or carrying capacity, actually undermines it; and the risk of a vicious circle among the PIIGS, the EZ and indeed the whole world, which remains under the gun of renewed contagion when market consensus flips from bailout to get-out mode. Indeed, repeated market experience bears this view out in other cases and in Greece/EZ PIIGS to date.

На рисунке показаны варианты реструктуризации

Базовая идея при выборе между пунктами меню – найти такое «решение», при котором можно было уменьшить долговую нагрузку на Греции без чрезмерного замутнения финансовой системы

The basic idea in choosing between that table menu of options is to find a ‘solution’ to the Greek problem by significantly cutting the Hellenic Republic’s debt burden without excessively roiling the financial system. Remember Greek banks hold plenty of Greek debt, and may be on the hook for CDS payouts, while private investors are notoriously skittish when it comes to burdensharing or subordination.

Roubini’s preferred option — a Brady-esque exchange, or ‘Option 3′ in the above table — would involve exchanging old debt for new bonds with the same face value as the old ones, but with a longer maturity and lower interest rates (no haircuts here, folks). This, he says, could be done through Greece introducing new domestic laws to change the terms of its existing (domestically-issued) debt — something Roubini figures could trigger CDS and would be a very “market-unfriendly” approach. Alternatively, Greece could aim for a voluntary Greek debt restructuring that wouldn’t trigger CDS. There’s a third option involving Greece borrowing collateral from the likes of the IMF or various eurozone bailout programmes to offer credit enhancement to sweeten the exchange deals too.

So Option 3 subdivided into Option 3(a) 3(b) and 3(c).

Intriguingly, there’s also the prospect of a combination of those options 3(a) plus 2, or whatever:

Also, note that Options 3a and 3b—a par bond—are not incompatible with Option 2—a discount bond. As in the Brady plan, there are some investors who mark-to-market (hold the debt in their “trading book”)—usually hedge funds and other alternative asset managers—and there are some investors—banks, pension funds, insurance companies—who don’t mark-to-market as they—at least in principle—hold the debt to maturity and/or in the “banking book”. Thus, as in the Brady plan, offering a menu of options—a discount bond for “mark-to-market” investors and a par bond for “hold-to-maturity” investors—makes sense. One group would prefer a discount bond and the other a par bond. And as is well known, on a [net present value] basis, a properly designed par bond is equivalent to a discount bond.

The ECB bought a large amount of Greek government bonds through its Securities Market Program. Our colleagues in Euro rates research estimate that the ECB bought around €40bn of Greek government bonds with €50bn of notional value, assuming an average purchase price of 80% to par. But the ECB has an even bigger exposure to Greece through its lending to Greek banks.

Greek banks had borrowed €91bn from the ECB as of the end of February with collateral of €144bn. What does this collateral consist of? $48bn is Greek government bonds held by Greek banks on their balance sheet. €55bn consists of government-guaranteed bonds issued by Greek banks, €25bn of which was only issued at the end of last year for the Greek banks to meet new more punitive collateral requirements by the ECB. €8bn is zero-coupon bonds which the Greek government had lent to Greek banks in 2008. The remaining €33bn is likely to be Greek ABS/covered bond collateral. The Greek government agreed earlier this year to extend state-guarantees to Greek banks by another €30bn, but it appears that this new aid package has not been used by Greek banks. All this analysis suggests that 77% of the collateral that Greek banks posted with the ECB is government or government-guaranteed, which would be directly affected in the hypothetical scenario of a Greek debt restructuring. In addition, the remaining 23% of ABS/covered bank bond collateral would almost certainly be affected in the case of a Greek debt restructuring as the solvency of Greek banks would become an issue.

In total, the notional ECB exposure to Greece amounts to around €50bn + €144bn = €194bn. Against this notional exposure, the ECB has lent/invested €40bn + €91bn = €131bn or 68% of its notional exposure. These calculations imply that in a hypothetical case of a Greek debt restructuring, the ECB is protected for a haircut of up to 32%. Beyond that cushion, the ECB is exposed to losses. A hypothetical haircut of 50% would create losses of around €35bn for the ECB.

The Eurosystem has experienced losses on refinancing operations in the past during the Lehman crisis as 5 banks defaulted on their repo operations. The losses incurred by the Eurosystem are to be shared by all national central banks in proportion to their shares in the ECB’s capital. The Eurosystem has €81bn of capital and reserves currently, enough to withstand even a 50% Greek debt haircut. But it would be a lot more problematic for the ECB if other countries such as Ireland had to restructure. The exposure of the ECB to Ireland is similarly big but likely with a smaller cushion. The total exposure of the ECB to Ireland consists of around €20bn of bond purchases and €83bn of repos with domestic Irish banks. This excludes around €67bn of ELA lending which represents an exposure for the national central bank rather than the Eurosystem as a whole. But if domestic Irish banks had to replace their ELA borrowing with ECB borrowing over the coming months, the total exposure of the ECB to Ireland would rise to €170bn, well above of that of Greece.

Greek banks own €49bn of Greek bonds. Their equity amounts to €29bn. The market value of their equity is €12bn, suggesting that the market is already pricing in a loss of €17bn or 35%. A hypothetical haircut of 50% on Greek government debt would create losses of around €25bn, leaving only €4bn of equity (or 1% of assets) for the Greek banking system. But the losses for Greek banks would be much smaller if a Greek debt restructuring were to take place in mid 2013. The average maturity of their Greek government bond holdings is 5 years and roughly €10bn matures every year. By mid 2013, their Greek government bond holdings will drop to €25bn, i.e. half of their current holdings.

The central Bank of Greece held directly €7bn of Greek government bonds as of the end of February. A hypothetical haircut of 50% on these bond holdings would wipe out its entire capital and reserves of €3bn.

Greek social security and other public entities hold around €30bn notional of Greek government bonds. They have already applied a loss of 30% in these holdings. A hypothetical haircut of 50% would create additional €6bn of losses vs. current financial assets of €31bn.

European banks hold €50bn of Greek government bonds according to Q3 2010 BIS data. Even a 50% hypothetical haircut would be manageable. But it becomes more problematic when ones looks at the total exposure of European banks to Greece, including private sector loans, repos, guarantees and credit commitments. These private sector claims are also likely to suffer in the case of a Greek debt restructuring. According to BIS, European banks’ total exposure to Greece was €165bn at the end of Q3 2010, driven by French banks (€68bn) and German banks (€50bn). The potential losses for European banks would be more threatening if other countries such as Ireland were to restructure. According to BIS, European banks’ total exposure to Ireland (both public and private sector exposure) was €450bn at the end of Q3 2010, driven by British banks (€165bn), German banks (€150bn) and French banks (€57bn).

Неудивительно, что банки так сопротивляются идее списания по бондам.

Притом больше их волнует даже не сам Греция ( с ней и так все ясно), сколько перспектива запуска подобных реструктуризаций в других странах.

Ситуация вокруг Греции опять осложнилась, это привело к укреплению доллара и новой серии продаж рискованных активов.

В Афины приехала представительная делегация от ЕС и МВФ, чтобы изучить ситуацию на месте и решить вопрос о новом пакете помощи. Вчера в Греции также состоялась всеобщая забастовка, в которой граждане страны протестовали против навязываемой им помощи, которая по мнению профсоюзов «душит» экономику.

Реструктуризация все-равно представляется маловероятной. Хотя очень многие не только в Греции, но и в еврозоне думают также, как и Тимо Соини, председатель Партии истинных финнов (http://mfd.ru/blogs/posts/view/?id=192). Помимо официальных властей еврозоны и Германия и Франция тоже выступают за новый пакет помощи.

10-летние греческие облигации торгуются с доходностью 15,7%, что соответствует примерно 55% их стоимости. Это примерно та величина списания греческого долга, которую необходимо принять во время реструктуризации. Но «друзья» Греции из Евросоюза усиленно навязывают помощь Греции, чтобы оттянуть насколько можно неминуемый дефолт и тем самым уменьшить потери втянутых в эту историю банков.

Скорее всего переговоры о помощи Греции продлятся до конца недели, и какое-то решение возникнет на выходных или в понедельник, когда состоится встреча министров финансов ЕС. Там же будет решаться вопрос и Португалией.

Возможно, что до этого момента мы увидим на рынках продолжение движения вниз. S&P500 может скорректироваться в район 1310-1315 пунктов, а eurousd может скорректироваться ниже 1,40. Затем, возможно, последует краткосрочный отскок вверх.

Вслед за металлами биржи стали поднимать гарантийное обеспечение на нефть (CME подняла на 25%, и возможно оно не станет последним), и это тоже способствует коррекции. То, что это происходит именно сейчас и настолько энергично, наводит на определенные мысли о спланированности этих действий.

Среднесрочно:

На следующей неделе будет достигнут лимит госдолга США, но за счет экстремальных мер Казначейства наступление дефолта отсрочено до начала августа. Переговоры о бюджете опять зашли в тупик и предположу, что какое-то решение будет найдено только в середине-конце июля. А до этого момента среднесрочно коррекция продлится и ожидаю, что большую часть времени рынок проведет в боковике в диапазоне 1250-1340 пунктов по S&P500.

US Treasuries вчера возобновили рост: тенденция, которая тоже будет способствовать уходу от рискованных активов.

Важнейшей новостью вчера стали не nonfarm payrolls, а статья в Шпигеле, раскрывшая миру секрет о том, что Греция собралась выйти ез еврозоны, намеревается ввести собственную валюту и что переговоры о реструктуризации долгов Греции вот-вот начнутся.

Кризис в Греции принял драматический оборот.

Основные тезисы:

Проблемы Греции столь огромны, а антиправительственные выступления проходят почти каждый день, что премьер-министр Папандрео по-видимому решил что другого выхода не остается.

SPIEGEL ONLINE из германских правительственных источников получил информацию о том, что Греция рассматривает вопрос о выходе из еврозоны и введении своей собственной валюты.

Несколько ключевых министров финансов еврозоны и представителей ЕС соберутся в пятницу ночью в Люксембурге на секретную встречу.

Помимо желания выйти из еврозоны, министры будут обсуждать возможную реструктуризацию греческих долгов.

Германский министр финасов намерен отговорить Грецию от этого шага. В статьи перечисляются последствия, к которым это приведет.

К сожалению у нас редко оперативно осуществляют переводы столь важных документов, поэтому приходится его давать на английском языке: все-таки английский у нас знает гораздо больше читателей, чем немецкий.

And the original version of the article in native English:

The debt crisis in Greece has taken on a dramatic new twist. Sources with information about the government's actions have informed SPIEGEL ONLINE that Athens is considering withdrawing from the euro zone. The common currency area's finance ministers and representatives of the European Commission are holding a secret crisis meeting in Luxembourg on Friday night.

Greece's economic problems are massive, with protests against the government being held almost daily. Now Prime Minister George Papandreou apparently feels he has no other option: SPIEGEL ONLINE has obtained information from German government sources knowledgeable of the situation in Athens indicating that Papandreou's government is considering abandoning the euro and reintroducing its own currency.

Alarmed by Athens' intentions, the European Commission has called a crisis meeting in Luxembourg on Friday night. In addition to Greece's possible exit from the currency union, a speedy restructuring of the country's debt also features on the agenda. One year after the Greek crisis broke out, the development represents a potentially existential turning point for the European monetary union -- regardless which variant is ultimately decided upon for dealing with Greece's massive troubles.

Given the tense situation, the meeting in Luxembourg has been declared highly confidential, with only the euro-zone finance ministers and senior staff members permitted to attend. Finance Minister Wolfgang Schäuble of Chancellor Angela Merkel's conservative Christian Democratic Union (CDU) and Jörg Asmussen, an influential state secretary in the Finance Ministry, are attending on Germany's behalf.

'Considerable Devaluation'

Sources told SPIEGEL ONLINE that Schäuble intends to seek to prevent Greece from leaving the euro zone if at all possible. He will take with him to the meeting in Luxembourg an internal paper prepared by the experts at his ministry warning of the possible dire consequences if Athens were to drop the euro.

"It would lead to a considerable devaluation of the domestic currency against the euro," the paper states. According to German Finance Ministry estimates, the currency could lose as much as 50 percent of its value, leading to a drastic increase in Greek national debt. Schäuble's staff have calculated that Greece's national deficit would rise to 200 percent of gross domestic product after such a devaluation. "A debt restructuring would be inevitable," his experts warn in the paper. In other words: Greece would go bankrupt.

It remains unclear whether it would even be legally possible for Greece to depart from the euro zone. Legal experts believe it would also be necessary for the country to split from the European Union entirely in order to abandon the common currency. At the same time, it is questionable whether other members of the currency union would actually refuse to accept a unilateral exit from the euro zone by the government in Athens.

What is certain, according to the assessment of the German Finance Ministry, is that the measure would have a disastrous impact on the European economy.

"The currency conversion would lead to capital flight," they write. And Greece might see itself as forced to implement controls on the transfer of capital to stop the flight of funds out of the country. "This could not be reconciled with the fundamental freedoms instilled in the European internal market," the paper states. In addition, the country would also be cut off from capital markets for years to come.

In addition, the withdrawal of a country from the common currency union would "seriously damage faith in the functioning of the euro zone," the document continues. International investors would be forced to consider the possibility that further euro-zone members could withdraw in the future. "That would lead to contagion in the euro zone," the paper continues.

Banks at Risk

Moreover, should Athens turn its back on the common currency zone, it would have serious implications for the already wobbly banking sector, particularly in Greece itself. The change in currency "would consume the entire capital base of the banking system and the country's banks would be abruptly insolvent." Banks outside of Greece would suffer as well. "Credit institutions in Germany and elsewhere would be confronted with considerable losses on their outstanding debts," the paper reads.

The European Central Bank (ECB) would also feel the effects. The Frankfurt-based institution would be forced to "write down a significant portion of its claims as irrecoverable." In addition to its exposure to the banks, the ECB also owns large amounts of Greek state bonds, which it has purchased in recent months. Officials at the Finance Ministry estimate the total to be worth at least €40 billion ($58 billion) "Given its 27 percent share of ECB capital, Germany would bear the majority of the losses," the paper reads.

In short, a Greek withdrawal from the euro zone and an ensuing national default would be expensive for euro-zone countries and their taxpayers. Together with the International Monetary Fund, the EU member states have already pledged €110 billion in aid to Athens -- half of which has already been paid out.

"Should the country become insolvent," the paper reads, "euro-zone countries would have to renounce a portion of their claims."

Все, что здесь написано, звучит очень сильно и тревожно.

Последовали многочисленные официальные опровержения, но факт остается фактом: нет дыма без огня. Шпигель не стал бы распускать столь беспочвенных слухов.

Рынки уже отреагировали на эту новость. Евро снизился на две фигуры относительно доллара, S&P500 тоже развернулся и до закрытия успел пройти 20 пунктов вниз.

Интересно, что все почти в точности повторяется, как в прошлом году. Тогда тоже в мае разразился греческий кризис и ей потребовалось оказание помощи.

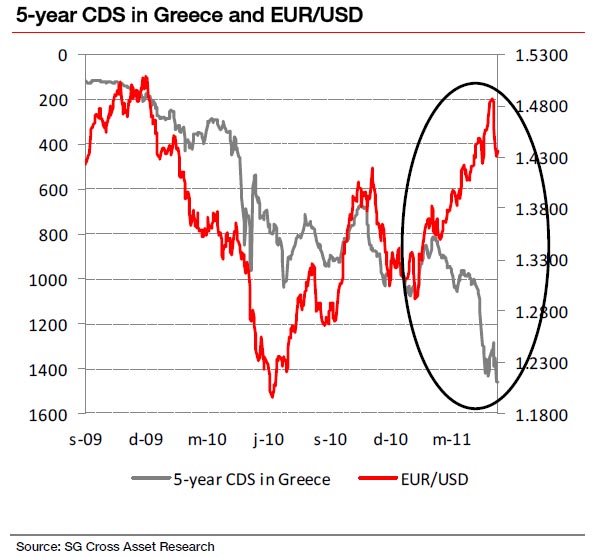

Обращает на себя внимание очень сильная дивергенция, которая возникла в последнее время между евро и оценкой рисков неплатежеспособности ( CDS Греции, да и других PIIGS). Если раньше они относительно хорошо коррелировали между собой, то теперь графики просто разошлись совершенно в разные стороны. На мой взгляд, это говорит о том, что выход Греции уже не рассматривается как риск для дальнейшего существования еврозоны. Загнанных лошадей пристреливают, не правда ли...

Несомненно выход из еврозоны будет иметь драматические последствия для самой Греции и поэтому маловероятно, что она это сделает это по собственной воле.

Для этого есть следующие доводы:

В настоящий момент Греция хорошо обеспечена ликвидностью до 2013 года, имеется еще 83 млрд. евро в фондах ЕС и МВФ, зарезервированных под Грецию.

Помимо всего прочего ¼ долга (это на самом деле немало) сосредоточено внутри страны: социальная защита (28 млрд. евро), банки ( 31 млрд.) и даже домашние хозяйства держат 6 млрд. евро греческого долга.

Поэтому скорее всего речь на переговорах пойдет о реструктуризации.

Будем следить за тем, что будет дальше. Читайте комментарии...

Вчера днем было довольно сильное падение евро, которое, правда, во второй половине дня было выкуплено.

Оно было связано с заявлениями министра финансов Германии Вольфганга Шойбле по поводу Греции, которое участники рынка восприняли как угрозу реструктуризации долгов страны.

April 14 (Bloomberg) -- German Finance Minister Wolfgang Schaeuble said Greece may have to seek debt restructuring if an audit in June questions its ability to pay creditors, Die Welt reported, citing an interview.

Greece would have to negotiate to ease its debt burden since creditors can’t be forced to take losses until Europe’s permanent rescue system for the euro starts up in mid-2013, the Berlin-based newspaper cited Schaeuble as saying in comments published today.

“We will have to do something” if the review by the International Monetary Fund and European authorities in June raises doubts about Greece’s “debt sustainability,” Schaeuble was quoted as saying. “Then, further measures will have to be taken.”

Вот как прокомментировал это заявление Gary Jenkins на Evolution Securities

Greek bonds are getting crushed today due to the comments from the German finance minister and the Greek equivalent. The ESM allows a roadmap towards restructuring, indeed it insists upon it if debt cannot be restored to a sustainable path. Whilst in the first instance any such restructuring from Greece may involve extension of maturities / coupon forgiveness ultimately we believe that if the idea is to get the debt back to a sustainable level then the target will be the Maastricht treaty limit of debt / gdp of 60%. In order to reach that level bonds will have to take a haircut of some 62%. Thus whilst the 10 year bonds have cheapened up considerable and now yield over 13% for the first time, the fact is that at a cash price of 64.6 they still have the potential to fall a long way...Whilst there is a step down in price once you get past the 13’s (on the basis that the latter would be expected to be more likely to be safe as they pre-date the ESM) one wonders if Greece will even get that far before they enter into “voluntary” discussions...

А это комментарий аналитиков BNP Paribas

The Greek restructuring story is somewhat puzzling, even resembling a Gordian knot. Credit markets traded nervously on Thursday, on concerns that a potential Greek debt restructuring could happen sooner rather than later. These were caused by German Finance Minister Schaeuble’s comments reported by Reuters. “In June we will get a progress report. I’m expecting a detailed analysis on the debt sustainability of Greece, that will be done in consultation with the Commission and the ECB. If this report concludes that there are doubts about the debt sustainability of Greece, something must be done about it.” As well as “until then [2013] a restructuring could only take place on a voluntary basis.”

Появились опасения, что реструктуризация долгов Греции произойдет уже летом этого года