Вчера мы видели в действии один из современных приемов монетарной политики, который называется «Вербальные интервенции».

...на позитивных данных с рынка труда рынки растут. Затем, когда говорят, что эти данные не отражают реального положения дел, рынки опять растут. Не абсурд ли это?

Нет, это не абсурд. Это прием монетарной политики.

Это называется вербальной интервенцией – словесное обещание сделать что-либо, которое заменяет реальное действие.

Между прочим, еще осенью 2010 года глава ФРБ Нью-Йорка Уильям Дадли говорил о таком приеме монетарной политики в своей речи – читал об этом непосредственно в «первоисточнике».

На мой взгляд, выступление Бернанке нужно трактовать противоположным образом тому, как это сделали рынки. Но не я формирую рыночные рефлексы. Их формирует Goldman Sachs – «доктор Павлов» современных финансовых рынков.

Уильям Дадли – кстати, бывший главный экономист этого учреждения.

Нужна ли была вербальная интервенция в том случае, если бы впереди нас ждала реальная? Думаю, что нет.

Тогда бы первичные дилеры сидели бы и тихо скупали активы. На перспективном бычьем рынке не нужно устраивать выносы по искусственному поводу.

С утра Азия продолжает покупать риск, но на рискованных валютах это не отражается, нет и привычной покупки EURO в таком случае. Продаж, правда, тоже нет. Рынки как будто ждут сигнала – куда дальше.

Говорят, что конец квартала стимулирует покупки активов? Но почему он должен стимулировать покупки, если и так все выросло очень прилично?

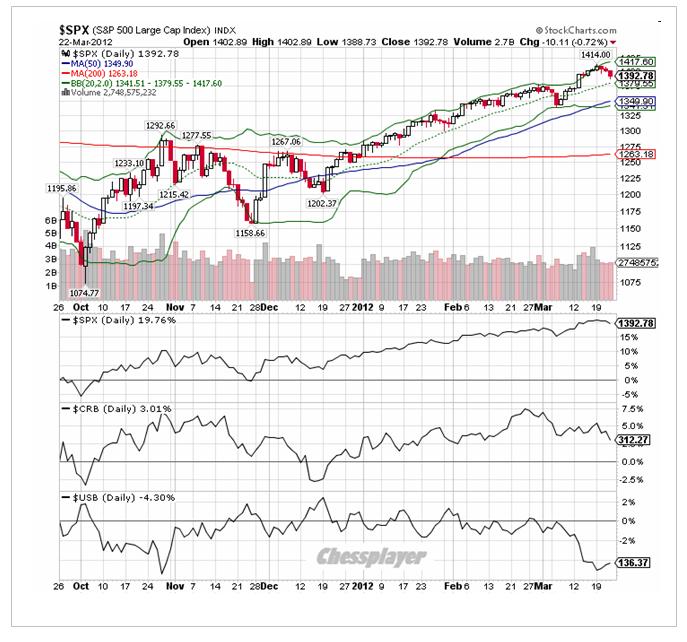

Ну что сказать, амеры реализовали вчера ту самую малую вероятность для роста в 5%, упомянутую нами, и обновили хаи года, в очередной раз выкупившись от 1392. Выперли вверх невзирая ни на что, ни слова уже про плохое ни в одном СМИ - ни про грецию, ни про "испанию и прочие румынии", ни про амерский госдолг, про новый фискальный евросоюз вообще ни слова, только елейные и в то же время путаные выступления Бернанке, мол "как быстро сокращается безработица, быстрее восстановления экономики)), хотя конечно, это может быть вследствие ошибок в статистике")). Плюс какой-то странный намек на новые стимулы от ФРС, что многие восприняли как слово о КУ-3... И выступать стал три раза в неделю, какой-то чес по стране пошел)). На этом фоне опять подросли и банки и эппл, ну что на это сказать, мощные три месяца роста у амеров, каждый раз когда все уже повисает на резинке от трусов, приходит дядя-слон и решительно спасает свое чадо от наказания сторожа, снимая воришку с забора. Если не обращать внимание на тренд, то по идее сегодня консолидация у достигнутых уровнях, вокруг 1415, а потом снова развилка. Если эту неделю удастся закрыть в нуле или минусе, то и следующая будет падучей, но пока не видно, на чем и кто сыграет наконец амеров вниз. Понятно, что ситуация ненормальная, американских трейдеров прозомбировали, так что пока сам инициатор тренда не ливанет, видимо, продавцы не появятся.

Нефть на 125, азия прирастает прежде всего японцами)). В целом идет конечно тотальное принуждение к росту, даже немцы уже стали отставать от амеров, не понимая, что происходит, ну не могут рынки не выдыхать.

Наши вчера вполне спокойно стояли, даже отбивку в минус по мамбе сделали, но увидев как амеры рванули сквозь 1400, вышли вверх, причем даже не достали 1570, откуда снова начали фикс. Через меру полезли только в суры и сберы, рыночные афродизиаки этого года, остальное торговалось вполне аккуратно и на небольшие объемы, то есть никто себя в лонги не засаживал. Какая будет реакция на новые хаи амеров? видимо снова окажемся в зоне 1576-86 (примерно +1.5% по мамбе), зона старых сопротивлений, а дальше непонятно, по нашему рынку было видно, что покупать выше 1600 мало кто хочет, ибо 1700 в этом году под большим вопросом. По идее и сейчас все также и ничего не изменилось, покупать надо на 1200 по мамбе в этом году, а не выше 1600. Но это если не появятся новые свежие и крупные деньги. Шорт пока не увеличиваем, скорее всего новая порция продаж пойдет завтра. Немного обидно, что наших мишек так подвели амеры, но с другой стороны, амеры явно выращивают черного лебедя, надувая свой пузырь, так что лонги все равно опаснее шортов, и все равно на шорты дадут много меда,больше профита, чем на лонги в итоге, когда мамба придет на 1200-1300.

Вчера ведущие фондовые индексы Америки обновили свои четырехлетние максимумы. На рынке просто не стало продавцов, когда глава ФРС Бен Бернанке, заявил, что в целях снижения уровня безработицы и более быстрого экономического роста стимулирующая денежно-кредитная политика должна сохраняться. То есть уверенность игроков в том, что дешевая ликвидность не уйдет с рынков в обозримой перспективе, создала предпосылки для повышения спроса на рискованные активы. На деле же экономика США не развивается столь бурными темпами, как ее фондовый рынок. Вчерашняя статистика – лишнее тому подтверждение: индекс подписанных, но неоплаченных договоров по продаже существующих домов в феврале показал снижение на -0,5% м/м против прогноза +1,0% м/м; в марте индекс деловой активности в обрабатывающей промышленности ФРБ Далласа составил лишь 10,8 п. против прогноза 16,0 п. Как бы то ни было, но вчера мы видели равномерный рост по всем секторам рынка на американских биржах.

Курс евро вчера существенно укрепил свои позиции против доллара на фоне последнего выступления главы ФРС, в котором он заявил о приверженности мягкой аккомодационной политике в Америке. Напротив, представители ЕЦБ вчера намекнули о возможности сворачивания программ долгосрочного кредитования европейского банковского сектора. К утру вторника пара EUR/USDподнялась и стабильно торгуется возле отметки 1,3360. Азиатский рынок акций пассивным ростом (MSCIAsia+1,68%) отреагировал сегодня на продолжение ралли на Уолл-стрит.

Во вторник мы ожидаем увидеть нейтрально-позитивное начало торгов на российских фондовых биржах. Вчера индекс ММВБ приблизился к сильному сопротивлению на 1570 п. Думаю, сегодня будут ждать торги в фазе консолидации. Почему? Еще вчера за 1,5 часа до закрытия сессии было видно, что покупатели ослабли, а индекс ММВБ завершил сессию точно на уровне 38% коррекции от падения прошлой недели. Цены на сырьевых площадках сегодня утром не демонстрируют оптимизма (Brent $125,5/барр), равно как основные сырьевые валюты (AUD/USD1,0520) и фьючерс на S&P(+0,05%) после подъема вчерашнего дня сегодня консолидируются. Потолок роста индекса ММВБ на сегодня – 1572 п. Ждать ли снижения в ближайшее время? После хорошего вчерашнего роста на рынках пока не наблюдается внятного коррекционного движения, что говорит об отсутствии продавцов. Возможно, свежая статистика из Европы и США вытолкнет рынки из фазы консолидации. Думаю, как минимум до вечера среды курс рубля к доллару сохранит силу и останется ниже уровня 29 (28 марта пройдет уплата налога на прибыль 150 млрд. руб.).

Сегодня в 10-00 Германия опубликует индекс доверия потребителей Gfk за апрель. В 10-45 во Франции выходит индекс доверия потребителей за март. В 14-00 выходит индекс розничных продаж CBI за март в Великобритании. В 17-00 будет опубликован индекс цен на дома в крупнейших городах США за январь от S&P/Case-Shiller. В 18-00 выходит индекс доверия потребителей за март. В это же время выходит индекс экономической активности ФРБ Ричмонда.

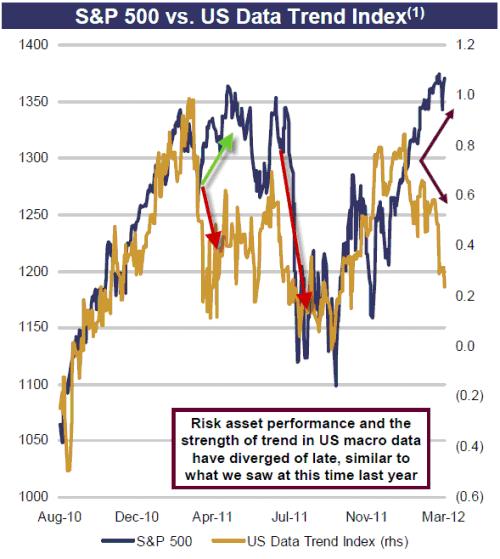

В настоящий момент, когда греческая тема ушла на задний план, а новая европейская (португальская, испанская, ирландская) головная боль пока еще не проявилась, рынки торгуют экономические данные.

Печальные данные по PMI Китая и Европы толкали вчера весь день фондовые индексы вниз. На этом фоне даже меньшие, чем ожидались обращения за пособиями по безработице были проигнорированы.

Американский фондовый рынок третий день подряд закрылся снижением. При этом падение от мартовского максимума пока составляет всего 1,6%. Вчера впервые отметился падением финансовый сектор. Под серьезным давлением находятся сектора рынка, связанные с commodities.

Отметим, что вчера был гэп на открытии – редкий по нынешним временам случай, который так и не был закрыт. Вжное значение будет иметь – закроется ли он в ближайшие пару дней.

Торговый диапазон (ATR) остается прежним – очень небольшим; что в пользу продолжения бычьего ралли.

Как обстоит дело с индикаторами риска: VIX и put/call?

VIX остался в режиме «риск выключен», а вот put/call вырос и оказался на границе бычьего рынка.

Конечно, количество медведей возросло. Но часто на заключительной стадии ралли их используют для того, чтобы придать силу этому ралли.

Индикатор настроений DAX (опрос проводится по средам) показан на рисунке.

Инвесторы на немецком рынке – а в опросах участвуют далеко не «чайники» разделились практически поровну.

На мой взгляд, говорить о том, что мы наблюдаем среднесрочный разворот еще пока очень преждевременно.

Пока это всего лишь коррекция. Вопрос в том – какая она будет?

Окажется ли это падение еще одной микрокоррекцией?

Микрокоррекцией я называю падение в пределах 2-3 %. Или на этот раз будет более существенное падение – порядка 5-8%?

Максимальную цель, которую я определил бы для текущей ситуации это примерно в районе 1320 пунктов.

Увидеть рынок ниже мне представляется маловероятным до начала серьезного потока негативных макроэкономических данных по американской экономике. До 10 апреля такой поток маловероятен.

СИТУАЦИЯ НА РЫНКАХ ОБЛИГАЦИЙ

Goldman Sachs утверждает, что американские казначейские облигации стоят дорого и призывает покупать акции (по-видимому, им очень необходимо разгрузить свой портфель от акций).

На рисунке внизу показана сравнительная динамика движения трех основных классов активов: рынка акций (S&P500), commodities – индекса оптовых цен CRB, рынка казначейских облигаций (30-year US bonds)

Глядя на этот рисунок разве можно сказать, что US Treasuries стоят дорого?. С середины октября S&P500 вырос на 19,76%, а цена на 30-year US bonds упала на 4%.

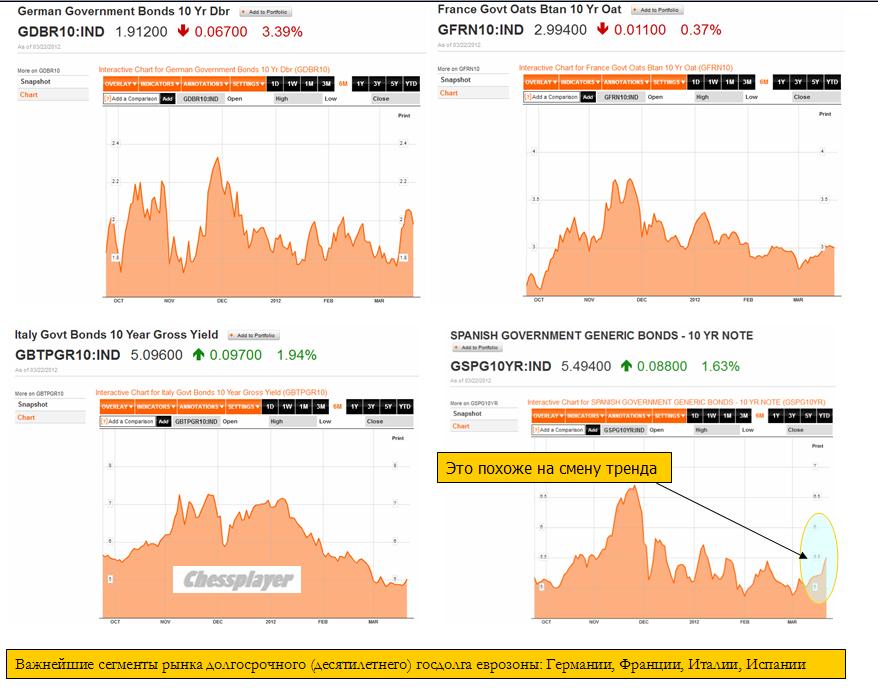

Ситуация с европейским суверенным долгом впервые за последние три месяца ( с начала 3-year LTRO) начинает развиваться в худшую сторону.

На рисунке внизу показана доходность по 10-летним бумагам основных долговых рынков еврозоны.

Как мы видим, доходность 10-year итальянских и испанских бондов поднялась выше 5%, спрэды с германскими растут.

Сильное движение в доходности испанских бумаг говорит о том, что там у них что-то не в порядке.

А не прошло еще и месяца после того, как они получили большую помощь от ЕЦБ в виде 3-хлетних кредитов на поддержание ликвидности.

Напомню, что в случае снижения стоимости облигаций банкам приходится вносить дополнительные залоги в обеспечение взятых в ЕЦБ кредитов.

Также сложная ситуация у Португалии.

Периферийный госдолг еврозоны, по сути, тоже является рискованным активом. И здесь мы видим настораживающие сигналы.

Резюме:

КАК Я ОЦЕНИВАЮ ПЕРСПЕКТИВЫ РЫНКА

Скорее всего, текущая коррекция на следующей неделе разовьется примерно в район 1340-1350 пунктов по индексу S&P500, затем последует новая волна роста. Примерно до 10-20 апреля.

Затем выборы в Греции, во Франции, новые долговые проблемы еврозоны и плохие данные американской экономики могут вызвать уход от риска и коррекцию, которая перерастет в смену тренда.

Но если америкосы «нарисуют» позитивные данные, то бычий рынок может продолжиться вплоть до июня месяца и мы увидим в первом полугодии почти полное повторение сценария прошлого года.

В этом вопросе немцы и так остаются примером для окружающих: еще в середине прошлого года аналитики ждали дефицита по итогам всего 2011 г. на уровне 2% от ВВП, однако по итогам 12 месяцев стало известно, что дефицит составил всего 1%. Уже в 2014 г. планируется сократить дефицит до символического минуса в 0,35%, а к 2016 г. и вовсе выйти на сбалансированный бюджет.

По данным Национального статистического ведомства Великобритании, общий объем государственных заимствований правительства в настоящее время оценивается в 110 млрд фунтов. До конца текущего финансового года остается всего один месяц. По данным независимых аналитиков, за весь фингод уровень госзаймов составит порядка 127 млрд фунтов, однако, учитывая последние данные статистического ведомства, итоговые займы окажутся на 7 млрд фунтов меньше прогнозных значений.

В 2011 г. Россия разместила рублевые еврооблигации на 90 млрд руб. Семилетние евробонды на 40 млрд руб. с доходностью 7,85% годовых размещены в феврале 2011 г., доразмещение этого выпуска на 50 млрд руб. проведено в мае.

Recently O'Neill said oil prices are his biggest concern not Greece. He reiterated the argument that China is creating an economy the size of Greece every 11.5 weeks, and asked: "Who cares about Greece?"

Каждые 11.5 недель Китай создает такую экономику, как Греция.

А вот с этого все началось:

This morning Goldman portfolio strategists Peter Oppenheimer and Matthieu Walterspiler made a bullish case for U.S. equities saying stocks are much cheaper than bonds. Jim O'Neill told CNBC he has been bullish on U.S. equities for a while:

"One is we have really low levels of bond yields, because many including policy makers do not believe things can ever return to normal. And the other one is we have people that don't believe that world growth can do better than it did at point x in the past. Being mister BRIC in reality despite western problems the world economy's growth rate is trending higher than it has been for 30 years of my existence. Put all of that together it is really bullish on equities."

Голдманисты считают, что акции стоят дешево по сравнению с бондами.

В долгосрочной перспективе, может, это правда... Но не в краткосрочной.

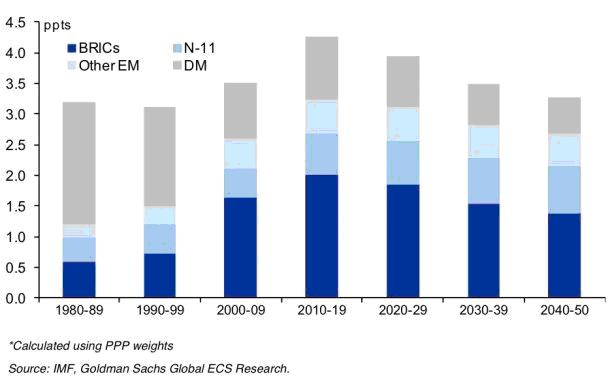

And though you might think that things are slowing down around the world, Goldman argues just the opposite, that the 2010-2019 period has more growth potential than any decade between 1980 to 2050.

Голдман считает, что период 2010-2019 годов имеет потенциал роста больший, чем любая декада с 1980 по 2050.

Sure, developed markets aren't growing as fast as they used to be. And even the BRICs are slowing down. BUT, because the BRICs are so big now, and because the N-11 countries (Bangladesh, Egypt, Indonesia, Iran, Mexico, Nigeria, Pakistan, Philippines, Turkey, South Korea, and Vietnam) are growing so fast, the net effect is that this decade could be a monster.

Вот график фантазий будущего аналитиков Голдмана

Откуда они знают, что будет в 2020-2050 годах? Линейная аппроксимация?

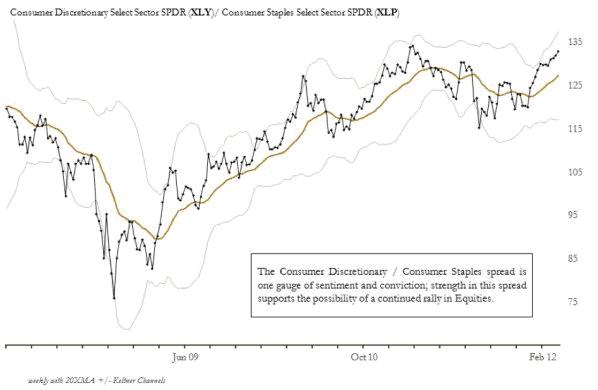

“Historically, the Discretionary/Staples spread has rallied with the broad market; in other words, it is not a leading indicator on rallies. However, it has also historically faltered before major indexes, making it a useful timing indicator and an early warning of trend failure. we see no weakness in this spread at this time.”

Отношение динамики двух секторов Discretionary/Staples американского фондового рынка может служить предостерегающим сигналом близкого разворота.

Как немецкие банки уходят из- под бдительного ока Феда.

Why are we not surprised at the fact, as reported by the WSJ, that Deutsche Bank AG changed the legal structure of its huge U.S. subsidiary to shield it from new regulations that would have required the German bank to pump new capital into the U.S. arm. The bank on Feb. 1 reorganized its U.S. subsidiary, known as Taunus Corp., so that it is no longer classified as a 'bank-holding company' (BHC). The technical change has important consequences.

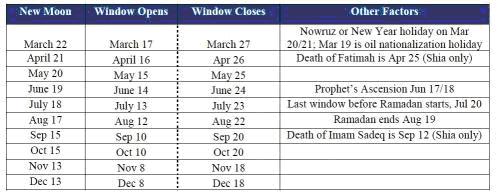

Анализируется, когда Израилю наиболее удобно по времени нанести удар по Ирану

Based on press reports, officials see high odds of an attack sometime between 2Q12 and the end of the year, with most pointing to 2Q or 3Q.

If Israel elects to conduct a conventional military strike, the optimal conditions would be moonless and cloudless nights. “Operation Orchard,” Israel’s attack on Syria’s reactor at Al-Kibar on Sep 6, 2007, took place 5 days before the new moon. This suggests windows starting about 5 days before a new moon and ending five days after - see the table below. Low humidity is also ideal, but not required.

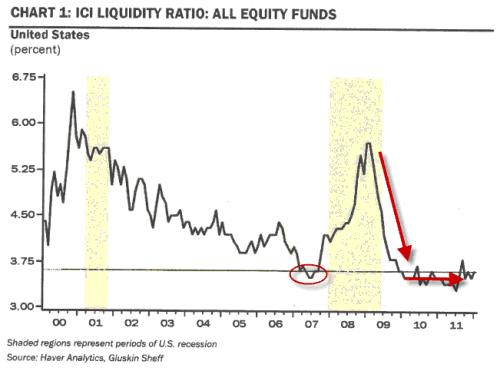

Дэвид Розенберг свидетельствует, что кэш находится вблизи минимальных уровней.

However, as Rosie points out equity fund cash ratios are at a de minimus 3.6%, the same level as in the fall of 2007 and near its lowest level ever. The time when cash was heavy and 'ample' was at the market lows in 2009 when the ratio was very close to 6%. Bond fund managers, it should be noted this includes the exuberant HY funds, are now sitting on less than 2% cash so if retail inflows continue to subside as they did this week, buying power could weaken over the near-term.

Albert Edwards из SocGen ожидает, что ралли в акциях скоро выдохнется и мы еще увидим новые минимумы доходности US Treasuries в этом году.

Albert Edwards explains: 'With bond yields breaking out to the upside and the equity bull run continuing, investors are back to their same old hopeful habits. Many are thinking that if we have seen the all-time lows on bond yields investors will be forced into equities. We already can observe leading indicators rolling downwards in exactly the same way as they did in 2011." And here is why Edwards will once again be unpopular with the permabull, momentum chasing crowd: "Expect new lows on bond yields by Q3 and this equity rally to turn to dust – just as it did in 2011."

Ситуация в европейских суверенных долгах начинает разворачиваться в худшую сторону.

Whether it was the truthiness of Willem Buiter's comments this morning, the sad reality of Spanish housing, or more likely the ugly fact that LTRO3 is not coming (as money-good assets evaporate), today was broadly the worst day of the year for European sovereigns. Spanish 10Y spreads jumped their most since the first day of the year, Italian yields broke back above 5% (and spreads broke back over 300bps), and Belgium, France and Austria all leaked notably wider. Since Friday's close, Italian and Spanish bonds have suffered their largest 2-day losses in over 3 months. Notably the CDS markets rolled their contracts into Monday and perhaps this derisking is real money exiting as they unwound their hedges - or more simply profit-taking on front-run LTRO carry trades but notably the LTRO Stigma has exploded in the last few days back to near its highs. European equity markets are now underperforming credit - having ridden the high-beta wave far above credit markets in the last few months (a picture we have seen in the US in Q2 2011 and HY is signaling risk-aversion rising in the US currently in the same way). Just how will the world react to another risk flare in Europe now that supposedly everything is solved?

Рынок недвижимости Ирландии/Испании не подпадает под категорию «слабый». Он хуже.

After a disappointing home sales print in the US (as the shadow overhang remains heavy), some perspective on just how bad it is in Europe is worthwhile. With Spanish yields starting to blow out again, it likely comes as no surprise that, as Goldman notes, the Spanish housing market (and for that matter the periphery in general) is bad and getting worse. However, Ireland remains the worst of the worst and Goldman sees yet another growing divide between the haves and have-nots of Europe as the residential property price performance can essentially be split into four groups: Strong, Recovering, Weak, and Ireland/Spain; with the latter perceived as considerably worse than the 'reported' data would suggest. Is it any wonder that Spain trades wide of Italy again now and as Citi's Buiter noted earlier, Spain is now the fulcrum market (Spanish 10Y spreads +30bps from Friday's tights).

Здравый смысл – это не то, что свойственно большинству.

As usual, Oaktree's Howard Marks cuts to the chase in his latest memo. Much as we just discussed the seeming complacency and drop in risk perception that currently exists, Marks scoffs at the 'It's Different This Time'-argument noting "there’s sure to be another cycle, another bubble and another crisis. There’ll be another time when people overpay for exciting investment ideas because their future appears limitless, and then a time of disillusionment and price collapse. There’ll be another period when leverage is embraced to excess, and then, consequently, a period when it gets people killed. And there’ll certainly be another time when people can only imagine the possibility of gain, and then one when – after huge sums have been lost – they can think only of further declines." Touching on the extremes of dysphoria and complacency that summarize the herd of global investors, he nails the reality of the crowd: "common sense isn’t common. The crowd is invariably wrong at the extremes. In the investing world, everything that’s intuitively obvious is questionable and everything that’s important is counter-intuitive."

Будет новый цикл, новый пузырь и новый кризис. Толпа неизменно неправа на экстремумах рынка.

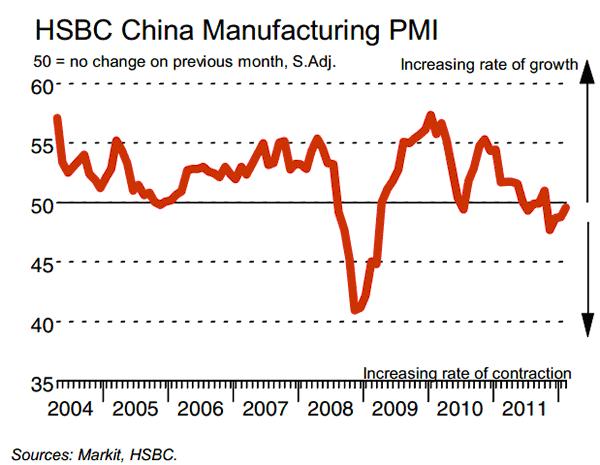

В четверг в 6.30 по Москве выйдет индекс деловой активности в производственном секторе Китая, рассчитываемый банком HSBC – ключ к дальнейшему движению цен на commodities и риску в целом.

Главный китайский фондовый индекс Shanghai Composite и цены на медь уже отражают опасения инвесторов относительно роста китайской экономики.

Chinese Stocks and Copper Reflect This Pressure

China's main index – the Shanghai Composite – already reflects concerns about China's growth as it has topped off in early March, and begun declining.

Copper – a key commodity in the production process similarly reflects this pressure as it trades in a range throughout February and March unable to push above a recent downward sloping resistance trendline and horizontal resistance at 3.9450.

Президент ФРБ Нью-Йорка Уильям Дадли считает, что сигналы улучшения экономики остаются вялыми, а рисков становится все больше: это растущие цены на сырье, малый объем налоговых сборов и слабый рынок недвижимости.

По мнению экономиста, улучшение показателей было обеспечено увеличением материальных запасов страны и ненормально теплой погодой. На вопрос об увеличении программы выкупа ФРС гособлигаций Дадли ответил, что «окончательного решения еще нет», и таким образом повторил ранее озвученную позицию Комитета по открытым рынкам.

Глава Нью-Йоркского ФРБ также нивелировал достижения на рынке труда, о которых заявляют действующие власти. «Если бы уровень участия рабочей силы не снизился с 66% в 2008 г. до 64% в нынешнем, то безработица все еще была бы выше 10%».

По мнению аналитиков, выступление Дадли было пессимистичным.

Подтверждением этих слов могут служить прогнозы Дадли о росте ВВП в этом квартале. Он заявил, что «если запасы делают большой вклад в рост ВВП, то после такого квартала обычно следуют очень слабые периоды». Напомним, в IV квартале 2011 г. американская экономика выросла на 3%, из которых 1,9% пришлись на запасы.

Zero Hedge повторяет свой старый тезис: чтобы избежать окончания операции «Твист», необходимо, чтобы взгляд на экономические перспективы со стороны Феда значительно ухудшился. Что само по себе подразумевает, что рынки акций должны ответить на это снижением.

As macro data trends deteriorate and Dudley demurs, it is becoming increasingly clear that the risks for the US equity market are skewed to the downside as we head towards the end of Operation Twist (and seasonal factors subside). The Fed's 'upgrade' from modest to moderate growth certainly spooked Gold and Treasuries and saw small caps notably underperform but given historical precedence, if Operation Twist ends without a new program beginning, investors will likely expect a drop in equities (broadly) of 8-10% (which coincides with the QE1 and QE2 ends as well as the 1983, 1994, and 2003 normalizations in policy). Reiterating our recent theme, in order to avoid the end of Operation Twist, the Fed's economic outlook would need to deteriorate - which itself is a scenario likely to result in falling stock prices and just as the cause of a 'crash' in PCE towards the end of QE1 and QE2 was a function of higher inflation, we have the current spike in energy prices to ensure this time is no different.

ZH ожидает, что как в случае QE1 и QE2 причиной для такого ухудшения станут высокие цены на энергоносители – процесс, который мы сейчас как раз и наблюдаем.

Рынок высокодоходных бондов в последние 4-6 недель не разделяет оптимизма рынка акций.

As the S&P 500 reaches new multi-year highs and VIX touches multi-year lows, there is one rather large and risk-appetite-proxying market out there that is not as excited. The high-yield bond market has seen record in-flows dropping off recently and for the last four-to-six weeks high-yield spreads, yields, and bond prices have been very flat as stocks have surged ahead. Despite US earnings yields at near-record highs relative to high-yield bond yields, we see little pick-up in LBO chatter suggesting a notable preference for higher-quality junk credit (and/or lack of belief in sustainability of earnings yields) and the recent 'dramatic' outperformance in investment grade credit is a notable up-in-quality rotation (as well as early spread-compression reaction to Treasury weakness recently) that strongly suggests less risk appetite among real money managers (given how 'cheap' high-yield appears across asset classes). Lastly, the ratio of HY bond prices to VIX is near its extreme once again, something we saw occur before the risk flares of 2010 and 2011 surrounding the end of the Fed's QE sessions.

Президент ФРБ Далласа считает, что финансовая система США хорошо фондирована и не нуждается в дополнительных вливаниях ликвидности.

The U.S. financial system is well funded and needs no further injections of liquidity, a top U.S. central banker said on Monday.

"We have filled the tanks, there is plenty of liquidity. We need no more," Dallas Federal Reserve President Richard Fisher told a round table discussion at a business event in London.

Высказывания другого крупного чиновника Феда тоже не предполагают QE3 в ближайшей перспективе.

(Reuters) - The Federal Reserve has not yet decided on whether to embark on a third round of quantitative easing, or QE3, New York Fed President William Dudley said on Mo nday.

A decision on such large-scale asset purchases would depend on how the economy evolves, and would take into account "costs and benefits," Dudley added.

Overall, we think the basis for another rate cut has diminished in the last few months, thus we are not looking for the RBA to loosen policy this year. Instead, the bank may start a tightening cycle next year. The biggest threat to this stance is a possible deterioration in conditions offshore, especially in Europe and China. Also, we will be closing watching employment data out of Australia for any indication conditions in the labour market are worsening. Whilst we expect the unemployment rate to increase somewhat this year, it may not be enough to force more policy loosening from the bank given the rise will likely be partly the result of structural changes which are out of the RBA's control.

Противоречия внутри Коммунистической партии Китая, информация о которых практически все время оставалась достаточно закрытой, стали достоянием широкой общественности. ЦК Компартии приняло решение об отстранении от должности одного из самых популярных китайских политиков, члена Политбюро Центрального Комитета КПК, руководителя парторганизации города Чунцин Бо Силая.

"...We know how much money has been flowing into those bonds funds over the last three or four years. All of a sudden they might get a little nervous and say where am i going to go? Where can i get some yield and also some protection against inflation and growth? and that's when I think we're going to see people fleeing the bond market moving into stocks."

Goldman Sachs вешает лапшу на уши клиентам: прогнозирует QE3 уже в апреле

Confused why every asset class is up again today (yes, even gold), despite the pundit interpretation by the media of the FOMC statement that the Fed has halted more easing? Simple - as we said yesterday, there is $3.6 trillion more in QE coming. But while we are too humble to take credit for moving something as idiotic as the market, the fact that just today, none other than Goldman Sachs' Jan Hatzius came out, roughly at the same time as its call to buy Russell 2000, and said that the Fed would announce THE NEW QETM, as soon as next month, and as late as June.

Что нужно делать.

As for Goldman, if one ignores all of the below, the only thing to remember is that Goldman is now selling stocks to, and buying bonds from the muppets.

Вопросы и ответы: с помощью которых GS пытается своих клиентов убедить, что QE3 будет уже возможно на следующем заседании ФОМС в апреле.

Q: What is your current forecast for Fed policy?

A: It has definitely become a closer call, but we still expect another asset purchase program that involves purchases of both mortgage-backed securities and Treasuries. This would expand the Fed's balance sheet, but its impact on the monetary base would likely be "sterilized." We expect this program to be announced in the second quarter, either at the April 24-25 FOMC meeting or the June 19-20 meeting. The argument for April is that this would leave more time before the end of the long-term bond purchases under Operation Twist (more formally known as the Maturity Extension Program), and would thereby reduce the risk of market disruptions as uncertainty about the Fed's role in the market rose. The argument for June is that this would allow Fed officials a bit more time to assess the state of the economy. After June, we believe the hurdle for more action rises, not so much because of the impending presidential election but more because a decision to wait until after the end of Operation Twist would signal greater comfort on the Fed's part with denying the economy additional stimulus.

Peter Tchir of TF Market Advisors про итальянские банки и рынок госдолга

So Italian banks have issued about $100 billion of these ponzi bonds and even in this day, that is a big number.

Banks issue bonds to themselves. Then they get an Italian government guarantee. Then they take those bonds to the ECB and get money, which I assume they use to pay down other debt mostly.

The Italian banks and Italian sovereign debt markets are essentially becoming one and the same. The sovereign has added 100 billion of risk to the banks (that today no one is focused on) and the banks and ECB would have to come up with some new gimmick if the sovereign had problems.

Рынки банковского долга и суверенного долга Италии стали практически одно и то же.

These ponzi bonds ensure that Italian sovereign and bank spreads become 100% correlated over time. The fact that LTRO has daily variation margin adds to the death spiral. The fact that the ECB's outright holdings will be made senior to other holders is also an issue. I have lost track of what the EFSF or ESM are currently doing, or plan to do, but some money is being used up on the latest Greek bailouts, and the reluctance to pre-fund it, means that risk of the market rejecting EFSF or ESM bonds at times of crisis remains high.

Шансы, что рынки откажутся от бондов EFSF и ESM в момент кризиса остаются велики.

PeterTchirofTFMarketAdvisors пишет про различные сегменты рынка бондов

Without a doubt, retail has fallen in love with corporate bonds. Fund flows were originally into mutual funds, and have shifted more and more into the ETF’s. The ETF’s are gaining a greater institutional following as well – their daily trading volumes cannot be ignored, and for the high yield space, many hedgers believe it mimics their portfolio far better than the CDS indices.

The investment grade market looks extremely dangerous right now as the rationale for investing in corporate bonds – spreads are cheap – and the investment vehicles – yield based products.

И про рынок казначейских облигаций

I do not like the move in treasuries. ZIRP can hold down the short end of the curve. Operation Twist can help keep the longer end anchored and focused on the short end, but that is more difficult to accomplish. The further out the curve, the less control the Fed has. With LQD having a very long duration and trading at a premium to NAV, I think there is room for more weakness here. Investors will learn that investment grade bond investments can lose money even as spreads tighten.

В этом месяце наблюдается значительный рост волатильности юаня. Что это означает для экономики и рынков?

This month has brought signals of a subtle regime change in the People‟s Bank of China‟s (PBoC‟s) management of the external value of the Chinese yuan (CNY). We have seen a considerable upturn in the volatility of the daily PBoC fixes for USD-CNY and, more specifically, two sharp fix-to-fix CNY losses.

By and large, that China’s highly manipulated currency market is on the verge of ‘equilibrium’.

That’s to say, the country is no longer attracting enough dollar inflows to justify its long-orchestrated currency manipulation, a.k.a Treasury buying... a.k.a Chinese-led US quantitative easing.

Китай сократил покупку американского госдолга. Кто теперь будет его покупать?

As a result of the shrinking trade surplus and the need to import expensive crude, China does not have the investable dollars it once had. So it is no longer buying US Treasuries at the previous fast pace. At the same time, the US Treasury is issuing debt at the rate of $100B a month. If the Chinese aren’t buying debt, then it must be sold to other dollar holders.

The Australian dollar has long been seen as a China/commodities trade, but Macquarie’s Brian Redican reckons that’s no longer the case. The currency is increasingly influenced by external factors, rather than the country’s own ever-growing mining sector, or its monetary and fiscal policy.

And this, he says, is a momentous shift — so much so that Macquarie now sees the AUD remaining around its current levels for several years, and only gradually sliding to $1.05 by 2015. Their previous forecast was a fall below USD parity by the end of this year.

75% австралийского выпуска бондов находится за рубежом

It’s now reached the point where 75 per cent of national government bond issuance is held offshore. And yields are high against other AAA sovereign bonds: close to 4 per cent for 10-year maturities.

В дополнение темы: речь заместителя главы ЦБ Австралии

Во время Всекитайского собрания народных представителей премьер Госсовета Вэнь Цзябао всенародно объявил о необходимости реформы партийного и государственного руководства. Без этого бессмысленны экономические реформы.

Кризис в китайском руководстве

В ожидании отставки глава китайского правительства подвел итоги своей деятельности и предрек дальнейшее замедление экономики.

Комментируя обменный курс юаня, Цзябао пообещал постепенно расширять коридор его колебаний. Хотя надобности в этом уже почти нет

..."С тех пор как в 2005 году была запущена реформа курсообразования, юань укрепился к доллару на 30%. Можно сказать, что реальный курс юаня достиг сбалансированного уровня," - считает Вэнь Цзябао.

В целом выступление председателя Госсовета КНР выглядит пессимистично. Он много извинялся за ошибки руководства, говорил о неудачах правительства.

China Speech And A Word Of Warning - Chinese Premier Wen Jiabao gave a speech yesterday and the Shanghai stock market got knocked for a loop (down 340 Dow equivalent points). The media feels that was due to his warning about housing. That may be but another part of the speech caught my eye.

Wen warned that major political change is needed lest the nation fall victim to another “cultural revolution”. Was this a slightly veiled reference to the recent actions and statements of that other Chinese leader, Party Leader Bo Xilai? We’ll try to do some research on that as its implications could be enormous. A power struggle in China is clearly not priced into world markets.

Голдман считает, что продажи американских облигаций связаны с последним заявлением ФОМС и призывает продавать 10-year US Treasuries.

Last night’s FOMC statement ‘marked-to-market’ the committee’s assessment of US economic conditions, which continue to gradually improve. Attention now turns to the minutes of yesterday’s policy meeting, which may reveal whether easing options were contemplated after the expiration of ‘Operation Twist’. US Treasuries sold off yesterday, and are now breaking above the yield range in place for many weeks. The 10-year US-Germany differential, now at 40bp, is at the widest level since last November. A wider spread is in line with our valuation metrics. But the level of intermediate yields remains about 25-50bp too low on both sides of the Atlantic. Using 10-year bond futures (TYM2), we would recommend short at 129-17 for a target of 126-00 and tight stops on a close above 131-16.

Аукцион 30-year US bonds: самая высокая ставка доходности с августа 2011г. – через несколько дней после понижения рейтинга США.

As has been noted all this week, starting with Monday's 3 Year auction which printed at the highest yield in 5 months, the $12 billion 30 Year Bond did not surprise, and at a yield of 3.381%, just inside of the When Issued 3.385%, it priced at the highest yield since August 2011, or just days after the US downgrade. The Bid To Cover was 2.70, on top of the TTM average of 2.68. Take downs were a carbon copy of February, coming at 14.7%, 29.0% and 56.3% for Directs, Indirect and, of course, Dealers. Does the yield have a ways to go? Oh yes - back in February 2011 the 30 Year priced at 4.75%, and then the slow steady decline commenced. What happens next? Will the US need another downgrade for yields to paradoxically slide? Or will the Fed truly leave the UST curve untouched by phasing out its market subsidization? Hardly: as a reminder, here is where we stand: $1 trillion in bond issuance in the next 10 months, and $100 billion in bond sales by China in December (with the latest TIC data pending). Forget stocks, and keep your eyes glued to the bond market. Things are starting to get interesting, especially for the Fed whose DV01 of $2Bn means that every basis point rise in yields means less P and more L.

Что-то странное происходит на рынке бондов. Доллар укрепляется – при этом начинается какое-то повальное бегство из трежерей.

Альтернативный взгляд на недавнюю слабость в трежерях

The last few weeks have seen massive, record-breaking amounts of investment grade USD-based corporate bond issuance, at the same time dealer inventories for corporate bonds are at multi-year lows and Treasury holdings at all-time-highs. In general to underwrite the massive corporate bond issuance, dealers will place rate-locks (or short Treasuries/Swaps in various ways) to control the yield and sell the idea of the 'spread' to clients (which is where most real-money buyers will be focused on value. We suggest that the almost unprecedented corporate issuance and therefore need for rate-locks has provided a significant offer for Treasuries that the dealers (who are loaded) and the Fed (who is only minimally involved) was unable to suppress. The key question, going forward, is whether the expectations of a much lower issuance calendar will relieve this marginal offer in Treasuries and allow rates to revert back down?

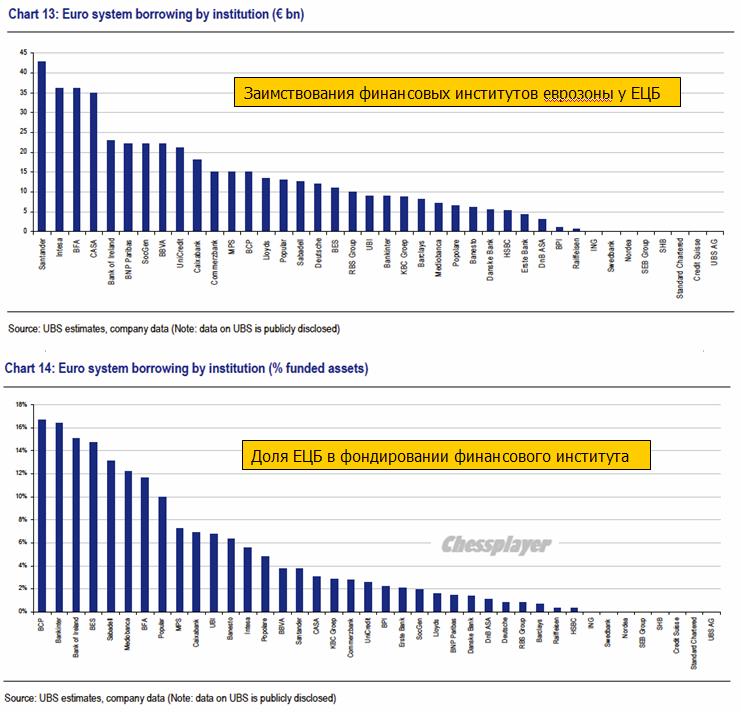

В феврале заимствования испанских банков у ЕЦБ достигли рекорда

As Banco de Espana just released earlier today, Spanish banks have borrowed a record €152 billion in February, a €19 billion increase from January. At least we now know what the capital shortfall was in Spain since pre-LTRO days, when total borrowings were €98 billion

Экс-голдманист критикует нравы, царящие в компании.

How did we get here? The firm changed the way it thought about leadership. Leadership used to be about ideas, setting an example and doing the right thing. Today, if you make enough money for the firm (and are not currently an ax murderer) you will be promoted into a position of influence.

What are three quick ways to become a leader? a) Execute on the firm’s “axes,” which is Goldman-speak for persuading your clients to invest in the stocks or other products that we are trying to get rid of because they are not seen as having a lot of potential profit. b) “Hunt Elephants.” In English: get your clients — some of whom are sophisticated, and some of whom aren’t — to trade whatever will bring the biggest profit to Goldman. Call me old-fashioned, but I don’t like selling my clients a product that is wrong for them. c) Find yourself sitting in a seat where your job is to trade any illiquid, opaque product with a three-letter acronym.

Apple теперь больше, чем весь розничный сектор США

A company whose value is dependent on the continued success of two key products, now has a larger market capitalization (at $542 billion), than the entire US retail sector (as defined by the S&P 500). Little to add here.

Исторический день: цены на бензин достигли рекорда

Presented with little comment except to remind all those newly refreshed consumers that for every penny rise in pump prices, more than $1bn is added to the hoousehold spending bill (assuming driving habits are unaffected - which brings its own set of unintended consequential events). And in the past month alone, gas prices have increased by precisely 30 cents.

Способна ли девальвация йены разрушить глобальный рост?

Seemingly hidden from the mainstream media's attention, we note that the last six weeks has seen the second largest devaluation in the JPY since Sakakibara's days in the mid-90s. As Sean Corrigan (of Diapason Commodities) notes, this has to be putting pressure on Japan's Asian neighbors - not least the engine of the world China. Furthermore, JPY on a trade-weighted basis has cracked through all the major moving averages and sits critically at its post-crisis up-trendline. As we noted last night, perhaps Japan really is toppling over the Keynesian endpoint event horizon. JPY weakness and the carry trade may not be quite as hand in hand if rates start to reflect any behavioral biases, inflation (or more critically hyperinflation) concerns any time soon.

The dollar continued to gain ground against the yen during the session, with the pair rising to its highest level since April 2011. The divergence we expect to see between the BoJ and Fed, as the BoJ continues down the loosening path and the Fed becomes increasingly optimistic, may provide a floor for USD/JPY, thus the path may be clear for a push towards 90.

Не могу с ними согласиться. Считаю, что скорее прав Джон Тейлор.

FOMC Meeting: We expect no change, in line with consensus.

BoJ Meeting: The BOJ took the market by surprise at its February MPM by (1) increasing its Asset Purchase Program budget by 10 trillion yen and (2) citing a 1% CPI inflation goal “for the time being”. Political pressure has not abated since the February MPM. At this week's MPM we expect the BOJ to extend its Fund Provisioning to Strengthen the Foundations for Economic Growth, since this is due to expire at the end of March. We also think reference will be made to the pace of upcoming asset purchases.

Вот почему USD/JPY растет! Ждут продолжения интервенций. С трудом верится, что второй месяц подряд.

ECB Draghi Speech

Ecofin Meeting

Ниже идут прогнозы по некоторым экономическим данным. Интересно будет проследить за тем, как они сбудутся.

Wed 14 March

Euro area CPI (Feb): Consensus expects a slight increase to February inflation, 2.7% from 2.6% yoy.

Euro area IP (Jan): Consensus expects further contraction of -0.8%, compared with last month’s -2.0% yoy.

United States CA (Q4): We expect a slight widening of the current account deficit on the back of larger than expected trade deficits in Q4. GS: -$119 bn, consensus expects -$114.2 bn, widening from -$110.3 bn.

Fed’s Benanke SpeechThu 15 March

US Producer Prices (Feb): Producer prices probably received a headline boost in February. GS: +0.37, at 0.5% mom, consensus is up from the previous value +0.1% mom.

US TIC Data (Jan): As always, we will look at the quality of capital inflows into the US. TIC portfolio inflows have recently been geared towards inflows into US treasuries, while US investors tend to be pretty systematic buyers of foreign stocks and bonds. Last +$17.9 bn.

Fri 16 March

US Consumer Prices (Feb): Consumer prices probably received a headline boost in February, while we expect a moderation in core inflation measures. GS: +0.45%, consensus expects 0.4% mom, slightly up from 0.2%.

US IP (Feb): We expect industrial production to benefit from strong gains in vehicle output. GS: +0.6% mom, consensus expects 0.4%, up from 0.0% last month.

The jump in yield from 0.347% to 0.456% may not sound like much, but that is what just happened following the pricing of the latest $32 billion in 3 Year paper, which came at the highest rate since October's 0.544%. And considering that anything under 3 years is virtually risk free courtesy of ZIRP, this move is actually far more pronounced than it appears on the surface.

We do not expect additional QE in the coming months

We do not expect BoJ to announce any additional QE in connection with this week's monetary meeting.

Going forward the most important question will be BoJ's commitment to its new inflation target. The suspicion remains that the easing move on 13 February was mainly driven by external political pressure and less by real conviction by the BoJ board members of the need for a more aggressive monetary stance. For that reason the release of the minutes from the 13 February monetary meeting on 16 March could prove to be more interesting than tomorrow's statement.

With GDP growth poised to rebound in Q1 (possibly above 3% q/q AR), we do not expect BoJ to announce additional QE in the coming months unless JPY for some reason resumes appreciating. The purpose of Japan's FX intervention policy remains solely to stem the appreciation of JPY. Because Japan's intervention policy has been criticized by both the US and the EU, we do not expect to see renewed intervention unless USD/JPY revisits earlier lows below 76. Overall Japan's policy of attempting to “draw a line in the sand” on a stronger JPY has gained credibility. The market increasingly understands that a substantial appreciation will be met by more aggressive monetary easing and possibly even renewed intervention in the FX market.

In our view the ceiling for asset purchases could be raised further in H2 12 to make room for continued asset purchases in 2013.

Danske Bank также не ожидает каких-либо действий от Федрезерва

Following the positive employment report for February, we believe that the FOMC will take a wait-and-see approach at its monetary policy meeting tomorrow. The recent improvement in the labour market does in our view rule out the announcement of new easing measures. However, the door for further easing will be kept open, given Bernanke's wondering over the apparent decoupling of growth and jobs data. Hence, we need more solid economic data before the Fed will make any material changes to its economic projections.

Danske Bank оценивает шансы на новый раунд QE в этом году только в 25%.

We are relatively upbeat on the US economic outlook for the coming six months and we believe that the chance of another round of Fed easing this year is only around 25%.

Banks that found themselves with above 10% of funded assets in public sector money have often either been nationalised or, like Lloyds and Bank of Ireland, have undertaken massive equity issuance in order to change their balance sheet sufficiently to make a full return to the private sector.

It will come as no surprise to any reader that volumes in general are dismal. This leads inevitably to the question of just how liquid markets are in general. This may not be a critical question for mom-and-pop buying some IBM or CAT at the margin but for institutional investors it is critical to the decision to enter a position. Pairing off reward expectations with risk concerns tends to focus too much on volatility and too little on liquidity and by looking at daily market turnover and the bid-offer spread of each asset class, UBS finds taking liquidity into account can make a huge difference to performance (and risk-appetite). Unsurprisingly, the most liquid assets are large cap equities and US Treasuries. The least liquid assets include various fixed income securities, and in particular high yield credit. Perhaps this goes a long way to explaining why US Treasuries have maintained their strength and why large cap equities have been so strong relative to credit markets (a topic we have discussed at length) as money finds its 'easiest' hole to fill and thanks to liquidity concerns, high yield credit investors remain more pragmatic entrants to an ever-inflating bubble of liquidity (as exits will be small and crowded at the first sign of tightening). We suspect the increasing dispersion between the most and least liquid securities in each asset class will likely feed on itself as fewer funds are willing to 'earn' an 'illiquidity' premium given the bigger binary risks facing all markets.

Маленькие валюты крушат большие. Корзина из 20-ти перечисленных ниже валют (G20) превосходит по всем статьям большую четверку (USD, GBP, EURO, JPY)/

The "small" currencies are crushing the bigs.

Specifically, basket consisting of The Aussie dollar, Canadian Dollar, South African Rand, Norwegian Kroner, Swedish Kroner, New Zealand Dollar, Singapore Dollar, Taiwanese Dollar, Colombian Peso, Indian Rupee, Indonesian Rupiah, Russian Ruble, Turkish Lira, Argentine Peso, Brazilian Real, Mexican Peso, Chinese Yuan, and the Malaysian Ringgit has clobbered a basket of the bigs: The Dollar, the British Pound, the Euro, and the yen.

Главный экономист Дэвид Костин по рынку акций GS видит S&P500 на 1250 пунктах к концу году.

The S&P 500 closed at about 1,370 at the end of last week, exceeding David Kostin's target of 1,250 for the end of 2012. Kostin, chief U.S. equity strategist at Goldman Sachs, told Bloomberg TV that he is sticking by his forecast despite the S&P's recent run.

Костин называет три причины:

Kostin said there were three main reasons for his call:

The U.S. economy is stagnating, growing below trend.

In a weak economic growth environment, markets historically have a flat multiple

2012 is expected to see earnings growth of only 3 percent.

Вопрос в том, не окажется ли S&P500 сперва на 1500, а потом уже на 1250 ?

Так или иначе косвенно такой прогноз свидетельствует о том, что Костин не ожидает QE3 до конца года?!

Утром сегодня Азия подрастала, хотя мне и неизвестно на каких факторах, американский фьючерс обновил максимум года.

От BOJ, заседание которого должно было состояться утром, не приходилось ждать никаких новых шагов по смягчению монетарной политики. От Феда, заседание Комитета по открытым рынкам которого должно состояться вечером – тоже.

Может быть поводом послужили какие-то позитивные новости с заседания ECOFIN (министров финансов еврозоны), хотя мне конкретно – что именно – неизвестно.

Возможно позитивные настроения продлятся сегодня в течение всего дня либо до момента завершения Ecofin.

А так, на мой взгляд, мы имеем шансы увидеть на этой неделе зеркальное отражение сценария прошлой недели. Рост в понедельник и вторник – затем коррекция до конца недели.

Значение индекса S&P500 вчера практически не изменилось, а вот put/call-коэффициент вырос почти до границы бычьего рынка.

Это неделя помимо прочего – неделя экспирации опционов на фондовые индексы. Следовательно, стоит ждать высокой волатильности.

Даже если на этой неделе мы увидим коррекцию, то все-равно пока нельзя исключать продолжения роста на будущей недели. Средний дневной диапазон (ATR) остается очень маленьким, что говорит в пользу пользу роста.

В пользу роста также говорит определенное давление, которое оказывается на рынок US Treasuries даже в те дни, когда фондовый рынок падает. В начале прошлой недели мы это наблюдали.

Кто-то сейчас активно продает американские трежеря и это поддерживает рынки акций, и в целом, аппетит к риску.

Как вы видите на рисунке, хотя число медведей приросло на прошедшей неделе, рыночные настроения на Ticker Sense продолжают оставаться бычьими.

В то же время уже есть определенные «намекающие» на коррекцию сигналы.

1.Главный стратег по рынкам акций Goldman Sachs выступил с очень медвежьими комментариями

2.Настроения среди инвесторов уж слишком безмятежные. Уровень шорта на NYSE на четырехлетнем минимуме.

3.В последние недели наметилась тенденция роста ставок по краткосрочным US Treasuries (см. на рисунке). Причины этого мне неизвестны, но как правило за этим следует рост ставок на денежном рынке и далее продажа риска.

4. Наблюдается некоторый рост среднего значения put/call-коэффициента за последнее время.

Кроме того, рост рынка идет на очень небольших объемах. Но это уже наверно стало постоянным явлением, поскольку «физиков» на рынке акций становится все меньше.

Таким образом, мы видим, что присутствуют в достаточном количестве как бычьи, так и медвежьи сигналы, что и предопределяет боковик, в котором рынок сейчас находится.

Опрос активных инвесторов, проводимый немецкой биржей, тоже показывает, что настроения колеблятся возле какого-то равновесного уровня. Если рынок припадет, начинают преобладать быки, вырастет затем на 2-3% - появляются медведи.

В целом, отметим, что, начиная с начала февраля, настроения стали колебаться между бычьими и медвежьими с небольшим перевесом то в одну, то в другую сторону.

В настоящий момент рынок находится у верхней границы коридора, очерченного лентами Боллинджера (1340-1380 пунктов) и вероятность движения к 1340 пунктам на этой неделе на мой взгляд гораздо выше, чем к 1400.

Сегодня-завтра – ключевые размещения американского госдолга – 10-year и 30-year соответственно. И это фактор может оказать медвежье влияние на рынки.

Немцы проклинают тот момент, когда Драги стал главой ЕЦБ.

Against this backdrop, it is perhaps no coincidence that details of his letter to Draghi emerged in the Frankfurter Allgemeine Zeitung (FAZ) - a respected German daily.

In his letter, Weidmann called for a return to collateral rules as they had been before the crisis, the FAZ said.

Weidmann had already expressed concern that "too generous" supply of liquidity could create risky incentives for banks, which could in turn store up future inflation risks.

Ewald Nowotny, a member of the ECB's 23-man Governing Council, went further on Tuesday and said the bank should think about an exit strategy after its massive cash injections.

Глава Бундесбанка Вайдман направил письмо Драги с призывом вернуться к более строим правилам залога.

Центральные банки стали непосредственно сами покупать акции.

The Bank of Israel will begin today a pilot program to invest a portion of its foreign currency reserves in U.S. equities.

The investment, which in the initial phase will amount to 2 percent of the $77 billion reserves, or about $1.5 billion, will be made through UBS AG and BlackRock Inc. (BLK), Bank of Israel spokesman Yossi Saadon said in a telephone interview today. At a later stage, the investment is expected to increase to 10 percent of the reserves.

A small number of central banks have started investing part of their reserves in equities. About 9 percent of the foreign- exchange reserves of Switzerland’s central bank were invested in shares at the end of the third quarter, the Swiss bank said on its website.

The investment will be made in equity index trackers and will include between 1,500 to 2,000 shares, among them stocks like Apple Inc. (AAPL), Saadon said.

After some impressive data in early February, which boosted the Russell 2000, over the last month still-solid macro data has failed to produce further results and the Russell -- along with other high beta/cyclical implementations -- have sagged (even though the S&P 500 has continued to progress). This may partly reflect the headwinds from higher oil prices and with today’s weaker-than-expected ISM, and forward-looking components also turning softer, we have decided to close this position with modest gains.

Выглядит как медвежья рекомендация

Despite our shift back to neutral, we will continue to use the data to inform our tactical trading stance, and will consider reengaging if the current softer patch in US data turns out to be transient. But our view of forward risks is more balanced at this point, having already seen a significant data-driven market rally, and with the data turning incrementally less uniformly good.

Индекс S&P500 закрылся в пятницу с минимальным снижением: -0,25%. «Полка» удлинилась до 4 сессий. В силу ряда факторов сегодня ИМХО уже маловероятно, что это стояние продолжится. Жду сильного движения вниз.

Однако произойдет это, скорее всего, только вечером.

Как и в пятницу, американский фьючерс в азиатскую сессию сходил почти на -1%, а сейчас восстанавливает свои позиции.

EURO ночью пробил уровень 1.27 и сходил до 1,2666. Но, скорее всего, это было не столько его собственное движение, сколько кроссдвижение от пары AUD/USD. Основная азиатская валюта AUD третью сессию подряд под сильным давлением в азиатскую сессию. Это между прочим симптом....

Понаблюдайте за тем, как формируется свеча EURO/AUD: в азиатскую сессию она растет, в европейскую разворачивается, а в американскую превращается в медвежью. Но если раньше огарок свечи, или как принято это называть – тень, лишь слегка заходил на черное тело предыдущей свечи, то теперь огарок удлинился, а тело стало маленьким-маленьким. Произошло качественное изменение картины.

В ближайшие день-два мы увидим разворот в EURO/AUD и я очень удивлюсь, если рост пары EURO/AUD не будет сопровождаться массированными продажами рискованных активов: нефти, акций, серебра и даже золота (обратите внимание на ценовой канал внизу графика).

Рост пары EURO/AUD при текущей диспозиции валютного рынка – негатив для рискованных активов.

Если мы посмотрим на недельный график EURO/AUD, то увидим интересную вещь: совершенно поразительное ослабление европейской валюты относительно AUD за последние три года.

Азиатские фондовые рынки падают второй день подряд. Это тоже между прочим симптом...Но, скорее всего, сегодня днем мы увидим в последний раз выкуп азиатского падения: выход американского фьючерса в район 1273 или выше, закрытие гэпа по евро где-то в районе 1,273-1,274, выход AUD/USD примерно в район 1,023.

Сегодня главное событие – это переговоры между Меркель и Саркози.

Я с трудом себе представляю, что какие-то новые детали координации бюджетной политики инициаторов создания новой «еврозоны» (бюджетной) внутри старой (валютной) могут вызвать приступ оптимизма у рынков.

Однако у рынков существует условный рефлекс, выработанный «доктором Павловым», в роли которого выступает Goldman Sachs. Этот рефлекс состоит в том, что на любых новостях о переговорах в еврозоне сперва следует расти, а затем уже реагировать так, как следует реагировать. Главный дирижер мировых рынков GS постарается исполнить для американских трейдеров в момент пробуждения какую-нибудь пьесу – типа «Доброе утро», поскольку для пьесы «Рыночный восторг» ну никак нет оснований.

На этом думаю, что рождественское ралли, начавшееся аккурат сразу после Дня Благодарения, который в прошлом году прошел очень нетрадиционно (рынки встретили его на минимумах), завершится. Существует вероятность, но очень небольшая, что будут обновлены максимумы вторника. Наверно это будет наиболее оптимальный момент для открытия шорта по индексу S&P500.

Скорее всего сразу после завершения переговоров Меркель и Саркози мы увидим новое движение вниз в EURO/USD и еще более сильное движение вниз в AUD/USD.

Проводящийся сегодня ANTI-POMO будет способствовать распродаже рискованных активов.

И в заключение еще несколько графиков:

Первый график показывает совершенную раскорреляцию в движении S&P500 и австралийского доллара, которую мы наблюдали на прошлой неделе. На мой взгляд, это определенное свидетельство искусственного поведения американского рынка акций в последние дни.

Валютным рынком манипулировать гораздо сложнее, чем рынками акций.

Второй график показывает, что между рынками акций и рынком облигаций существует теперь такая же раскорреляция. Доходность 30-year US bonds совершила прогнозируемый мною в прошлый раз разворот. Картина здесь совершенно медвежья для доходности трежерей и соответственно для рынков акций.

И еще один любопытный график. Этот график показывает, что индекс S&P500, номинированный в EURO, вышел на многолетние максимумы.

Давайте сравним его с германским фондовым индексом DAX. Если сравнить отношение текущих значений с минимумами начала 2009 года, то мы совершим интересное открытие.

S&P500/EURO=10,05/5,2=1,932

DAХ=6057,92/3588,89=1,688

При таком же уровне EURO, какой был на минимумах фондовых рынков в начале 2009 года, главный фондовый индекс Германии выглядит намного слабее главного индекса фондового рынка Америки в сравнении с началом 2009 года.

Слабая валюта, в общем и целом, должна вести к ОТНОСИТЕЛЬНОМУ росту фондового рынка Германии - страны с наилучшей в Европе экономикой и экспортером №1 в мире. Относительному - хотя бы относительно Америки.

Вспомним, как позитивно на американский фондовый рынок влияло ослабление доллара в результате количественного смягчения!

В этом, на мой взгляд, есть глубокое фундаментальное противоречие.

P.S. Пока я писал это вью, фьюч S&P500, EURO уже совершили определенные движения.

Похоже, что буквально очень скоро EURO/AUD совершит технический разворот. Для этого нужно преодолеть 1,2505. Интересно будет понаблюдать, как на это среагирует американский фьюч...