The ECB kept the leading interest rate unchanged at 1% as widely expected. We continue to expect the ECB to keep the refinancing rate unchanged until Q1 14. The chance of more rate cuts in this easing cycle has diminished further.

At the press conference, ECB President Mario Draghi cherished the effect of the 3Y LTROs and pointed towards the change in market sentiment since November. Draghi stated that the LTROs have been an "unquestionable success".

The quarterly staff forecast on inflation was revised upwards while the growth forecast was revised down. It is surging energy prices in particular that have pushed up inflation.

On previous occasions oil price increases have prompted the ECB to hike rates. We believe that Draghi will abstain from this knee-jerk reaction as he appears to put more emphasis on the fact that price pressures should remain limited in an environment of subdued growth.

The market reaction was muted as the ECB delivered as expected.

Danske Bank считает, что ЕЦБ оставит процентную ставку неизменной вплоть до первого квартала 2014 года.

Драги считает 3-хлетние LTRO несомненным успехом.

Прогноз по инфляции был немного пересмотрен в большую столрону, а по росту экономики еврозоны в меньшую.

Реакция рынка на заседание ЕЦБ по ставке была очень спокойной.

Верояность понижения ставки в течение этого цикла количественного смягчения очень мала.

Про заседание ЦБ Канады, посвященное процентной ставке

The bank upgraded its assessment of the economy as well as inflation, which argues for the next step being a rate increase, though that may still be about a year out.

On Growth: “Recent developments suggest that the outlook for the Canadian economy is marginally improved from the January MPR. Although the economy will likely grow faster than forecast in the first quarter due to temporary factors, underlying economic momentum remains around trend, balancing domestic strength and external weakness. Private demand is now expected to be slightly stronger than projected, owing to improved sentiment and highly-supportive financial conditions. Canadian household spending is expected to remain high relative to GDP as households add to their debt burden, which remains the biggest domestic risk. Net exports have been supported by stronger-than-anticipated U.S. activity but are expected to contribute little to growth, reflecting still-moderate foreign demand and ongoing competitiveness challenges, including the persistent strength of the Canadian dollar.”

On Inflation: “The profile for core and total CPI inflation is somewhat firmer than previously anticipated as a result of reduced economic slack and higher oil prices. After moderating in the second quarter, total inflation is expected, along with core inflation, to be around 2 per cent over the forecast horizon, reflecting the combination of modest growth of labour compensation, an economy operating around its potential over time, and well-anchored inflation expectations.”

The bank sees “considerable monetary policy stimulus” but did not mention removing it.

В заявлении повышены прогнозы по инфляции, что повышает вероятность повышения ставки, но никак ее понижения.

Банк видит заметное влияние стимулирующих мер в экономике, но не собирается от них отказываться.

Торговый и текущий балансы Японии рисуют удручающую картину. Это является результатом сильной йены в последние годы.

Japan's Trade and Current Account imbalances appear to be hitting some kind of terminal velocity and while neither JGBs nor CDS seem to reflect the ensuing chaotic recognition that perhaps the can that has been so faithfully kicked down the "Nishi-no-michi" or the West Road may have plunged over the lip of Mount Fuji (conjuring images of Mordor), FX markets recent and abrupt weakness brought on by yet more printing (a topic we discussed in great detail recently as the chosen heretical method du decade) may well be coming face to face with reality. We assume Azumi is faithfully watching these market moves but we wonder at what point the quasi-intentional weakening of local currencies flares into a full-blown currency war - and instead of merely encouraging simpleton FX-carry strategies chasing momentum and leverage - quickly becomes the hyperinflationary super nova that many have been waiting for over the last decade. Dismal demographics aside, we wonder how long before Koo prescribes yet more of the same medicine for this constant state of deflation and at what point does inverted-Apple-looking charts for Trade and Current Account balances become simply too hot to handle...

Не перерастут ли QE ЦБ Японии в полномасштабную валютную войну?

Про приток денег в ETF-индустрию. Почти весь приток денег представлен 6-ю фондами.

ETF fund flows have been a uniformly positive source of capital into U.S. risk markets in 2012. Looking a little deeper at the decidedly 'risk-on' flows, Nic Colas (of Convergex Group) notes perhaps their most provocative feature has been their high degree of net concentration. When you look at the entire “ETF Ecosystem” of listed funds, just 6 funds represent all the net gains in assets over the past month ($5.4 billion in net inflows) – LQD, HYG and JNK in fixed income, VWO in emerging markets, VXX in risk, and GLD in commodities. With 1,433 different ETFs listed on U.S. markets now, Colas likens the comprehension of the $1.2 trillion in AUM across these ETFs to how well you know your spouse as we know ETF flows are important (just like a wedding anniversary date or what day the trash is picked up at home) but with their still-evolving proliferation it seems a daunting task to keep tabs on them. All in all, this brief analysis points to more of a pause in investor sentiment rather than the opening for a more full-blown correction in the coming weeks.

Аналитики Morgan Stanley предлагают свой взгляд на новые греческие облигации, которые заменят старые в результате свопа

Morgan Stanley provides some color on the new GGBs, which they expect to trade at least 200bps wide of Portugal and with an inverted curve expecting prices to stabilize in the mid-20s (with technicals in the short-term pushing prices below 20). The GDP warrants are estimated at a fair-value around 1c and if the Argentine framework is any evidence, this will be heavily discounted (read ignored) by the market. All-in-all, not exactly positive but still buy stocks because 90% sounds like a good number!

Art Cashin комментирует новую идею «стерилизованного QE»

So the Fed is looking for a way to lower rates without producing any inflationary pressure. That’s because critics have claimed the inflationary impact of prior easing managed to push up oil, gold and other commodities. It also weakened the dollar.

Okay, now put on your Sherlock Holmes hat and examine yesterday’s action. Stocks rallied but so did gold and oil and lots of commodities. The dollar also fell. Those actions were just the ones that the supposed new program was designed to avoid.

Посмотрите, как среагировали на эту идею цены. Реакция была как раз именно такого характера, которого хотели бы избежать с помощью нового плана.

Юрген Шларк: «Баланс ЕЦБ – просто гигантский, качество залога – ужасающее».

[Stark] added the structure of the balance sheet is a cause for concern because increasingly short-term debt claims are being replaced by long-term ones and this will make it more difficult for the bank to reverse its loose monetary policy.

With his comments, the bank's former hawk Stark is backing Germany's central bank president Jens Weidmann. The head of the Bundesbank told Der Spiegel weekly magazine over the weekend that requirements for banks' cheap loans have been "very generous" and the program calms the situation in the short term, but this calm could be deceptive. He was concerned about the collateral requirements that the banks had to provide.

The ECB's balance sheet soared past the EUR3 trillion level last week partly because the bank has flooded markets with over EUR500 billion in cheap loans for banks.

Штарк добавил, что структура баланса ЕЦБ изменена таким образом, что краткосрочный долг заменен на более долгосрочный, и это значительно усложнит задачу по свертыванию мягкой монетарной политики.Это спокойствие обманчиво.И ZH добавляет:

Of course, this long-term deterioration in prospects for yet another central bank means that it has bought a short-term reprieve, as has been reflected by rising asset prices. However, what happens when the effect of this latest dilution in the value of the paper currency fades, or worse, when the ECB's balance sheet becomes non-performing and confidence in the montary authority is lost?

Well, since that will be "someone else' problem" why worry?

Сильная волатильность в commodities является обычным явлением в годы, предшествующие наступлению максимумов.

You might think this kind of volatility is high – and it's true. Worse – or better, depending on how you see things – the volatility in the underlying commodity is magnified in the related company stocks. This is why Doug Casey calls mining stocks, especially the juniors, "the most volatile stocks on earth." But the thing is, metals volatility has been higher in the past, particularly during a mania.

Here's what I mean.

The following chart documents gold's daily price changes from 1976 through the end of 1980. Take a look at the jump in volatility in 1979-'80.

Волатильность была нормой в 1979 и особенно 1980-ом году. Колебания в 4% и более не были чем-то необычным.

Volatility became the norm in 1979 and especially 1980. Fluctuations of 4% or more were not uncommon.

Here's the same chart for silver. The metal's volatility during the 1979-'80 period became

ZH считает, что ключевым драйвером для риска в 2012 году станет соотношение между балансами федрезерва и ЕЦБ.

Something interesting happened when the ECB announced last week that its balance sheet was about to rise by €1 trillion gross, and hit a record €3 trillion net earlier today: the EURUSD barely budged. Why? Because as a reminder, the key driving relationship for relative risk performance of 2012 as we forecast back in December is the correlation of the Fed and the ECB's balance sheets, and the EURUSD, respectively, because while we may pretend that there is still alpha in this joke of a market, the truth is that in this new normal only beta matters (the more lever the better), and the only beta that matters is that generated by relative USD strength/weakness.

Рисунок показывает кросскорреляцию между ФРС/ЕЦБ активами и EURO/USD.

In this context, we bring back readers to the chart that may be the only one that matters: the cross-correlation of the Fed/ECB total assets, and the EURUSD spot, where the first thing that stands out is that the pair should be 1000 pips lower at least. And yet it isn't. The reason for that is that the FX market is actively expecting, despite all rhetoric otherwise, an injection from the Fed. What is convenient is that the chart allows us to calculate how much the expected QE3 will be: since the absolute value of the Fed/ECB size (currency invariant) is now 0.9685m or the lowest in history, the ratio would have to raise to 1.18 for EURUSD asset implied parity. Which means the Fed's balance sheet would have to increase by about $650-700 billion promptly.

Что будет, если ФРС не приступит через какое-то время к QE3? Наступит коллапс в риске.

Что будет в том случае, если случится массированный уход от риска, выражаемый в падении рынка акций? Будет QE3.

Кто моргнет раньше?

That's only what's priced in (paging Dick Fisher) courtesy of perpetually lax Fed monetary easing decisions in the past. What would happen if the Fed were to really not do QE3 any time soon is that not only would the market not ramp, but we would see a collapse in risk, with the S&P driven to nearly triple digits, which is where it was last time the EURUSD was around 1.20 back in the August 2011 lows. On the other hand, that kind of relative market drop (especially in crude) is precisely what the Fed will need to proceed with QE3. So: who will blink - the Fed or the market?

Преимущество операции «Твист» в том, что она не ведет к увеличению и так уже раздутого баланса ФРС, а уменьшение процентных ставок в долгосрочном секторе облигаций позитивно для таких секторов, как рынок недвижимости.

Известный инвестор Марк Фабер считает войну между Израилем и Ираном практически неизбежной. В ответ на это Бернанке ничего не останется, как печатать-печатать деньги. Деньги будут нужны, чтобы финансировать войну.

Swiss money manager and long term bear Marc Faber, aka "Dr Doom", says political risk in the Middle East has increased significantly with war between Iran and Israel “almost inevitable”, and precious metals and equities investments offer some safety. "Political risk was high six months ago and is higher now. I think sooner or later, the U.S. or Israel will strike Iran - it's almost inevitable," Faber, who publishes the widely read Gloom Boom and Doom Report, told Reuters on the sidelines of an investment conference. Brent crude traded near $123 per barrel in volatile trade on Tuesday on fears of a disruption in Iranian supplies. Israeli Prime Minister Benjamin Netanyahu showed no signs of backing away from possible military action against Iran following a Monday meeting with U.S. President Barack Obama. "Say war breaks out in the Middle East or anywhere else, (U.S. Federal Reserve chairman) Mr Bernanke will just print even more money -- they have no option...they haven't got the money to finance a war," said Faber. "You have to be in precious metals and equities ... most wars and most social unrest haven't destroyed corporations - they usually survive," he said. He said that Middle East markets had largely bottomed out, though regime changes from the Arab Spring revolutions were unlikely to be investor-friendly.

В такой момент следует быть в золоте и акциях. Большая часть войн и социальных беспорядков не ведут к разрушению корпораций – они обычно выживают.

Несмотря на то, что вторая программа помощи Греции должна была положить конец беспокойствам вокруг проблемной экономики, сейчас европейские банкиры уже говорят про возможность третьей программы.

По неподтвержденной информации, такую опцию сейчас обсуждают в Европейском центробанке (ЕЦБ) и вся "тройка" международных кредиторов (Еврокомиссия, ЕЦБ, МВФ). Причем чиновники уже весьма скептически смотрят на второй транш в размере 130 млрд евро. По мнению ряда специалистов, частный сектор совсем не горит желанием списывать со своих счетов половину стоимости греческих гособлигаций и нести убытки общим размером в 74% от текущего уровня.

Такие настроения могут привести к тому, что уровень добровольного участия частного сектора в спасении Греции, так называемая программа PSI, окажется меньше 60%. В этой ситуации рискует сработать механизм принудительного обмена бондов, что будет признано кредитным случаем, иными словами, неконтролируемым дефолтом.

Последующий запуск выплат по кредитно-дефолтным свопам (CDS) повлечет за собой фантастические убытки корпораций и непредсказуемые последствия для мировой экономики.

Дедлайн, который рискует омрачиться запуском описанной выше череды событий, по срокам добровольного списания назначен на 8 марта. В ЕЦБ не исключают подобного сценария и готовятся к худшему. Между тем в "тройке" считают, что на этом фоне третья программа помощи станет неизбежной и составит приблизительно 50 млрд евро.

Банковское лобби IIF, представлявшее интересы частных кредиторов в ходе переговоров с Грецией о роллировании ее бондов и списании существенной части долга, заявило, что разногласий с властями у инвесторов не осталось.

Обмен греческих гособлигаций

Это означает, что списать как минимум 53.5% греческого долга готовы 12 банков, страховщиков, инвестфондов и хедж-фондов. В их числе BNP Paribas, Deutsche Bank, National Bank of Greece, Allianz и Greylock Capital Management.

IIF не озвучил данные о количестве греческих облигаций, находящихся во владении дюжины финансовых компаний, но осведомленные источники сообщают, что сумма может достигать 90 млрд евро.

Долговой будильник зазвонит в четверг

Принять решение кредиторы Афин должны в четверг. Шаг со стороны IIF можно трактовать как попытку призвать инвесторов сделать выбор, даже несмотря на то, что текст сообщения этому противоречит. Демонстрируя свою готовность пойти на сделку, лобби намекает другим держателям долга, что спорить с Грецией уже поздно. Но решиться на "стрижку" бизнесу непросто. Ведь потери в 53.5% - это лишь вершина айсберга.

Если принять во внимание низкую доходность новых бумаг, выпущенных Грецией и Фондом стабильности евро (EFSF), итоговые убытки могут составить 74%. При этом пункт о "коллективных действиях", который Афины задним числом вписали в текст соглашения о роллировании облигаций, не оставил инвесторам никаких шансов остаться в стороне от сделки или заблокировать ее в случае, если главное лобби - IIF - уже дало согласие на ее проведение.

У Греции нет плана В

Ну а министр финансов Греции Евангелос Венизелос сделал инвесторам последнее предупреждение. Он заявил, что текущие условия роллирования облигаций - это "лучшее предложение, потому что единственное". Нешительность может дорого обойтись бизнесу: Венизелос еще раз подтвердил, что в рамках соглашения Афинам необходимо согласие лишь 75% инвесторов. Право на принудительный запуск программы дает тот самый пункт о "коллективных действиях".

Кроме того, министр напомнил о решении Международной ассоциации по свопам и деривативам (ISDA), которая не признала реструктуризацию долгов Греции страховым случаем. "Если мы можем обойтись без страховых выплат по долгам, это наилучший сценарий" - заявил политик, однако дал понять, что и в противном случае программа все равно была бы запущена.

Евангелос Венизелос до сих пор не ответил и на главный вопрос, который интересует и кредиторов и рядовых греков. Еще месяц назад министр финансов должен был покинуть свой пост и принять участие в предвыборной гонке. Его считают главным кандидатом на пост главы партии PASOK, которую сейчас возглавляет экс-премьер Георгиос Папандреу. Однако Венизелос продолжает заниматься исключительно экономикой. Возможно, так министр демонстрирует, что его главная цель - благосостояние нации. Тем временем, выборы пройдут уже 18 марта.

HSBC think that once investors calm down a bit the long-term effect of the BoJ’s QE will be yen positive.

They definitely think the initial sell-off in the yen was overblown:

They argue extra liquidity will support risk assets and the effects of foreign investors wanting to increase their exposure to the equity market are likely to outweigh any selling of Japanese bonds – investors will move out of bonds into equities in search of higher returns – and the yen will benefit.

Essentially, QE can help boost nominal GDP, thereby supporting the currency as the FX market rewards an appropriate policy mix.

Here’s the LTRO comparison chart:

So far, so scientific.

But JP Morgan tends to agree that the yen has been way oversold and makes the very valid point that even if an independent recovery in the yen fails to materialise, a dollar-yen trade can still be seen as a cheap hedge to the possibility that risk markets succumb to fatigue.

Золотой век структурного инвестирования в Китае завершается.

Спрос на commodities будет снижаться.

Not quite 24 hours since China took the tarpaulin off the lowest growth targets since 2004, with an emphasis on consumption etc and woah, Credit Suisse’s Dong Tao has come over all epochal:

We believe the golden age of infrastructure investment is behind us now. The golden age of housing boom is behind us now. The golden age of export is behind us now. The golden age of policy stimulus is behind us now.

We ask whether China’s mighty demand for commodities will return in the medium term, and think the answer is “NO”.

Февральский PMI показал, что это не сезонная проблема

Worst February PMI since the data series started. This is not a seasonal problem

The cracks are appearing in the theory that “seasonality” is the key driver of the recent weakness in China’s steel production data – and we believe the recently released PMI data series adds further support to this view.

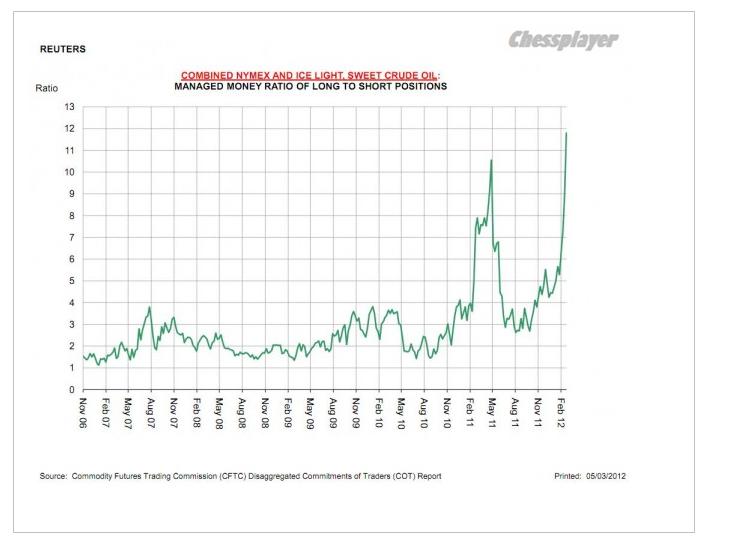

Хеджфонды и другие портфельные управляющие имеют максимальные лонги по нефти.

The following chart comes via John Kemp at Reuters. And as he notes this one kind of speaks for itself:

As a reminder, there are four reporting classifications: Producers, swap dealers, managed money (MM) and “other reportables” — thus, if managed money (which combines both speculative & passive positions) is nearly 12:1 long, some of the respective “others” must be somewhat short.

Неголосующий член Феда говорит о монетарной политике Федрезерва.

And now for some pure irony, we have a member of the Fed, granted a gold bug, but a Fed member nonetheless, one of the same people who not only enacted ZIRP, but encourage easy money every time there is a downtick in the market, complaining about, get this, Wall Street's "continued preoccupation, bordering upon fetish" with QE3. The irony continues: "Trillions of dollars are lying fallow, not being employed in the real economy. Yet financial market operators keep looking and hoping for more. Why? I think it may be because they have become hooked on the monetary morphine we provided when we performed massive reconstructive surgery, rescuing the economy from the Financial Panic of 2008–09, and then kept the medication in the financial bloodstream to ensure recovery....I believe adding to the accommodative doses we have applied rather than beginning to wean the patient might be the equivalent of medical malpractice

When we talk about China as an “investment-centric” economy – and this is something that I pound on the table and repeat in any and all forums – it can be very misleading; if you look at the sharp trend rise in China’s investment/GDP ratio over the last ten years, this increase has come predominantly from (i) property construction and (ii) related infrastructure, which would of course include the roads, subways, sewage and everything else that accompanies the housing and property build.

I.e., we’re not really talking about an ever-increasing share of the economy that has gone to, say, traditional SOE industrial capex or export-oriented investment. That is not really what the numbers are telling us over the last ten years in China. And as a result, when we think of “de-investifying” the economy and reducing the investment share, what we are really talking about at the end of the day is turning around the property boom.

And this goes directly to George’s point about the pace of investment decline, whether it comes down slowly or collapses. In China it’s very simple: you want to keep both eyes on the state of property markets. If the property market can stabilize and go sideways for a while and consumption continues to grow, then suddenly you have a more orderly adjustment on your hands. But if property markets are going to collapse or fall sharply over a sustained period of time, then you obviously have much lower hope for an orderly adjustment in this economy.

So the first point I would make for investors and clients listening on the call is “watch property in China”.

Главный призыв в отношении Китая: следите за рынком недвижимости.

случае уменьшения стоимости банки должны увеличивать залог под взятые кредиты.

This 'Deposits Related to Margin Calls' line item on the ECB's balance sheet will likely now become the most-watched 'indicator' of stress as we note the dramatic acceleration from an average well under EUR200 million to well over EUR17 billion since the LTRO began. The rapid deterioration in collateral asset quality is extremely worrisome (GGBs? European financial sub debt? Papandreou's Kebab Shop unsecured 2nd lien notes?) as it forces the banks who took the collateralized loans to come up with more 'precious' cash or assets(unwind existing profitable trades such as sovereign carry, delever further by selling assets, or subordinate more of the capital structure via pledging more assets - to cover these collateral shortfalls) or pay-down the loan in part. This could very quickly become a self-fulfilling vicious circle - especially given the leverage in both the ECB and the already-insolvent banks that took LTRO loans that now back the main Italian, Spanish, and Portuguese sovereign bond markets.

Теперь строка «'Deposits Related to Margin Calls' в еженедельном стейтменте приобретает особое значение.

What should also start to worry the Germans is the fact a 37x levered hedge-fund central bank with EUR3 trillion balance sheet that has extended credit in a 'risk-managed' approach on what appears to be an ever dwindling supply of performing collateral is starting to see dramatic 'gaps' in its asset-liability exposure (but rest assured Bernanke told us that our FX Swaps are safe as houses).

А каковы перспективы LTRO3?

One last point should be noted - the hopes of an LTRO3 or some such are surely now out of the window as clearly banks have run dry of any and all reasonable collateral or can the sovereign bonds purchased using LTRO1 and LTRO2 funds be lodged once again in a rehypothecated miasma circling the drain?

Очень проблематично, в т.ч. и потому, что банки уже исчерпали все стоящие залоги

Большая статья Peter Tchir о перипетиях переговоров по греческому долгу.

The situation in Greece should create some big headlines this week. The bond exchange “invitation” is set to expire at 3pm EST on Thursday March 8th. This is the so-called Private Sector Involvement or PSI. Greece has other steps to take during the week, and ultimately the Troika will determine how to proceed with the bailout, but not until the results of the PSI are known.

What a no-brainer to suck at the teat and go long some very transparent and liquid debt that matures in less than three years (how can there not be a rally in global risk assets when Europe's central bank pumps a combined $1.3 trillion into the financial system? Not to mention a second bailout for Greece we were told a year ago there wouldn't be any!). This must be the safest carry trade ever, or at least that is the perception (1% LTRO loan for a 5% Italian bond or a 2% short-term note even ... back up the truck!). Put up a tiny bit of capital and lever it up. It is incredible that we live in a world where the difference between going out of business as a bank and prosperity lies with cheap money being accessed from the central bank balance sheet.

Если LTRO-1 еще можно рассматривать как способ уберечь систему от разрушения, то LTRO-2 означает переход от роли кредитора в последней инстанции к роли «кредитора по первому вызову», как это назвал Peter Tchir.

At least LTRO1 was dealing with a possible breakdown of the system since the banks weren't lending to each other. LTRO2 is clearly an overt policy move from the traditional central bank role of being the lender of last resort (which even LTRO1 was to a point) to being the lender of first call, as Peter Tchir aptly puts it. There is no such thing as a free lunch, but there is such a thing as the law of unintended consequences. I can't say I know for sure what they will be or when they will show up, but there are going to be repercussions from a central bank morphing from a bona fide lender of last resort to a gift-giving institution.

ЕЦБ движется от роли традиционного центрального банка к роли учреждения, осуществляющего квазибюджетную политику.

Somehow a long gold, short euro barbell looks really good here. Bernanke, after all, now seems reluctant to embark on QE3 barring a renewed economic turndown while the ECB is moving further away from the role of a traditional central bank to take on the role of quasi fiscal policymaking, The German central bank, after all, is responsible for 25% of any losses that would ever be incurred by the massive Draghi balance sheet expansion. Why would anyone want to be long a currency representing a region with a 10.7% unemployment rate, rising inflation rates and free money? Mind you — the same can be said for the US (where U-6 jobless rate is even higher), which is why the best currency may be physical gold (or the producers that trade very inexpensively here and you pickup some leverage).

Дэвид Розенберг предлагает входить в лонг по золоту и шорт по EURO.

Since this week’s LTRO operation, the EUR/USD has fallen 3 straight trading days by as much 280 pips. Based on this price action, it looks like the pair is on its way to “mirroring” the post December LTRO move. It wouldn’t take much for this to occur - all the EUR/USD needs to do is fall another 180 pips which would STILL put it above the psychologically significant 1.30 level. Back in December, the selloff in the EUR/USD felt so much deeper because it triggered a break below 1.30 and a move to an 18 month low. I’m betting on it happening again. What about you?

Депозиты ЕЦБ увеличились до рекордных 777 млрд. EURO. ПО оценкам Zero Hedge чистый приток ликвидности от LTRO-2 составил 311 млрд. EURO – это почти ровно столько, насколько увеоичились депозиты ЕЦБ. Значит все новые деньги там.

ИМХО ZH занизил существенно приток новых денег.

When explaining the practical effect of Wednesday's second and certainly not last LTRO, we said that "when it comes to explaining why Europe's banks are not only not deleveraging but increasing leverage while paying an incremental 75 bps on up to €700 billion in deposits soon to be handed over to the ECB, one needs all the favorable spin one can muster." We also estimated that net of rollovers and other tangents, the true net liquidity add would be €311 billion and "the final number by which the ECB's deposit account will increase will be about €210 billion less than the overhead number" of €529.5 billion. Sure enough, as of this morning, which takes into account the full settlement and allocation of the second LTRO cash installment, the ECB's deposit facility has soared by precisely as expected, rising by €302 billion overnight to an all time record of €777 billion, or just over $1 trillion. In other words, Europe has now successfully managed to fool everyone that it is executing the carry trade, when it is doing nothing like that at all, and it continues to park record amounts of cash with the ECB on which not only is it not earning a carry spread, but it is losing 75 basis points as it is paid a meager 0.25% for a deposit that cost it 1.00%. Said otherwise, instead of building a cash position and retaining earnings to fund €3 trillion in debt rollovers over the next three years (by the time the LTRO matures incidentally - good luck paying down that additional €1 trillion, which makes it a total of €4 trillion in maturing debt), roughly 800 European banks will bleed by €6 billion in the next year just to store their cash with the ECB. So much for promises of the carry trade. And we certainly commiserate with all those who bought European bonds on the assumption that they were frontrunning banks who are buying up BTPs, Bonos and what not. They were only frontrunning themselves.

Немцы проклинают тот момент, когда Драги стал главой ЕЦБ.

Against this backdrop, it is perhaps no coincidence that details of his letter to Draghi emerged in the Frankfurter Allgemeine Zeitung (FAZ) - a respected German daily.

In his letter, Weidmann called for a return to collateral rules as they had been before the crisis, the FAZ said.

Weidmann had already expressed concern that "too generous" supply of liquidity could create risky incentives for banks, which could in turn store up future inflation risks.

Ewald Nowotny, a member of the ECB's 23-man Governing Council, went further on Tuesday and said the bank should think about an exit strategy after its massive cash injections.

Глава Бундесбанка Вайдман направил письмо Драги с призывом вернуться к более строим правилам залога.

Центральные банки стали непосредственно сами покупать акции.

The Bank of Israel will begin today a pilot program to invest a portion of its foreign currency reserves in U.S. equities.

The investment, which in the initial phase will amount to 2 percent of the $77 billion reserves, or about $1.5 billion, will be made through UBS AG and BlackRock Inc. (BLK), Bank of Israel spokesman Yossi Saadon said in a telephone interview today. At a later stage, the investment is expected to increase to 10 percent of the reserves.

A small number of central banks have started investing part of their reserves in equities. About 9 percent of the foreign- exchange reserves of Switzerland’s central bank were invested in shares at the end of the third quarter, the Swiss bank said on its website.

The investment will be made in equity index trackers and will include between 1,500 to 2,000 shares, among them stocks like Apple Inc. (AAPL), Saadon said.

After some impressive data in early February, which boosted the Russell 2000, over the last month still-solid macro data has failed to produce further results and the Russell -- along with other high beta/cyclical implementations -- have sagged (even though the S&P 500 has continued to progress). This may partly reflect the headwinds from higher oil prices and with today’s weaker-than-expected ISM, and forward-looking components also turning softer, we have decided to close this position with modest gains.

Выглядит как медвежья рекомендация

Despite our shift back to neutral, we will continue to use the data to inform our tactical trading stance, and will consider reengaging if the current softer patch in US data turns out to be transient. But our view of forward risks is more balanced at this point, having already seen a significant data-driven market rally, and with the data turning incrementally less uniformly good.

Китай в декабре продал трежерей на 100 млрд. долларов. Скрытым покупателем, действующим через Великобританию, является Россия.

First, here is a link to the revised TIC data as of this afternoon. That lack of Chinese trade surplus is really starting to bite not only China, but also the US, which as we noted last time, will be forced to rely ever more on domestically funded purchases of USTs: read Primary Dealers and the Fed, as the rest of the world developing world, also known as US Treasury buyers, clams down and exports far less to a recessionary Europe and contracting America. As the chart below shows, Chinese holdings are sliding, no matter how one cuts the data.

Yet the biggest surprise, is that contrary to previous speculation, Russia has not been dumping its Treasurys. In fact the country's holding of $150 billion are the same as they were back in June, and over $60 billion more compared to the pre-revised number.

In other words the biggest beneficiary of stealthy UK accumulation is no longer China (which is not accumulating US paper at all and quite the contrary), but Russia.

Чтобы получить представление о том, как поведут себя US Treasuries, нужно следить за китайским торговым профицитом. Если он вдруг превратился в дефицит, то это немедленно вызовет проблемы в US Treasuries.

Then again, this is the TIC data, which is notoriously wrong all the time. Best advice: keep a track of that Chinese trade surplus. If it becomes a deficit (just like Japan did recently), that is the first signal that things are changing dramatically from an international flow of funds perspective. It also means that unless the US finds subtitute demand, most likely from within, the only remaining buyer will be the entity that already has the largest holding of US paper - the Federal Reserve.

A month ago, Zero Hedge readers were stunned to learn that unemployment among Europe's young adults has exploded as a result of the European financial crisis, and peaking anywhere between 46% in the case of Greece all they way to 51% for Spain. Which makes us wonder what the reaction will be to the discovery that when it comes to young adults (18-24) in the US, the employment rate is just barely above half, or 54%, which just happens to be the lowest in 64 years, and 7% worse than when Obama took office promising a whole lot of change 3 years ago.

Федрезерв возобновляет обратные репо: надо изымать долларовую ликвидность.

В принципе это является бычьим сигналом для USD.

Dumping yet another liquidity cold shower in the aftermath of today's less than dovish Humphrey Hawkins speech by Bernanke (and sending precious metals even lower, albeit briefly), is the Fed's resumption of even more purely optical liquidity extractions, however symbolic, in the form of reverse repos, after the NY Fed just completed the first such operation since the dark days of summer 2011. As a reminder, the last time the Fed did these was back in August 2011 which cemented the market's plunge as it gave the market the impression that at least superficially no more money was coming in (intuitively it makes no sense to have Reverse Repos running at the same time as incremental liquidity), even as the reliquification baton was quietly being passed to the ECB. Today, reverse repos resume, as the Fed pays Primary Dealers an annualized rate of 0.17% in exchange for lending out $100 million in Treasurys. Will this continue? It depends entirely on what the economy, pardon, the Russell 2000 does. After all, that is the third and only mandate of the Fed that matter. And if the market considers this an indicator that QE3 really is delayed indefinitely, the FRBNY will mostly likely be forced to reassess.

Европейская команда MS отвечает на наиболее часто дискутируемые вопросы, касающиеся QE.

Morgan Stanley's European Economics Team asks and answers five of the most frequently discussed questions with regard quantitative easing. From whether QE has worked to inflation fears and concerns over policy normalization and what happens if the public lose confidence in central bank liabilities, we suspect these questions, rather dovishly answered by the MS team, will reappear sooner rather than later, and as they interestingly note, the deployment of central bank balance sheets is, in essence, a confidence trick.

Греки сейчас делают две основные вещи: они бастуют и забирают деньги из банков

Just like the housing market in the US, following the modest blip higher in December Greek bank deposits, immediately the great unwashed took to calling an end of the Greek deposit outflow and seeing a glorious renaissance for the country's bank industry. Well look again. According to just released data from the Bank of Greece, January saw Greeks doing what they do best (in addition to striking of course): pulling their money from local banks, after a near record €5.3 billion, or the third highest on record, was withdrawn from the local banking system. As a result, total bank cash has now dropped to just €169 billion, down from €174 billion in December, and the lowest since 2006. This is an 18% decline from a year ago, or €37 billion less than the €206 billion last January, and is a whopping 30% lower than the all time deposit highs from 2007, as nearly €70 billion in cash has quietly either left the country or been parked deep in the local mattress bank.

Странный во многих отношениях график, который предоставил Peter Tchir

Everyone and their mum knows by now that Italian bonds have rallied since the first LTRO and we are told that this is symptomatic of 'improvement'. While we hate to steal the jam from that doughnut, we note Peter Tchir's interesting chart showing how focused the strength is in the short-end of the bond curve (which we know is thanks to the ECB's SMP program preference and the LTRO skew) but more notably the significantly less ebullient performance of the less manipulated and more fast-money, mark-to-market reality CDS market as we suspect, like him, the CDS is pricing in the longer-term subordination and termed out insolvency risk much more clearly than the illiquid bond market does, and perhaps bears closer scrutiny for a sense of what real risk sentiment really looks like.

Рынок CDS показывает риск неплатежеспособности гораздо более отчетливо, чем рынок бондов.

Back in late November (pre LTRO and more SMP), the CDS spread was lower than the bond yield across the board (we could look at Italian bond spread to German bunds, or Italy CDS spread to German CDS). We have seen a very big move in bond yields. Yields have moved lower across the board, with the front end outperforming. CDS has moved tighter, but not by as much, and the curve when from slightly inverted, to slightly steep.

In fact, CDS spreads are now higher than bond yields (significantly so) in the 1 to 3 year range.

It would tell me that the less manipulated market, less subject to non mark to market accounting, has been less convinced by the move. I would hate to say “smart” money vs “dumb” money, but a bigger % of investors in the bond market are not subject to mark to market and are not subject to being right in the short term (or with all the bailouts – being right at all). We have also seen evidence in Greece, that the ECB’s SMP program likes the short end more than the long end, creating another artificial buyer, and they are DEFINITELY senior. So maybe CDS with less manipulation is a better assessment of risk. Since that tends to be fast money and mark to market money, it is interesting to see how much above bond yields they are willing to pay (though liquidity is low in sovereign CDS too). Maybe the CDS market is already pricing in the subordination that will occur if there is another crisis. The bond market can’t help but be pulled to the level of the ECB bid (though SMP has been quiet for 3 weeks), whereas CDS can anticipate the impact of subordination if things get bad again?

I’m not really sure what the answer is, but think this is worth watching (though in this market, the ECB will now finally get permission to sell CDS, or ban it, because who wants anything out there not fully controlled by the central banks).

ZH с обычным сарказмом пишет о статистических данных.

Earlier today, when forecasting the Chicago PMI, we warned to "expect another massive beat courtesy of consumers confident that they can have Apple apps, if not so much food, since they still don't pay their mortgages." Sure enough, the economic data is now straight out of China, with the Chicago PMI not only trouncing expectations, printing at 64, on consensus of 61 (the highest since last April when the peak of the liquidity bubble popped and the stock market rolled over), but, wait for it, the Employment index came at 64.2, up from 54.7, which was the highest employment print since April 1984! At this point it is no longer worth commenting on economic data, as between this, the NAR, the consumer confidence, it was all become farce of a blur. we now expect February unemployment to print negative as the labor participation rate slides to 50%, and seasonal adjustments and birth/date fixtures account for 5 million "additions" to jobs. One thing that is sure. There will be no more easing for a looooooooong time. Kiss any hope of more trillions in central bank liquidity goodbye.

Три графика, которые показывают, что несмотря на накачку экономики деньгами, доля кредита сокращается.

While the narrower spreads in Europe created the unintended consequence of perversely reducing the urgency for banks to delever their over-stuffed balance sheets (and in fact in many cases likely make them worse thanks to the ECB), the US Household continues to (sensibly) slowly but surely reduce their leverage. As today's Bloomberg Brief notes though, the slow pace of deleveraging will continue to weigh on growth over the next few years - even as they have drawn down debt as a percentage of personal income from its peak in June 2009 at 114.76% to 101.1% at the end of 2012. There is a long way to go to the apparent Maginot line of supposedly sustainable 90% and with wage growth stagnant, the bulk will come from debt reduction in true balance-sheet-recession style - putting still more pressure on a perniciously polarized government to do anything about it.

У португальских банков нет такого покровителя, как Драги, и покупать португальский долг некому....

As the ECB has stopped its SMP bond-buying and now the LTROs are all done (until the next one of course), Portuguese bond spreads have been increasing rapidly and post-LTRO today even more so. While broadly speaking European sovereign risk is modestly higher this week (and notably steeper across the curve) leaving funding costs still very high for most nations, Portugal has exploded over 100bps wider (and almost 70bps of that today post-LTRO) to back over 1200bps wider than Bunds. Only Italian bonds are better and even there they are leaking back to unch from pre-LTRO. Perhaps, shockingly, more debt did not solve the problem of too much debt and with growth and deficits being questioned in Ireland and Portugal (and Spain), it's clear the newly collateralized loan cash the banks have received won't be extended to the medium-term maturities in sovereign bonds.

ISDA Determinations Committee Accepts Question Related to a Potential Hellenic Republic Credit Event

LONDON, February 28, 2012 – The International Swaps and Derivatives Association, Inc. (ISDA), as secretary to the Determinations Committees (the DCs), today announced that a question relating to a potential credit event with respect to the Hellenic Republic has been submitted to, and subsequently accepted for consideration by, the EMEA Determinations Committee.

Заседание ISDA состоится 1 марта в 15.00 мск

In accordance with the Determinations Committee Rules, a meeting will be held at 11AM GMT on Thursday, March 1 to determine whether a credit event has occurred.

Further information regarding the question is available at www.isda.org/credit.

Поддерживать Грецию Германии становится все труднее

Chancellor Merkel failed to get her Chancellor Majority (310 votes in 620 member chamber) but did secure the passing of the EFSF with 305 votes.

Commentators are now busy talking about how she is increasingly finding it hard to negotiate with the Parliament and deal with overall German public opinion. There are several reasons for this:

She and her government told Parliament last year that Germany would be on the hook for a maximum EUR 211 billion. Now fast forward to today and the IMF is insisting that that EU increase the fire-power of bailout mechanisms to 700-750 bln. EUR.

This would mean the German contribution will rise to above 300 bln. EUR - in itself a problem politically (as she promised 211 was the absolute max) but add to this that the German Constitutional Court has already told the Parliament that any support for bailouts in excess of the current German budget (306 bln. in 2012) is risky and destablising. Get the picture? Indeed, the EU Summit this week will be interesting. It seems to me that Merkel will be forced to dig-in her heels on this issue and this will consequently risk the PSI deal and Greece in the process. The stakes are clearly rising.

Citigroup's Buiter put it very elegantly in his Global economic View (27. February 2012 - Why does the ECB not put its mouth where its money is? The ECB as lender of last resort for Euro area sovereign and banks):

'EU policy makers prefer support to fiscally weak Euro Area sovereigns under attack by markets to be provided through the ECB, since that support is off-budget and off-balance sheet, unlike the contributions to the EFSF, ESM'.

This is the key political driver! There is no budget, no balance sheet impact from having Draghi pretend he is the great saviour of everything European (read: banks) but if the ESM, EFSF should need additional capital, then there will need to be a vote - heaven forbid!

The divergence is in the accountability. The ECB is already violating its mandate and the Treaty but they are not up for vote or even accountability so far, hence they will fold their cards first in this game of poker and have done so, again, again and again.

Через ЕЦБ по ряду причин делать это гораздо сподручнее

S&P downgraded Greece to Selective Default (SD) from ‘CC’. S&P said that the downgrade followed the Greek government's retroactive insertion of collective action clauses (CACs). However, if the debt exchange is completed as expected, S&P will raise Greece’s credit rating to ‘CCC’. (RTRS)

-S&P have said they believe Greece would face imminent outright payment default if an insufficient number of bondholders accept the exchange offer.

The EFSF outlook was changed to negative from developing by S&P; 'AA+' ratings affirmed. (RTRS) S&P concluded that credit enhancements sufficient to offset what they view as the reduced creditworthiness of EFSF guarantors are not likely to be forthcoming. The negative outlook on the long-term rating also mirrors the negative outlooks of France and Austria.

The is to make a decision on Greece CDS triggers by 1700 GMT, Wednesday February 29. (FT Alphaville-More) The ISDA announced that a question relating to the Hellenic Republic has been submitted to the EMEA Determinations Committee. The ISDA will decide whether to accept the question for deliberation or reject it.

The ECB have temporarily suspended the use of Greek debt as collateral, reflecting the Greek debt ratings in the light of the PSI agreements. (Sources)

Standard & Poor’s Managing Director Kraemer has commented that the outlook on the Eurozone remains negative, adding that the ECB’s LTRO is not a substitute for reforms, but it does help in the immediate term. (Sources)

The ECB’s Nowotny has said there is no need for ECB’s key interest rate to move below 1% at the moment, adding that the ECB is concerned about the long-term effects of loans. (Sources)

Очень выборочно:

ЕЦБ приостановил принимать облигации Греции в качестве залога.

Важно: ISDA будет принимать решение по поводу контрактов CDS by 1700 GMT, Wednesday February 29 – в среду в 21.00 по Москве

LONDON, February 27, 2012 – The International Swaps and Derivatives Association, Inc. (ISDA), as secretary to the Determinations Committees (the DCs), today announced that a question relating to the Hellenic Republic has been submitted to the EMEA Determinations Committee.

In accordance with the Determinations Committee process, the EMEA Determinations Committee will decide whether to accept the question for deliberation or reject it and this decision will be made by 5PM GMT on Wednesday, February 29, 2012.

В среду пока лишь будет решаться вопрос, принимать ли этот вопрос к рассмотрению.

Суть вопроса:

Does the announcement of the passage by the Greek parliament of legislation that approves the implementation of an exchange offer and vote providing for collective action clauses (“CACs”) that impose a “haircut amounting to 53.5%” (MINFIN Announcement, 2.21.2012) that “shall bind the entirety of the Bondholders [of eligible instruments]” (First Article, Section 9), constitute a Restructuring Credit Event in accordance with Section 4.7 of the 2003 ISDA Credit Derivatives Definitions (as amended by the 2009 ISDA Credit Derivatives Determinations Committees, Auction Settlement and Restructuring Supplement to the 2003 ISDA Credit Derivatives Definitions, published on July 14, 2009) because (i) the European Central Bank and National Central Banks benefitted from “a change in the ranking in priority of payment” as a result of the Hellenic Republic exclusively offering them the ability to exchange out of their “eligible instruments” prior to the exchange and implementation of the CACs, thereby effectively “causing the Subordination” of all remaining holders of eligible instruments, and (ii) this announcement results directly or indirectly from a deterioration in the creditworthiness or financial condition of the Hellenic Republic?

As for what the final size of the LTRO will be, just ask your hotdog vendor: he has as much guidance as anyone else. Regardless of the size outcome, one thing is certain - the banks that are found to use the ECB's Discount Window should prepare for major stock pain, as the market, devoid of easy targets, focuses on them next as the European stigma trade becomes the hedge fund divergence trade du jour. After all there is a reason why the Fed's Discount Window expansion lasted for all of 3 months, and ended up hurting the participating banks (ahem Dexia) more than any other Fed concoction during the early stages of the Depression.

Дисконтное окно Феда просуществовало всего 3 месяца, поскольку пользование им для банков имело слишком сильные репутационные издержки. Вот и на этот раз, те, кто в полной мере воспользуется предлагаемым ЕЦБ LTRO, рискуют надолго получить черную метку и проблемы на межбанке...

Case Shiller продемонстрировал 8-й подряд месяц снижения цен на дома.

The December Case Shiller came, saw, and shut up all those who keep calling for a home price recovery. The Index printed at 136.71 on expectations of 137.11, with the prior revised to 138.24. The top 20 City composite was down -0.5% on expectations of a 0.35% drop. 18 out of 20 MSAs saw monthly declines in December over November, with just the worst of the worst - Miami and Phoenix - posting a dead cat bounce, rising 0.2% and 0.8% respectively. And granted the data is delayed, but the fact that we have now had 8 consecutive months of home price declines even with mortgage rates persistently at record lows, and the double dip in housing more than obvious, can we finally shut up about a housing bottom? Because as Case Shiller's David Blitzer says: "If anything it looks like we might have reentered a period of decline as we begin 2012.

Двойное дно по рынку недвижимости более, чем очевидно и пока не видно признаков, что рынок начинает выбираться из этого дна.

То, что цифры соответствуют текущей обстановке, уже никого не удивляет.

Начинается переход к режиму QE3 –экономического разочарования, - язвительно замечает Zero Hedge.

После LTRO от ЕЦБ следующая очередь за Федом .

And so the transition to the QE3 "economic disappointment" regime begins. Because after the ECB is done with the LTRO it's over for global QEasing, and the Fed is next. Remember- Bernanke's semiannual testimony to Congress is tomorrow. Whatever will he say....

Headline Durable Goods plunges from +3.2 to -4% on expectations of -1%

More painfully, Durable goods non-defense ex aircraft down a whopping -4.5% on Exp of -1.3%, down from +3.4%.

Visually, this is the lowest Durable Goods number since January 2009

Дефолт Греции можно считать почти состоявшимся. Но никакого волнения не ощущается. До 20 марта мы скорее увидим кредитное событие и срабатывание CAC

So far there are no dramatic consequences of the Greek default. The ECB did say they couldn’t accept it as collateral, but national central banks (including Greece’s somehow solvent NCB) can, so no real change. We will likely get a Credit Event prior to March 20th once CAC’s are used to get the deal fully done. Will the market respond much to that? Probably not, though there is a higher risk of unforeseen consequences from that, than there was from the S&P downgrade. It just strikes us that Europe wasted a year or more, and has created a less stable system than it had before. Tomorrow’s LTRO is definitely interesting. It seems like every outcome is now bullish – big take up is bullish because of the “carry” trade. Low take up is bullish because “banks are okay”. Any weak bank looking to borrow from the LTRO to buy sovereign debt would be insane to buy bonds longer than 3 years and take the roll risk, but on the other hand, the weakest and most insolvent, got there by doing insane things in the first place.

Любой исход завтрашнего LTRO будет позитивен для рынков.

Большой спрос – позитивен из-за кэрритрейда. Маленький спрос – потому-что у банков все ок.

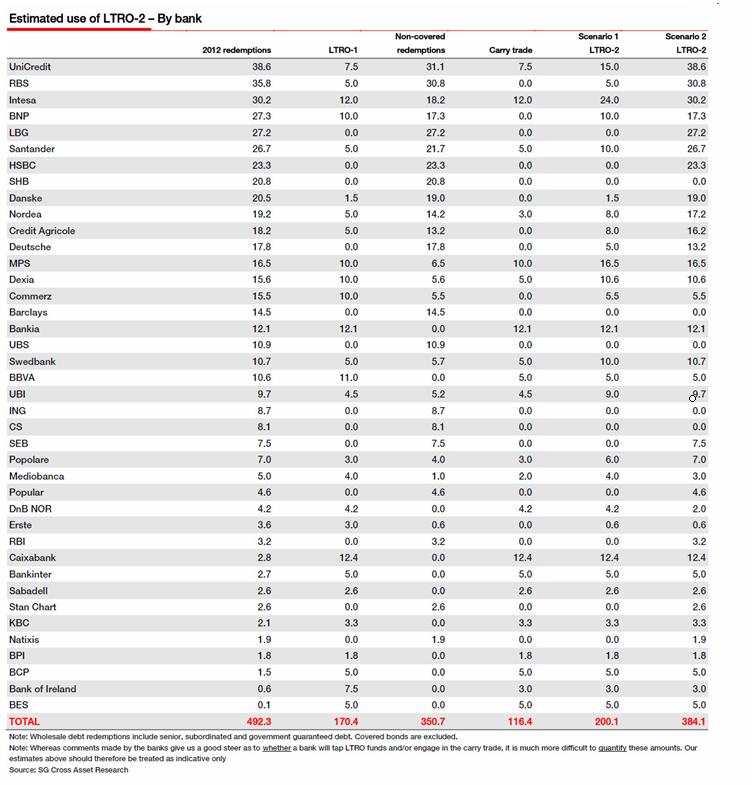

SocGen provides a comprehensive top-down analysis of the drivers of LTRO demand, the likely uses of those funds, and estimates how much of this will be used to finance the carry trade (placebo or no placebo). Italian (25%) and Spanish (20%) banks are unsurprisingly at the forefront in their take-up of ECB liquidity (likely undertaking the M.A.D. reach-around carry trade ) and have been since long before the first LTRO. On the other side, German banks have dramatically reduced their collective share of ECB liquidity from 30% to only 6%. SocGen skews their detailed forecast to EUR300-400bn, disappointing relative to the near EUR500bn consensus - and so likely modestly bad news for risk assets. Furthermore, they expect around EUR116bn of this to be used for carry trade 'revenue' production which will however lead to only a 0.6% improvement in sectoral equity levels (though some banks will benefit more than others), as they discuss the misunderstanding of LTRO-to-ECB-deposit facility rotation. We, however, remind readers that collateralized (and self-subordinating) debt is not a substitute for capital and if the ECB adamantly defines this as the last enhanced LTRO (until the next one of course) then European banks face an uphill battle without that crutch - whether or not they even have collateral to post. Its further important to note that LTRO 2 cannot be wholly disentangled from the March 1-2 EU Summit event risk and we fear expectations, priced into markets, are a little excessive.

[ZH: What we do note is that this is unlikely to be a Goldilocks moment. Too small an uptake, as SocGen expects will lead to risk-off and disappoint markets. Too large an uptake, in our view, will also shock the market - the greater stigma and rising subordination of assets via collateralization will hurt senior unsecured credit and implicitly cost of funding medium-term (shutting private funding channels and increasing public funding dependencies) - leading to risk off. Unless we see EUR475-EUR525bn - just right - then we suspect we will see risk-off either way.]

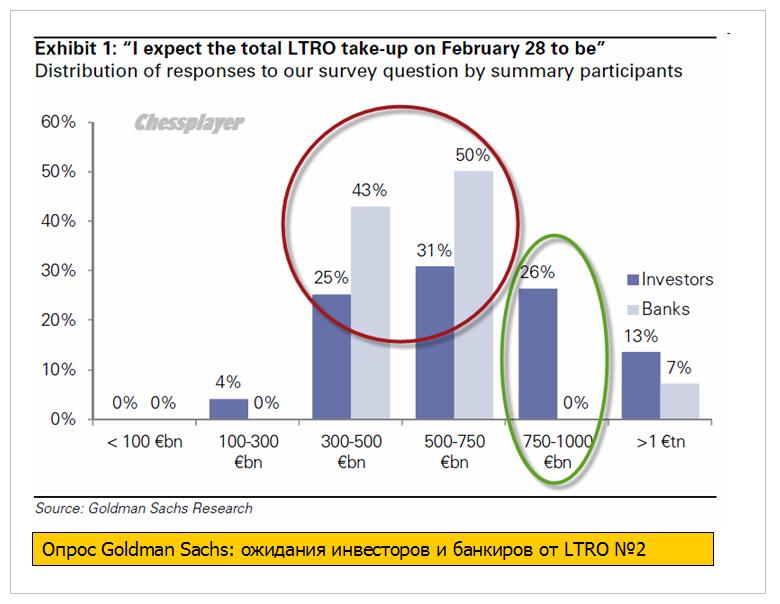

Gaming out the impact of this week's LTRO2 demand on global risk assets is complicated by the ability of banks to mobilize collateral (how much can they pledge to the ECB and how much of that will be 'optimal' given the implicit subordination of senior unsecured debt holders), the use of those funds (carry trade economics are considerably lower and refinancing needs remain high), and the market's expectations (just how much more back-door QE is priced into European - and for that matter - US asset prices). Goldman Sachs surveyed its clients and found a gaping divide between banks and investors with the latter expecting considerably more than the banks - it seems someone will be disappointed - investors hope for more and banks expect to do less.

Ожидания банкиров и инвесторов относительно размера предстоящего LTRO №»2 разительно отличаются. Банкиры ждут гораздо меньшего: по-видимому они гораздо лучше осведомлены о способности банков предоставить подходящий залог.

Банк Англии может еще расширить программу выкупа активов, размер которой сейчас составляет 325 млрд фунтов, заявил председатель комитета по монетарной политике Пол Фишер.

"В этом вопросе необходимо сохранять не зашоренный взгляд на вещи, что мы и делаем. Скорее всего, мы подождем до мая, когда мы подготовим новый экономический прогноз, и, основываясь на нем, примем соответствующее решение. Мы можем в будущем столкнуться с любыми сюрпризами, как положительными, так и с негативными", - заявил он в интервью телеканалу Sky News.

Двадцатка министров финансов отказалась увеличивать фонды МВФ.

And below are some of the key excerpts from the G-20 communique (source)

We are reviewing options, as requested by leaders, to ensure resources for the IMF could be mobilized in a timely manner. We reaffirmed our commitment that the IMF should remain a quota-based institution and agreed that a feasible way to increase IMF resources in the short-run is through bilateral borrowing and note purchase agreements with a broad range of IMF members. These resources will be available for the whole membership of the IMF, and not earmarked for any particular region. Adequate risk mitigation features and conditionality would apply, as approved by the IMF Board. Progress on this strategy will be reviewed at the next ministerial meeting in April. Other options mentioned by leaders in Cannes such as SDRs are under review."

Автор статьи Peter Tchir сравнивает последние меры по лечению европейского долгового кризиса с таблетками с эффектом плацебо.

Пациенту временно становится лучше, но эффект очень кратковременен и реального лечения болезни нет.

Making it even more difficult to determine if a policy is working is the “placebo” effect. The market is being fed a lot of medicine (pun intended). LTRO and Greek “resolution” being the latest medicines. But are these treatments really working or are we rallying on a diet of pablum?

The LTRO was designed to support the market, the market is up, so the LTRO must be working. That at least is the logic many investors are applying. They see the improvement in sovereign debt yields, the avalanche of “positive” (if unfounded) headlines, and the relentless march higher of the stock market. So the plan is working? Not so fast. The treatment was designed to help the stock market. The stock market is encouraged by that and believes it is getting better. That price action in turn convinces more people that things are better or fixed, and creates further demand for stocks. But is it real or are we just in another “Placebo Effect” stock market rally? The problem with the patients who get better on the placebo, is that the effect tends to be short-lived since nothing is actually fixed.

Рынки недвижимости и розничной торговли, получившие наибольшие выгоды от кредитного разгула ждут очень тяжелые времена..

Retail sales in 1992 totaled $2.0 trillion. By 2011 they had grown to $4.7 trillion, a 135% increase in nineteen years. A full 64% of this rise is solely due to inflation, as measured by the BLS. In reality, using the true inflation figures, the entire increase can be attributed to inflation. Over this time span the U.S. population has grown from 255 million to 313 million, a 23% increase. Median household income has grown by a mere 8% over this same time frame. The increase in retail sales was completely reliant upon the American consumers willing to become a debt slaves to the Wall Street bank slave masters. It is obvious we have learned to love our slavery. Credit card debt grew from $265 billion in 1992 to a peak of $972 billion in September of 2008, when the financial system collapsed. The 267% increase in debt allowed Americans to live far above their means and enriched the Wall Street banking cabal. The decline to the current level of $800 billion was exclusively due to write-offs by the banks, fully funded by the American taxpayer.

.....

Credit cards are currently being used far less as a way to live beyond your means, and more to survive another day. This can be seen in the details underlying the monthly retail sales figures. On a real basis, with inflation on the things we need to live like energy, food and clothing rising at a 10% clip, retail sales are declining. Gasoline, food and medicine are the drivers of retail today. The surge in automobile sales is just another part of the “extend and pretend” plan, as Bernanke provides free money to banks and finance companies so they can make seven year 0% interest loans to subprime borrowers. Easy credit extended to deadbeats will not create the cash flow needed to repay the debt. The continued penetration of on-line retailers does not bode well for the dying bricks and mortar zombie retailers like Sears, JC Penny, Macys and hundreds of other dead retailers walking. With gas prices soaring, the economy headed back into recession and the Federal Reserve out of ammunition