The 1922 German hyperinflation experience was undoubtedly propelled by printing massive amounts of money. Yet, the Japanese money printing experience has had no impact whatsoever on inflation.

Here we are in 2012, and the World’s four main central banks (USA, Britain, Europe and Japan) continue to print gobs of money. Will the outcome be 1922 Germany or 1990 Japan?

An important point to understand is whether the printed money actually flows through to the economy. In the 1922 German case – yes, it definitely did. The printed money circulated in the economy causing the German Mark to plummet against other currencies which resulted in extreme inflation.

Самое важное – понимать, поступают ли напечатанные деньги в экономику.

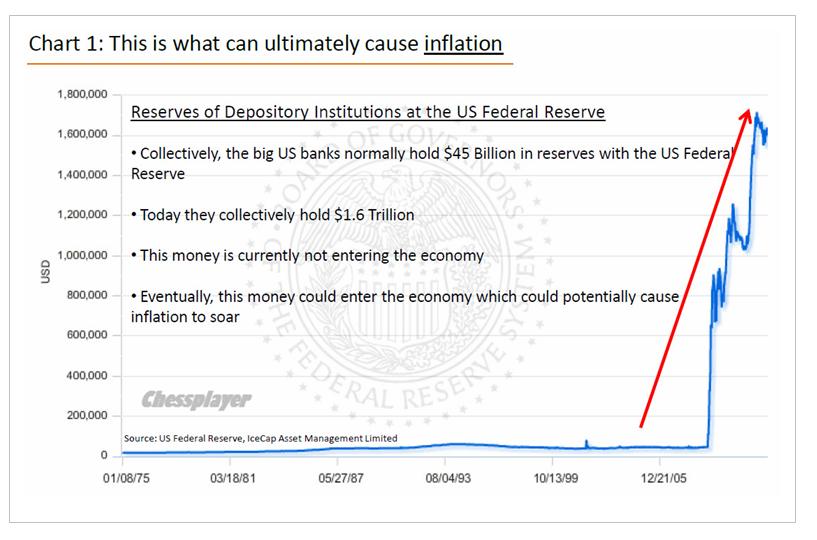

Today, trillions of Dollars, Yen, Euros and Pounds are being printed – yet this new money is certainly not being distributed into the economy. Instead, big banks everywhere are hoarding the newly minted cash for a rainy day. In economic parlance, this is referred to as a “liquidity trap” meaning there is plenty of cash available, however the cash remains trapped and is not being used. This makes today’s situation, perilously closer to the Japanese experience.

На рисунке внизу показаны резервы депозитарных институтов в ФРС

We (and many, many others) have been very critical of the American, European and British central banks. We freely admit that these people all have very good intentions – they truly do want the World’s economy to return to normal.

Yet in our opinion, it is their analysis of the problem that is leading them to make a very big mistake. The central banks fully believe that the World is currently suffering from what they would call – an aggregate demand problem. They believe growth is slow around the World because people and companies are not spending as much money as they normally would.

Сейчас 2012 год и 4 основных центральных банка продолжают печатать горы денег. Что будет в результате: Германия 1922 года или Япония 1990?

To many of the big banks, stock brokers and mutual fund sales people, this “aggregate demand problem” sounds no different than any other economic slow down – it’s a part of a normal business cycle. And during a normal business cycle, the solution to encourage people and companies to spend more money has always been 1) lower interest rates and 2) increased government spending. And if the situation becomes untenable as it is today, you can add 3) money printing to the list.

The reason this combination isn’t working today is due to the flawed belief that all of this extra money sloshing around in the economy will naturally entice people and companies to spend their hard earned (and borrowed) money again.

With trillions in freshly printed money, sub 2% growth, widening government deficits and continued bailouts to banks, it has become crystal clear that the central banks’ money printing strategies are not working.

The reason it isn’t working is simply due to the fact that all of this free money being provided to the banks, is not being distributed back into the economy. US and European banks are hoarding this free money and as a result - the transfer mechanism is broken.

Деньги, которые печатают центральные банки, не попадают в экономику. Трансферный механизм разрушен.

For the game of Tug of War - it is this lack of liquidity-flow-through that is hugely supportive of a return to the 1990 Japanese experience. The lack of spending by people and companies in favour of paying down their debt and increasing their savings guarantees sluggish growth at best.

However, it is also critical to know that despite the hoarding of cash by the big banks, the act of money printing by the central banks strongly encourages investors to shun low paying bonds and cash, and instead focus on stocks and commodities.

This by product of money printing has two effects. First, it pushes commodity prices higher, which inevitably causes the prices of some things to also rise higher (when you have a chance, check out the price of gasoline these days).

Secondly, while a higher stock market does help everyone who owns stocks, it just so happens to help the very wealthy a lot more. It is this growing divide which is fueling the bitter tax debate in the US, as well as being the spark for the recent “Occupy Wall Street” movement. Today, you can also include it as the indirect spark which will lead to the eventual social uprising in Greece.

Побочный эффект от печатания денег – рост commodities и перераспределение национального богатства в пользу более богатых.

The bottom line is as follows – the combination of the bursting of property prices and the refusal of the big banks to write-off the corresponding bad debt is resulting in a big wave of deflation. We expect this to continue. Yet, we also are mindful enough to know that pockets of inflation will occur in various countries and within various industries.

Результат будет следующим: крах цен на недвижимость и отказ крупных банков списывать потери от этих инвестиций приведет к большой волне дефляции. Мы ожидаем, что этот процесс продолжится. Мы также не знаем, где – в каких странах и каких отраслях случатся вспынки инфляции.

The real threat of hyper inflation will occur when a major currency collapses. Any country that leaves the Eurozone will undoubtedly see extreme inflation during their transition years. Outside of the Euro-zone, Britain remains at risk due to it being a key center of global finance and at risk should the World’s super-size banks implode once again.

Реальная угроза гиперинфляции возникнет в тот момент, когда произойдет крах основной валюты.

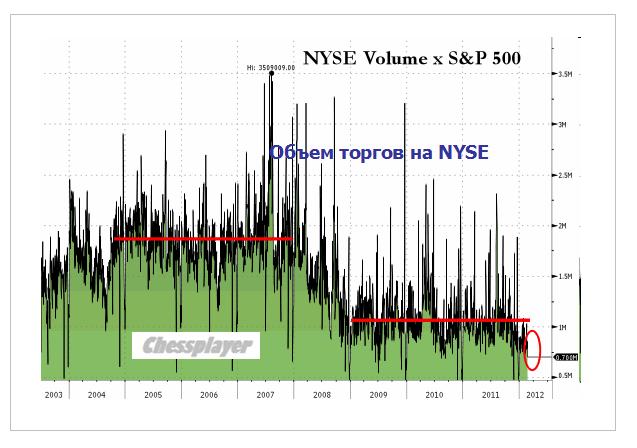

Both NYSE and ES (e-mini S&P futures) volumes were the lowest of the year so far. This is the lowest non-holiday trading day on the NYSEVOL (from Bloomberg) since its data began a decade ago and eyeballing ES volumes, this appears to be one of the lowest ever volumes of the last few years. For those who think this is irrelevant as the market's price has risen and so total USD volume remains approximately equal - wrong! Today is the lowest USD volume day since the mid 2009 (which tended to coincide with holiday trading volumes around July 4th) - making today's USD trading volume less than 50% of their 2004-2007 average!

В пятницу был наименьший объем торгов на NYSE за десятилетие. Это меньше, чем 50% от среднего объема торгов в 2004-2007 году

Торговый диапазон дня тоже наверно был минимальным за несколько дней: 5,5 пунктов (1363,47-1368,92)

Эйфория сдвинулась о рынка акций к рынку биржевых товаров

With LTRO 2 already priced in, and the Fed having been handed the baton of printing by the rest of the world's central banks this weekend at the G20 meetings, we suspect the liquidity will remain pumping in Oil until the CME steps on its throat or someone disappoints a perilously over-the-top market for stocks (and slightly less so credit now as it has started to awaken from its risk slumber) with a PSI deal fail, disappointing LTRO, new record Oil, or our favorite the unknown unknown consequence.

Объявление о результатах, кстати, последует в 14.15 по Москве.

On Wednesday at 0515ET/1015GMT, the results of the ECB's second (and, for now, final) Long-Term Refinance Operation (LTRO) will be announced. Markets are expecting Euro-area banks to draw around EUR450 bio in fresh 3-year financing, slightly less than the EUR 489 bio taken up at the Dec. 22 LTRO. Should banks take up less than EUR 400 bio, we think European government bond markets may be disappointed and we could see yields start to move higher again, which might take some of the wind out of the euro's sails.

Forex.com ожидает порядка €450 млрд. Если будет меньше, то компания ожидает, что рынки постигнет разочарование и по ним пронесется волна продаж

Next week also sees the usual month-end portfolio rebalancing flows and we expect to see a bias toward further USD-selling, typically culminating each day in the hours leading up to the 1600GMT/1100ET London fixing. The strongest dollar-sell indications are against the commodity currencies (AUD, CAD and NZD), but also against GBP, CHF and JPY. For the JPY, however, as we discuss below, we would not look to sell USD/JPY.

Аналитики Forex.com пишут о ребалансировании портфелей, которое происходит в конце месяца. Честно говоря, я не понял этого вопроса.

Более подробно о ребалансировании портфелей здесь:

Эта статья о главе ЕЦБ подтверждает высказанную мной в одной из статей идею, что Драги является засланным казачком и его действия в высшей степени позитивны для Америки и негативны для единой Европы, поскольку в долгосрочном плане подрывают европейский монетарный союз и ЕС в целом/

Сын Драги кстати работает валютным трейдером

This written statement, included in the nomination report,

4. [...A]re there any other relevant personal factors [...] that need to be taken account of by the Parliament when considering your nomination?

[Draghi] No.

is misleading because Draghi's son has been a (Euro?) bond trader at Morgan Stanley for some years, reported the newsmagazine Nouvel Observateur in January 2012. For instance, Morgan Stanley, a primary dealer in the EU, could potentially profit or unduly influence the markets, from an information leaked by Draghi to his son. The section on conflict of interest (4.1) of the ECB code of conduct (2002/C 123/06) specifically addresses "potential advantage for their families". There is a precedent of insider trading by a relative of a central banker leading. The central banker was removed from his position.

На валютном рынке сейчас одна из главных тем – японская йена

The depreciation in the Yen over the past several sessions has been nothing short of impressive and the market looks like it could really be in the process of carving a meaningful top against many of the major currencies. But what is even more fascinating is that the move in the Yen brings with it no clear catalyst for the aggressive pullback. We can not point a finger at any one fundamental driver and attribute it to the move in the Yen. Certainly, whether risk has been on or off has been irrelevant to the price action in the Yen in recent sessions, and the market seems to be stubbornly moving in one direction, paying very little attention to any of the fundamentals. We acknowledge that the recent move by the Bank of Japan to increase bond purchases is playing some part in the Yen depreciation, but at the same time have a hard time attributing the recent sell-off to this fact alone.

We have even been seeing a strong breakdown in correlations between Japanese yields and the Yen, with yields tracking far more stable since the depreciation in the Yen in recent days, and far more stable following the Bank of Japan easing announcement. The resulting price action could therefore be more reflective of a massive repositioning in the currency which now warns of a major structural reversal over the medium and longer-term, projecting significant depreciation in the currency.

О влиянии доходностей облигаций США и Японии на курсы валют

When looking at the recent rally in the USD/JPY it is important to consider the inter-market link between shorter term bonds in the US and Japan. This article attempts help explain that relationship.

Many Japanese financial institutions - pensions, insurance, and semi-government entities - and their investors generally invest in safe government bonds, usually domestically in the form of Japanese government bonds (JGB) or if internationally in US Treasuries.

Therefore, changes in the yields in these shorter-term bonds are critical to the exchange rate in the USD/JPY as these institutional investors either buy Treasuries therefore converting yen to dollars, or sell Treasuries and convert the dollar proceeds back into yen.

Therefore, the flow - the buying and selling - of Treasuries by Japanese investors is very important to monitor, and the key metric is the spread in the yield that these investors can expect to receive when comparing Treasuries to domestic bonds in the shorter maturity space (2 year).

Аукционы по размещению американского долга очень важны и статьи, описывающие, как это происходило (их публикует регулярно Zero Hedge), будут обязательно отражены в дайджесте.

Акцион по размещению 7-year прошел очень успешно. Что важно – активным было участие иностранных инвесторов.

While this week's two previous auctions were uneventful and very much unimpressive, today's 7 Year $29 billion issue continues to show that the bulk of the curve action continues to be at the belly. Unlike January's spotty 7 Year auction which saw a massive 56.64% in Primary Dealer take down, today's was the opposite, with the auction pricing a whopping 3 bps inside of the When Issued at 1.418%, with Dealers taking down just 38.89%, well below the TTM average 47.46%. This was the lowest Dealer take down since December 2010. The Indirect Bid was well higher than in January when as we already noted previously foreign investors were dumping US paper, yet at 41.85% was just in line with the TTM average of 41.54%. The big outlier however was the Direct Bid take down which soared from 11.59% to a massive 19.27% take down - a low 44% hit rate on the Direct Bid. Why the huge shift in sentiment toward US paper? It hardly has anything to do with the yield rising from a meager 1.36% to a just barely higher 1.42%. And yet, there was a tangible change in Direct interest - is it merely PIMCO buying up more paper? Most likely - this is perfectly aligned with the fund's recent average effective duration so we would not be surprised if Bill Gross is now loading up on the belly. The result of the super strong auction is the entire treasury curve sliding in yield, as it indicates that the wholesale expectation of a shift away from Treasurys and pushing into stocks, is nowhere to be seen. And stepping back from the tree, the forest now stands at just under 101.5% debt/to US GDP. Many more auctions coming.

И в заключение прогноз Николая Корженевского (Константин Бочкарев не давал валютного обзора в этот день)

Пустеющий календарь

Четверг 23 февраля 2012 г.

Время выхода форекс обзора: 12:27

Мы покупаем EURCHF, оставляем остальное позиционирование неизменным.

После двух дней мягкой продажи риска рынок берет паузу. Нет условий для резких движении в виде, например, стремительного укрепления доллара. Но отсутствуют и предпосылки для мощного роста высокодоходных инструментов. Основная пара EURUSD котируется в узком диапазоне между 1.322-1.327. И до проведения очередного трехлетнего аукциона ЕЦБ никаких событий, способных радикально изменить расстановку сил, мы не видим. На рынке все больше обсуждают нефть и ее возможное влияние на валюты. Ралли в черном золотое ускорилось. Накануне и Brent, и WTI обновили максимумы этого года. К сожалению, причина этого роста - не здоровое восстановление мировой экономики, а включение в цены премии за геополитические риски.

При таком сценарии нефть не сможет долго оказывать поддержку валютам, связанным с этим сырьем. Но на первоначальном этапе они будут смотреться лучше других товарных инструментов. Среди наиболее ликвидных относительно сильным может быть CAD, из менее популярных - NOK или RUB. В течение протяжении нескольких недель они могут дорожать быстрее конкурентов: в кроссах AUDCAD, NZDCAD уже давно наметилась коррекция. Однако потом весь рынок может оказаться во власти спекуляций на тему замедления глобальной экономики и сохранения высокой инфляции - по причине все тех же цен на нефть. Мы пока предпочитаем лишь держать длинную позицию в CADJPY и думаем над продажей AUDCAD. Но никаких агрессивных действий пока не предпринимаем. Если уж отдаться отчаянным спекуляциям, логичнее купить саму нефть Brent.

Вначале приведу прогноз Николая Корженевского (Константин Бочкарев не давал валютного обзора в этот день)

Китайское бездействие

Среда 22 февраля 2012 г.

Время выхода форекс обзора: 12:58

Мы покупаем CADJPY, будем открывать длинные позиции в USDJPY на пробитии 81 и в EURCHF на 1.2050, ищем точку входа в шорт по EURAUD.

После бурного начала недели рынок успокаивается. Накал страстей, связанных с Грецией, спадает. По крайней мере в ближайшие дни Афины станут темой второго плана. Интенсивно обсуждать финансовые истории Эллады, вероятно, вновь начнут только в марте, если, конечно, не случится чего-то непредвиденного. Пока же внимание постепенно перемещается на другие темы. Сегодня это индексы деловой активности. Главная публикация дня - данные из Китая. В феврале показатель PMI от HSBC составил 49.7. При первом взгляде кажется, что это хороший результат, уже хотя бы потому, что цифра растет третий месяц подряд и оказалась лучше ожиданий. Но, во-первых, это по-прежнему значение ниже 50, т.е. свидетельство дальнейшего сокращения экономики КНР. Во-вторых, никакого улучшения нет по ключевым подындексам: значение показателя по новым заказам осталось неизменным на 49.1, и уж откровенно плохо смотрится компонент экспортных заказов - здесь падение с 50.4 до 47.5.

Подобная статистика может спровоцировать спекуляции по поводу охлаждения китайской экономики. Это было бы негативом для всех региональных валют - AUD, NZD и JPY. О иене в этом контексте забывать совершенно не стоит, и именно она может стать аутсайдером. В последнее время для этого возникло сразу несколько предпосылок. Помимо данных из Китая, это еще и слабые цифры по торговому балансу самой страны. На них накладывается рост глобальных рост ставок, который традиционно провоцирует продажи иены для финансирования других позиций. Доходности двинулись вверх даже в США, что оказывает очень мощную поддержку USDJPY. Пробитие уровня 81 станет очень мощным сигналом к покупке с целью 88.

Аукцион по размещению 5-year US notes оказался вполне заурядным, как и прошедший днем ранее 2-year аукцион. Доходность=0,905%, Bid To Cover=2,89 – в точности соответствует среднему, участие Indirects (иностранных инвесторов), Directs, праймдилеров - на средних уровнях года. Ничем не примечательный аукцион.

Little to note about today's unremarkable bond auction of $35 billion in 5 Year bonds. Hot on the heels of yesterday's just as unremarkable 2 year bond auction, which saw total US debt/GDP surpass 101% two weeks after total debt/GDP rose over 100% for the first time, the details surrounding today's issuance were more or less as expected: the closing yield of 0.90% was inside the When Issued of 0.905%. The Bid To Cover was 2.89, weaker than January's 3.17, but right inline with the TMM BTC of 2.89. The Indirects took down 41.8%, Directs 12.9%, and the Dealers held at 45.3%, all in line with TTM average, so nothing to write home about. Overall an auction that just added a few pips to the total US debt/GDP, with the proceeds, especially by the Dealers, promptly to be pledged back into the repo market with the blessings of BoNY and State Street, where it is never heard from again.

Налоговый климат в Америке в 2013 году обещает быть очень сложным.

As he notes the radically changed taxation climate in 2013 and beyond will have an impact on all economic participants as they will probably opt to bolster their cash reserves in the second half of the year in preparation for the proverbial rainy day.

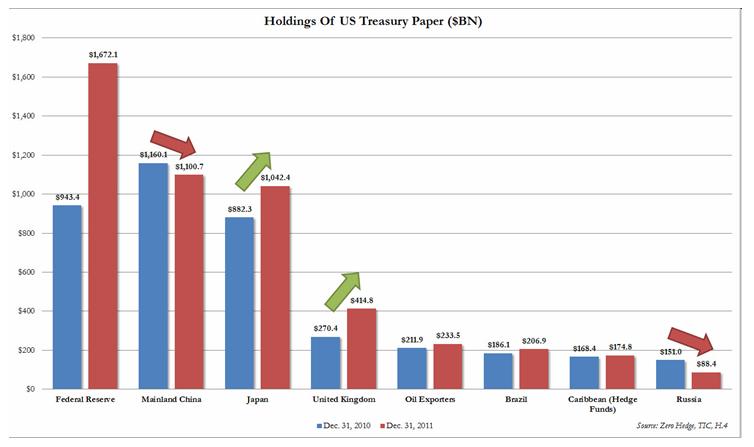

As the chart below, which highlights some of the biggest and most notable holders of US paper, shows, in the period December 31, 2010 to December 31, 2011, there have been two very distinct shifts: those who are going all in on the ponzi, and those who are gradually shifting away from the greenback, and just as quietly, and without much fanfare of their own, reinvesting their trade surplus in something distinctly other than US paper. The latter two: China and Russia, as we have noted in the past. Yet these are more than offset by... well, we'll let the readers look at the chart below based on TIC data and figure out it.

Про состоявшийся аукцион по размещению 2-year US notes: ничего примечательного

Tim Geithner just sold $32 billion in 2 year bonds at a rate of 0.31%, right on top of the When Issued, which was the highest yield since August 2011, yet nothing too dramatic. Since this is the short end of the curve where Bernanke is fully in control, the range in recent auctions has fluctuated from 0.222% to 0.31%. Yet as noted last week, the biggest "beneficiary" of short-end purchases have been Primary Dealers - are they starting to choke on thier holdings? And who will they sell to this paper which yields absolutely nothing. The auction internals were a snooze - the Bid To Cover was 3.54, a drop from January's 3.75, but higher than the TTM average of 3.42. Dealers took down 54.66%, in line with the average, Indirects left holding 35.84%, and 9.5% for the direct. Overall, nothing to write home about, and the bottom line is that the US just added another $32 billion to its net debt of $15.413 trillion, or a new record high debt/GDP ratio of 101%. It is going much higher.

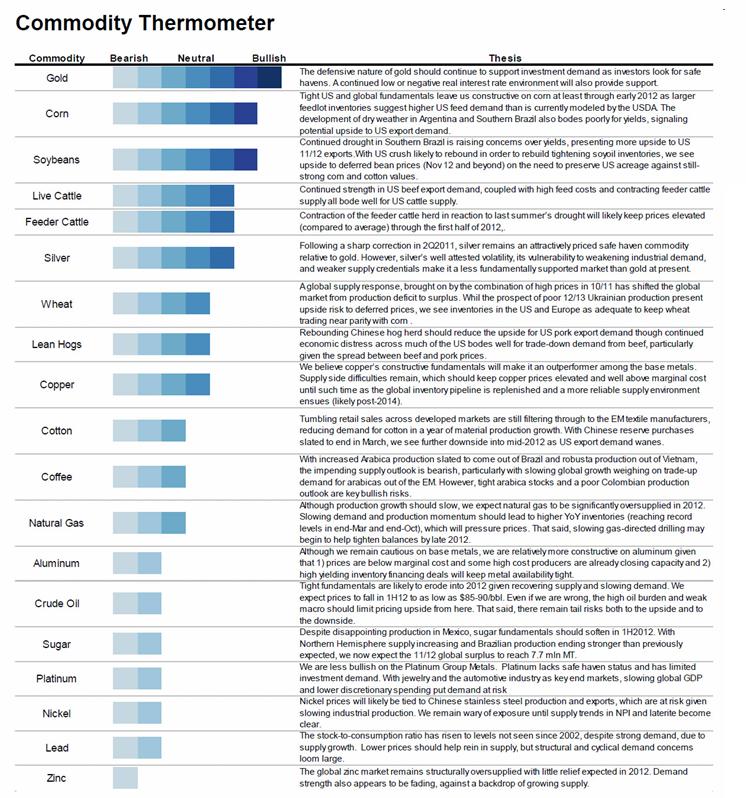

Представляем Commodity Thermometer от Morgan Stanley

По сути это прогноз на 2012 год.

...here is a simple way to gauge relative commodity strengths and weakness courtesy of Morgan Stanley's "Commodity Thermometer" which shows what products MS is bullish and bearish on, and why.

Это интересно! Если плохо видно - можно пройти по ссылке!

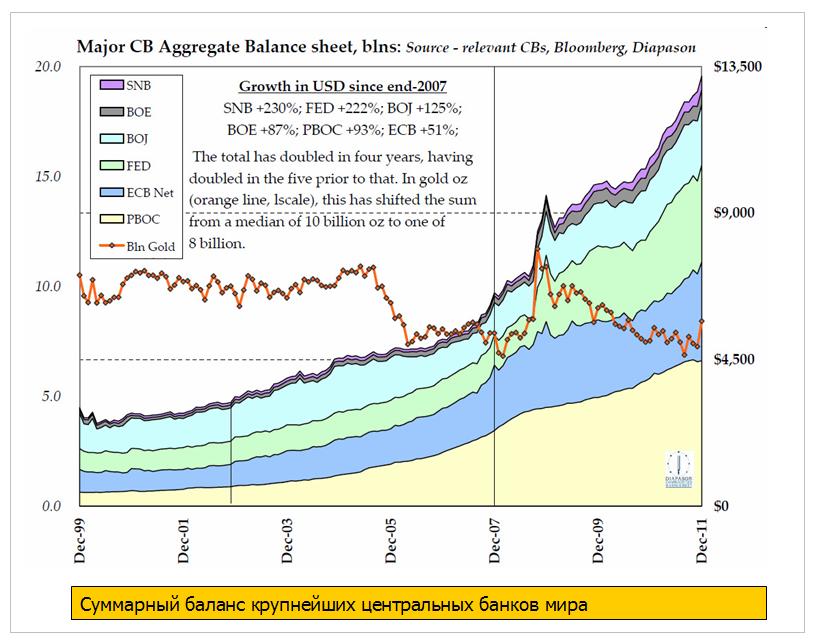

Wondering why the DJIA just passed 13K again? Wonder no more: as the chart below shows it is entirely due to the nearly $7 trillion pumped by global central banks into the world stock markets just in the past 4 years. As Sean Corrigan from Diapason notes, the aggregate global central bank balance sheet has doubled in four years, after doubling in the 5 years before that.

The European Central Bank wants its second offer of cheap ultra-long funds next week to be its last, putting the onus back on governments to secure the euro zone's longer-term future.

Powerful members of the central bank's 23-man governing council are privately hoping demand at the February 29 auction will fall well short of the 1 trillion euros some expect, backing their view that it should be the last.

Central bank sources say they are worried that banks will become too reliant on ECB funds, removing the incentive to restart lending between themselves.

Given the expectations priced into stocks (and remember credit has rallied but has recently started to weaken notably), any more hints by the ECB that LTRO 2 will be the last and that the liquidity spout is being shut down for now - leaving governments more responsible for growth - will not be taken well by the market.

Второй план помощи Греции: сроки, условия и ближайшие шаги

Successful PSI operation a necessary condition for a success of the program: now this is an issue, since the PSI will almost certainly fail and CACs will have to be enforced which bring up our question - is the usage of CACs in the "bailout" a Material Adverse Change clause, and is thus the loophole for collapsing the deal altogether?

Ближайшие шаги

German parliament will seek to approve deal Feb. 27

Finland expects to discuss bailout in week of March 12

Dutch Finance Minister Jan Kees de Jager has mooted possibility of waiting until after Greek elections (expected April 8), according to Rabobank

Увеличилась вероятность срабатывания CDS и условий CAC: это привдет к усилению волатильности

Позитивные моменты

Progress on Greek PSI: Relative to the tensions last week, progress has been made towards a substantial reduction of Greek debt through the PSI (estimated at EUR107bn, or 50% of 2011 GDP, will be pardoned), and a mutualisation of the remaining portion on the Euro area’s official sector’s balance sheet. As we have noted in the past, after the liability management exercise, the share of Greek liabilities still in private hands will be substantially reduced (and estimated to be roughly 25% by end-2014, including the part relating to the EFSF guarantee on new Greek debt).

Reduced risk of disorderly default: The introduction of a segregated account in which each quarter’s debt service will be paid in advance, together with a national law giving priority to debt servicing payments, should reduce the risk of a disorderly default and thus the systemic relevance of Greece.

Негативные моменты

Growth concerns: In its communiqué, the Euro group insists that the agreement is conditional on Greece fully implementing a revised adjustment program (official details of which, including crucial assumptions on expected nominal growth, are not yet available). To this end, surveillance by the ECB/EU/IMF ‘troika’ is strengthened. But with ongoing economic duress and the upcoming general elections, uncertainty remains around how fast the country will be able to bring its non-interest deficit (estimated at 2.5% of GDP in 2011) into surplus of at least 1.5% of GDP. And the slow progress so far in delivering politically unpopular structural reforms and privatizations are not reassuring. This may lead to further frictions with EMU partners, leaving the risk of Greece's EMU exit in place.

Increased likelihood of CDS: Moreover, higher losses inflicted on the private sector, involving the likely activation of CACs and the triggering of CDS, represent sources of near-term volatility.

Здесь также довольно подробно приводятся подробности участия официального и частного сектора

Между тем Китай переходит от валютных войн к торговым войнам

China just escalated currency wars into outright trade wars. Because as China Daily reports, "Chinese exports are set to get a tax boost." Translated: even as China pushes the CNY higher in infinitesimal and irrelevant increments to appease US Congress, it has just taken out the trade stimulus bazooka. Why? "Export tax rebates will be increased this year in response to an export decline triggered by the European debt crisis. The move, which Commerce Ministry officials said will be implemented when the time is appropriate, will be the first increase since 2009." Still think Europe is fixed? China's answer: nope.

Yeah, we had the same response as our readers when we saw that freak move in the EURUSD. Apparently, despite the fact that absolutely nothing has been resolved, Reuters just ran a headline that "Euro zone reaches deal on second Greek bailout package." And that is all it took for the EURUSD headline scanning algos to surge by 60 100 pips. That there nothing substantial in it, or that this is merely a rephrasing of the actual Bailout 2 announcement from before, is irrelevant. Here is what the actual Reuters report said.

Вот что сообщает Рейтерс:

Euro zone finance ministers struck a deal early on Tuesday for a second bailout programme for Greece that will involve financing of 130 billion euros and aims to cut Greece's debts to 121 percent of GDP by 2020, EU officials said.

"The financial volume (of the Greek package) is 130 billion euros and debt-to-GDP (will be) 121 percent. Now it's down to work on the statement," one official involved in the negotiations told Reuters.

Another official confirmed that the financing would total 130 billion euros with the aim of reducing Greece's debts from around 160 percent of GDP now to 121 percent by 2020.

The FT's Peter Spiegel has scoped up some additional details from the 10 page debt sustainability analysis that is at the basis of the latest Greek bailout talks. Some of the critical details:

"even under the most optimistic scenario, the austerity measures being imposed on Athens risk a recession so deep that Greece will not be able to climb out of the debt hole over the course of the new €170bn bail-out."

A German-led group of creditor countries – including the Netherlands and Finland – has expressed extreme reluctance since they received the report about the advisability of allowing the second rescue to go through.

A “tailored downside scenario” prepared for eurozone leaders in the report suggests Greek debt could fall far more slowly than hoped, to only 160 per cent of economic output by 2020 – far below the target of 120 per cent set by the International Monetary Fund

Under such a scenario, Greece would need about €245bn in bail-out aid, nearly twice the €136bn under the “baseline” projections.

“Prolonged financial support on appropriate terms by the official sector may be necessary,” the report said, a clear reference to the possibility that bail-out funds may be needed indefinitely.

Even in best case scenario country will need at least €50 billion on top of €136 billion.

A recapitalisation of the Greek banking sector, which originally was projected to cost €30bn, will now cost €50bn. A highly touted Greek privatisation plan, which originally hoped to raise €50bn, will now be delayed by five years and bring in only €30bn by the end of the decade.

Комментарий ZH:

Translated, this is yet another confirmation of what we have claimed all along - that Germany is no longer playing along.

Alphaville пишет в принципе о том же, но с некоторыми дополнительными деталями. Их взгляды и взгляды ZH практически совпадают: это пшик.

And from the FT’s Peter Spiegel, who has been leafing through the same leaked report:

The report makes clear why the fight over the new Greek bail-out has been so intense in recent days. A German-led group of creditor countries – including the Netherlands and Finland – has expressed extreme reluctance since they received the report about the advisability of allowing the second rescue to go through.

A “tailored downside scenario” prepared for eurozone leaders in the report suggests Greek debt could fall far more slowly than hoped, to only 160 per cent of economic output by 2020 – far below the target of 120 per cent set by the International Monetary Fund. Under such a scenario, Greece would need about €245bn in bail-out aid, nearly twice the €136bn under the “baseline” projections.

“Prolonged financial support on appropriate terms by the official sector may be necessary,” the report said, a clear reference to the possibility that bail-out funds may be needed indefinitely.

Even under the most favourable circumstances, Greece could need an additional €50bn in bail-out aid by the end of the decade on top of the €136bn in new funds until 2015 being debated at a crucial eurozone finance ministers’ meeting on Monday night. That “baseline” scenario includes projections that the Greek economy will stop shrinking next year and return to 2.3 per cent growth in 2014.

Несколько дополнительных ссылок из этой же статьи:

Обзор недели и ключевые события наступающей недели от Голдмана

Интересен комментарий относительно USD/JPY

What is interesting about the move in USD/JPY over the past month, is that it is once again co-moving with interest rate differentials after a notable breakdown in this relationship between mid-September last year to late January this. If the interest rate differential continues to widen, then USD/JPY may continue to move higher. However, FX is relative and we need to contemplate the prospect of QE3 from the FOMC likely in Q2. With the front ends of the curves in both Japan and the US likely to be anchored by indications that the respective central banks will keep rates on hold for years rather than months, there isn't much scope for interest rate differentials to widen significantly and support a much higher level for USD/JPY. The other recent relevant announcement for USD/JPY, was confirmation of so called 'stealth' intervention by MoF in early November after the significant intervention in spot on October 31. Ongoing fears of intervention may well also influence USD/JPY in the near term and the likelihood of a large Japanese trade deficit in January will keep potential Japanese policy measures on the radar screen.

Относительно платежного баланса

From a purely FX perspective, the US TIC data were a key piece of information last week. Foreign investors - both private and official - were net sellers of US assets in December. On the other had, US investors repatriated record amounts of foreign assets in December. Summing these flows up indicates still small inflows into the US, which leaves the US external balance negative for the Dollar.

Bob Janjuah: рынки настолько подвержены манипуляциям со стороны монетарных властей, что у меня нет четкого понимания, что же там происходит

Важно:

In the near term, LTRO2 at month-end is the next clear focus for markets, more so than Greece. If LTRO2 is USD1trn or more, the market will take that as a signal to load on more leverage, more risk and more ‘carry’. If LTRO2 is in the order of USD250bn to USD500bn, Risk Off will be the order of the day as markets will start to fear that central bankers are having to reign back-in their current policies, and that as a result we face another period where central bankers and policymakers fall back behind the curve. LTRO1 clearly took policymakers from behind to ahead of the curve, but this is an extremely fluid situation, where doing nothing is, in reality, the same as going backwards. As the skew of expectations is to a large LTRO2, a LTRO2 take-up in between these ranges is likely to be viewed with neutrality/mild disappointment.

The ECB, on its own and without judicial or parliamentary review, has swapped their Greek debt for new Greek debt that is not subject to any “collective action clause.” They did this unilaterally and without the consent of any other sovereign debt bond owners of Greek debt. They did this without objection of any nation in Europe. They have retroactively changed the indenture, the contract made by Greece with all of the buyers of their bonds, when the debt was issued. There is no speculation involved in these statements, there is no longer any guesswork on what might be; the ECB swapped their bonds for new Greek bonds with the assent of the Greek government and it is now a done deal.

...

We know now that the ECB can retroactively change the rules, change an indenture, so that if the ECB can do this with Greece then it can certainly do it with any sovereign debt in Europe.

We have just passed a clearly defined “break point” where the legal rules were changed to the great disadvantage of all the private debt holders. The risk of ownership of European sovereign debt is now infinitely more dangerous in my estimation than it was last week. We still do not know if the IMF will demand and receive the same special treatment but I assert that it no longer matters. The actions of the European Central Bank are all that was necessary to radically alter the value of European sovereign debt and it is just not me but any number of large financial institutions that are in shock given what has happened with one of the largest and most respected bond investors in the world telling me that “financial repression is the softer word for it.”

Христианская вера подталкивала и некоторых очень крупных европейских политиков к участию в военных провокациях США

And British Prime Minister Tony Blair long-time mentor, advisor and confidante said:

“Tony’s Christian faith is part of him, down to his cotton socks. He believed strongly at the time, that intervention in Kosovo, Sierra Leone – Iraq too – was all part of the Christian battle; good should triumph over evil, making lives better.”

Первичные дилеры увеличили количество трежерей в своем владении до рекордного максимума

В действительности, согласно последним данным от Резервного банка Нью-Йорка, за неделю по 8 февраля первичные дилеры увеличили свои вложения в облигации Казначейства на $37 млрд. до исторических максимумов в $102 млрд. Такой взрывной рост можно сравнить лишь приукрашиванием балансов (windows dressing) в конце кварталов. Драйвером выступили исключительно векселя и облигации со сроком погашения менее 3 лет, вложение в которые увеличились на . $37,7 млрд. Напомним, что благодаря сохранению нулевых процентных ставок до конца 2014г., облигации со сроком погашения до 3 лет являются функциональным эквивалентом векселям - или с точки зрения ликвидности эквивалентом кэшу, с дополнительным преимуществом, что эти бумаги могут приниматься в залог в операциях репо ФРС или кем-нибудь другим. В последний раз такое резкое увеличение концентрации у дилеров векселей было в начале 2009г., когда мир рушился, и когда вложения первичных дилеров выросли от нуля до десятков миллиардов за один день. Т.е вложения уменьшились лишь с началом QE1, когда снизились риски, и ещё больше упали в период после QE2. В настоящее время со стороны ФРС нет никакой поддержки, по крайней мере, публичной, и видимо, поэтому, первичные дилеры принялись сами покупать то, что даёт максимальную ликвидность, но не акции.

Рынки превращаются в разновидность игрового механизма, на котором скоро роботы будут торговать по новостям, создаваемым другими роботами. Думаю, что мы им не будем мешать...

As Mediabistro reports, "Forbes has joined a group of 30 publishers using Narrative Science software to write computer-generated stories. Here’s more about the program, used in one corner of Forbes‘ website

Автор материала в ActionForex пишет: "Лично я думаю, что политики выбрали наихудшее решение в отношении Греции." ОНи просто пытаются выиграть время.

I personally think the politicians will go for the worst solution, i.e., buying more time, as it's the only way the politicians feel they can control the domestic agenda both in Greece and in Europe. They do not want to implement any solution which entails asking local parliaments in Germany, Finland or Netherlands to ratify before the Greek and French election is done, but it is also the most risky scenario as it risks further aggravating Greek social unrest and I doubt the market will perceive it as a good solution.

Moody’s Investors Service placed the ratings of 109 financial institutions on review for possible downgrade, citing as reasons for the reviews · the difficult operating environment · weakening sovereign creditworthiness, as well as · challenges related to banks’ capital market activities.

The following are European banks and classes of their securities which are likely to face a downgrade to non-investment grade from the IG category as a result of this rating review:

Банк Японии принял решение о новой программе покупки активов

На заседании во вторник Банк Японии увеличил свой план выкупа активов на ещё ¥10 трлн. или около $130 млрд. Стоимость программы, включающую также льготные кредиты, выросла до ¥65 трлн. или $844 млрд. Камень преткновения, как говорится, заключается в общем ВВП Японии, который по последним данным был на уровне $6 трлн. (плюс/минус) и снижался. Что означает, что увеличение выкупа активов Банком Японии является функциональным эквивалентом $325 млрд. QE, объявленному ФРС.

Автор статьи подмечает, что в последнее десятилетие наметилась тенденция по снижению потребления не только автомобильного горючего, но и других видов энергии, в т.ч. и электрической.

ПО мнению двух аналитиков инвестиционных домов объем размещений на предстоящем LTRO будет меньше, чем ожидалось ранее

Here’s a pair of interesting analyst reactions to Friday’s details on eurozone central banks’ rules for accepting additional credit claims. It’s an expansion of eligible ECB collateral. But neither a free lunch – nor a source of easy carry – given the haircuts these assets (bank loans, from French real estate to Spanish public sector to Italian lease finance to Austrian SME, etc) will bear, it seems.

Он здесь хорошо пишет об условных рефлексах рынка; ассоциация, которую и я использовал не раз.

В данном случае важны только действия монетарных властей и ничего более, так как именно их активность или пассивность формируют те или иные условия, определяющие будущее состояние рынка. Я бы даже выразился точнее и, возвращаясь к научной терминологии, замечу, что определенные действия монетаристов формируют условные раздражители, которые в свою очередь влияют на рыночные ожидания.

К примеру, свежий statement от Федерального резерва вызвал "рефлекс собаки Павлова", и рынок тут же стал делать ставку на неминуемый запуск новых программ количественного смягчения, хотя до этого факта (если он состоится) еще есть довольно приличное количество времени. Тем не менее тут же упали ставки доходности по бумагам Казначейства, и соответственно пошли вниз процентные ставки на межбанковском рынке. Естественно, что в данной ситуации условия на рынке останутся такими, что негативные информационные потоки не смогут серьезно изменить обстановку, до тех пор пока не будет внешнего торможения условного рефлекса. Другой пример - это действия ЕЦБ, которые вызвали внутреннее торможение условных рефлексов и тоже сформировали определенные условия на рынке.

Вот примерно за счет действия подобных научных изысканий и происходят движения на финансовых рынках, и надо только выбирать, оказываться ли в положении "собаки Павлова" в определенные моменты рыночной истерии или эйфории или, "закрыв глаза и заткнув нос и уши", спокойно дожидаться, когда начнется торможение рефлексов. Как я уже отметил, самым важным аргументом для оценки существующей тенденции на рынках в наше время становится вовсе не факт какого-то события, а наличие условий, от которых и будет зависеть движение цен на активы.

Естественно, что эти условия определяются деятельностью монетарных властей, и можно сколько угодно обращать внимание на какую-нибудь статистику или новость, слушать мрачные пророчества "светлых умов", однако все это будет бесполезно, если нет необходимой основы для изменения ситуации. Поскольку идея немедленного мирового краха прочно «застряла» в умах рыночной массы, нет ничего удивительного в том, что при каждом новом «удобном» случае моментально возвращается иррациональный пессимизм, который «выжигал» рынки во второй половине прошлого года.

Мой блог называется «Дайджест рынка» и я стараюсь следовать этой миссии.

У меня есть обязательная программа, которая представлена тремя ежедневными статьями

1.Вью «Российский рынок сегодня».

Хотя я совсем не пишу о российском рынке, но здесь еще представлено два вполне достойных прогноза – Вануты и Александа Потавина, которые пишут в основном о российском рынке

2.Вью рынка

Это мой собственный развернутый анализ ситуации на рынке. В последнее время бывает достаточно большим по объему: 5000-7000 знаков и 4-5 рисункков. Если сказать о рынке особо нечего, то я объединяю его с вью №1.

3.Вью «Валютный рынок сегодня»

Здесь помимо собственных комментариев рынка я еще публикую очень достойные прогнозы двух аналитиков валютного рынка: Константина Бочкарева и Николая Корженевского

Это обзор я публикую обычно во второй половине, поскольку мне нужно дождаться выхода обзоров моих соавторов. Николай Корженевский раньше писал достаточно поздно: в 3-4 часа дня.

Представляю вашему вниманию новую ежедневную тему:

Тема называется LINKS-ДАЙДЖЕСТ

Это будет ежедневный ДАЙДЖЕСТ ссылок на аналитические материалы, главным образом англоязычные.

Здесь будут также копироваться важные цитаты из этих материалов, если их возможно выделить из статьи:

Это будут Bottom line (главные мысли)

Важное отличие этого типа материала:

ОН БУДЕТ ПОСТОЯННО ОБНОВЛЯТЬСЯ.

UPDATE FOREVER!!

Апдейт будет идти по двум направлениям:

1.Добавление новых ссылок

2.Перевод заголовка и отдельных, наиболее важных Bottom line

Таким образом, кому интересен подобный контент, я рекомендую его время от времени перечитывать. Спустя месяц статья может выглядеть уже совсем по-другому.

ВАЖНО: ИНФОРМАЦИЯ В РАЗДЕЛЕ LINKS-ДАЙДЖЕСТ БУДЕТ СТРУКТУРИРОВАНА.

Ссылки будут располагаться по темам.

В дальнейшем, даже если месяц спустя мне встретится материал, датированный этим днем, то я буду его добавлять в соответствующий LINKS: например это будет

LINKS-ДАЙДЖЕСТ 20.02.12

Если вы встретили интересный материал, то тоже можете привести здесь ссылку на него в комментариях и изложить какие-то важные мысли.