Месячные данные о покупках американских долгосрочных ценных бумаг зарубежными инвесторами публикуются во вторую пятницу каждого месяца.

Их нелегко найти в лабиринте сайта казначейства, а если нет прямой ссылки, то почти невозможно.

Для этого вначале надо зайти в Resource Center, а затем в Data-Chart-Center. Зачем они так запрятали эти важные данные – остается только гадать. Мультики найти на сайте Казначейства легче, чем данные TIC.

Вышедшие в эту пятницу данные содержат очень важную информацию. В апреле зарубежные инвесторы, официальные и частные, продали американских казначейских ценных бумаг на рекордную за все время ведения этой отчетности время сумму: 54,5 млрд. долларов. Зарубежные инвесторы также активно покупали в апреле MBS (23 млрд. долларов) и американские акции (11,2 млрд. долларов).

Таким образом, в апреле вовсю шла ротация зарубежных инвесторов из государственных облигаций в MBS (сектор недвижимости) и фондовый рынок.

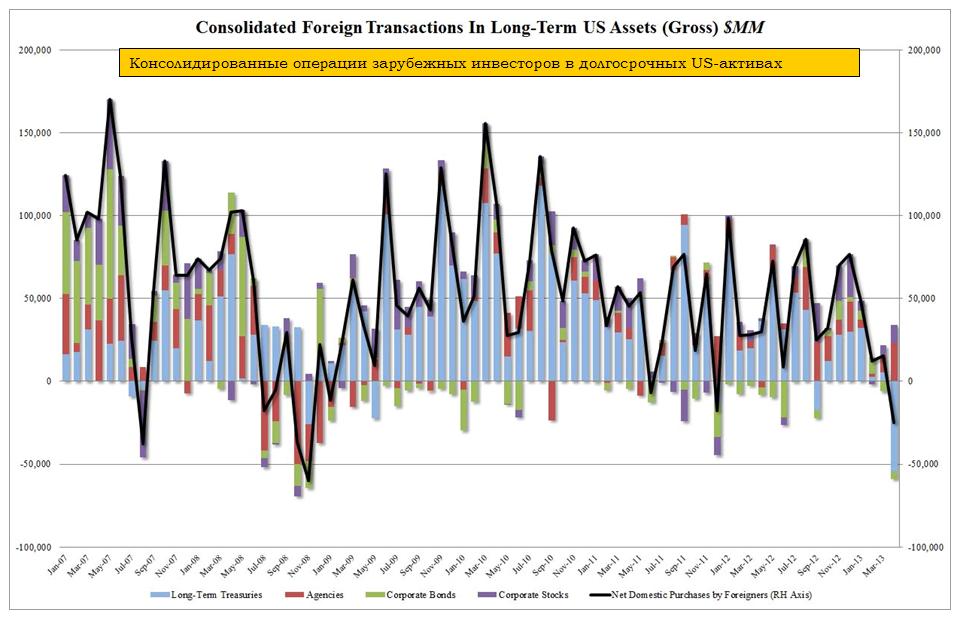

Zero Hedge дает нам график, как выглядели консолидированные операции зарубежных инвесторов в долгосрочных US-активах.

Парадоксальным при этом является то, что сами облигации в течении всего апреля росли. Таким образом, зарубежные инвесторы продавали US Treasuries весь месяц на росте. Возникает естественный вопрос: а кто обеспечивал этот рост? Ответ очевиден: их покупали в основном ФРС, первичные дилеры и некоторые хеджфонды (Jeff Gundlach, например, писал, что их покупал).

Из предыдущей статьи ясно, что календарный график погашений был, как будто, специально составлен таким образом, чтобы у первичных дилеров нашлись деньги на покупку US Treasuries.

Видимо, первичные дилеры при этом все-таки перенапряглись, поэтому в мае им пришлось активно продавать. Со 2 мая долгосрочные облигации, как видно из графика, перешли почти в отвесное падение. Уверен, что в мае зарубежные инвесторы их после рекордных продаж в апреле покупали.

Таким образом, мы наблюдаем не имеющие понятного смысла ротации капитала – то, что у нас называется переливание из пустого в порожнее, - и рост волатильности на важном для Америки рынке казначейских облигаций.

Эти ротации затрагивали и инвестиции в фондовые рынки.

Особый интерес представляет следущий рисунок: кто сколько продавал.

Больше всех продала Япония – на сумму 14 млрд. долларов.

Интересный вопрос: кто их продавал? Официальные или частные структуры структуры Японии? Мне это неизвестно.

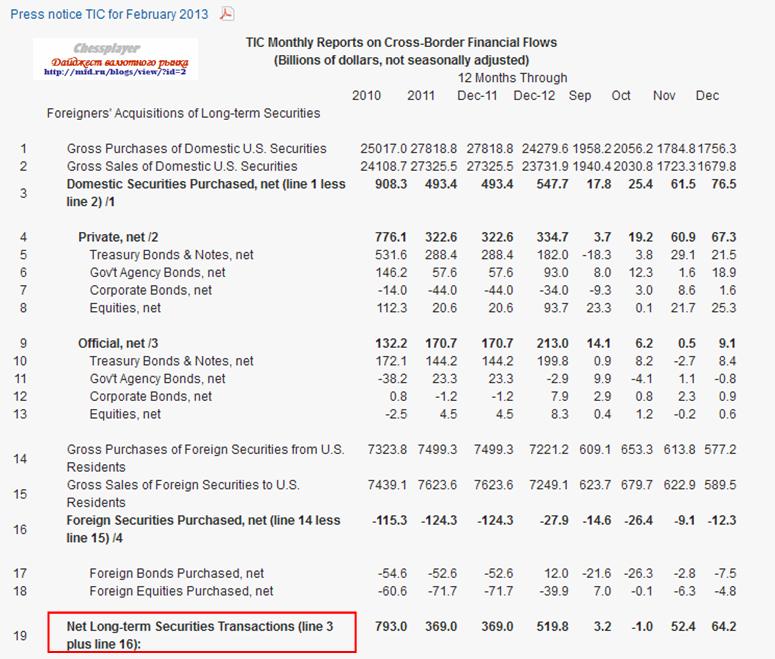

Смысл отчета TIC – получить представление о движение капитала при покупках/продажах ценных бумаг США иностранцами и иностранных ценных бумаг резидентами США.

Покупатели американских ценных бумаг подразделяются на частный сектор и официальный сектор (суверенные фонды).

На мой взгляд, значение этих данных в том. что они дают нам представление о долгосрочной дислокации активов.

Данные выходят с полуторамесячной задержкой. Так, например, 15 февраля выходят данные за декабрь месяц.

В этой таблице дана информация за каждый из последних двух лет, за последние 12 месяцев, за каждый из последних 4 месяцев.

Покупки ценных бумаг США подразделяются на покупки частными и государственными структурами (официальный сектор).

С точки зрения RORO (покупки риска)

Положительное сальдо Treasury Bonds & Notes= RISK OFF

Положительное сальдо Gov't Agency Bonds= RISK OFF

Положительное сальдо Corporate Bonds= RISK ON

Положительное сальдо Equities= RISK ON

Сами понимаете, что это достаточно условно. Особенно когда, взаимодействие активов сильно нарушено другими факторами, как сейчас.

Некоторые краткие наблюдения за отчетом:

Приток капитала частного сектора в рынок US Treasuries существенно замедлился в годовом выражении в 2012 году: меньше почти в 3 раза, чем в 2010 году, и почти в 2 раза, чем в 2011 году. Полагаю, что это отражает массированный переход инвесторов в EURO-активы.

Приток в рынок акций сохранился: на уровне хорошего 2010 года.

В последние два месяца возобновился приток капитала в рынок US Treasuries, хотя те в это время падали в цене. Полагаю, что с большой вероятностью в январе-феврале их тоже покупали.

В ноябре-декабре резиденты США выводили капитал из иностранных облигаций и акций. Таким образом, шла репатриация USD-валюты несмотря на то, что Федрезерв объявил о не имеющей срока окончания программе покупок US Treasuries. Фактически это означает, что ежемесячно происходит вливание 85 млрд. долларов ликвидности, тем не менее американские инвесторы не увеличили экспозицию на иностранные активы.

НА основании этих данных складывается впечатление, что USD продолжит расти.

Отчет TIC гораздо более детализированный и хранит в себе гораздо более интересную информацию: не о транзакциях, а непосредственно о дислокации активов. Об этом пойдет речь в следующем материале.

Данные выходят ежемесячно. Отчет достаточно объемный, и едва ли кто-то вникал в детали.

Отчет совершенствуется, в мае прошлого года здесь произошло важное добавление контента, о котором я тоже расскажу.

Скорее всего, подавляющее большинство из тех, кто следит за этим отчетом, ограничивалось наблюдением за одной цифрой, которая олицетворяет этот баланс.

Эта цифра отражает баланс между покупками и продажами долгосрочных ценных бумаг без учета типа этих бумаг.

В отчёте указывается баланс между покупками долгосрочных ценных бумаг, приобретённых гражданами США и иностранными инвесторами. Например, если иностранцы приобрели ценные бумаги на сумму 100 млрд долл, а граждане США - на сумму 30 млрд долл, баланс покупок долгосрочных ценных бумаг будет составлять 70 млрд долл.

Рискну взять на себя смелость утверждать, что главная цифра этого отчета – это абракадабра.

Итоговая цифра, которая берется из этого баланса - это строка 19.

Строка 19 = строка 3 + строка 16.

Строка 3 – это нетто покупок и продаж американских ценных бумаг иностранцами.

Строка 16 – это нетто покупок и продаж иностранных ценных бумаг резидентами США.

Они складывают, и в том и в другом случае, нетто покупок и продаж. Это мне представляется странным. Поскольку капитал при этом совершает движение в разные стороны.

По идее, они должны вычитать одну цифру из другой.

Может быть, я слишком самонадеян? Может мне не хватает финансового образования, чтобы понять, как нужно правильно считать?

Алгоритм расчета здесь внешне такой же. Но, в отличие от Казначейства США, в одном случае они берут нетто покупок/продаж (для нерезидентов), а в другом случае нетто продаж/покупок (для резидентов).

Если бы в первом случае из строки 3 вычли строку 16, то получили бы такой же результат.

Удивительный факт! В Японии и США считают этот показатель по-разному.

На мой взгляд, в Японии это делают правильно, а в США неправильно.

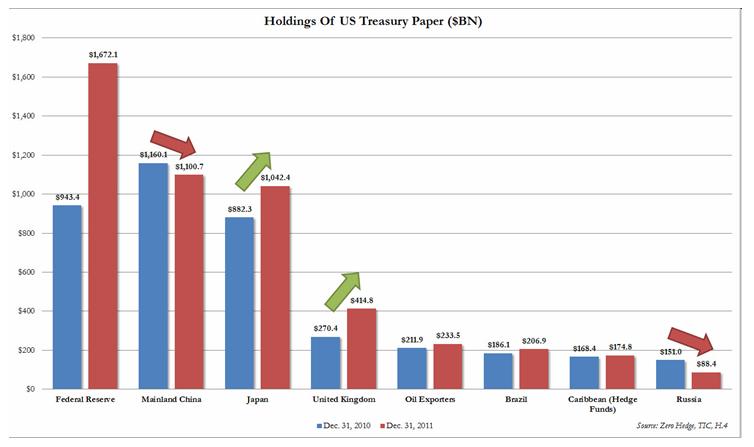

Китай в декабре продал трежерей на 100 млрд. долларов. Скрытым покупателем, действующим через Великобританию, является Россия.

First, here is a link to the revised TIC data as of this afternoon. That lack of Chinese trade surplus is really starting to bite not only China, but also the US, which as we noted last time, will be forced to rely ever more on domestically funded purchases of USTs: read Primary Dealers and the Fed, as the rest of the world developing world, also known as US Treasury buyers, clams down and exports far less to a recessionary Europe and contracting America. As the chart below shows, Chinese holdings are sliding, no matter how one cuts the data.

Yet the biggest surprise, is that contrary to previous speculation, Russia has not been dumping its Treasurys. In fact the country's holding of $150 billion are the same as they were back in June, and over $60 billion more compared to the pre-revised number.

In other words the biggest beneficiary of stealthy UK accumulation is no longer China (which is not accumulating US paper at all and quite the contrary), but Russia.

Чтобы получить представление о том, как поведут себя US Treasuries, нужно следить за китайским торговым профицитом. Если он вдруг превратился в дефицит, то это немедленно вызовет проблемы в US Treasuries.

Then again, this is the TIC data, which is notoriously wrong all the time. Best advice: keep a track of that Chinese trade surplus. If it becomes a deficit (just like Japan did recently), that is the first signal that things are changing dramatically from an international flow of funds perspective. It also means that unless the US finds subtitute demand, most likely from within, the only remaining buyer will be the entity that already has the largest holding of US paper - the Federal Reserve.

A month ago, Zero Hedge readers were stunned to learn that unemployment among Europe's young adults has exploded as a result of the European financial crisis, and peaking anywhere between 46% in the case of Greece all they way to 51% for Spain. Which makes us wonder what the reaction will be to the discovery that when it comes to young adults (18-24) in the US, the employment rate is just barely above half, or 54%, which just happens to be the lowest in 64 years, and 7% worse than when Obama took office promising a whole lot of change 3 years ago.

Федрезерв возобновляет обратные репо: надо изымать долларовую ликвидность.

В принципе это является бычьим сигналом для USD.

Dumping yet another liquidity cold shower in the aftermath of today's less than dovish Humphrey Hawkins speech by Bernanke (and sending precious metals even lower, albeit briefly), is the Fed's resumption of even more purely optical liquidity extractions, however symbolic, in the form of reverse repos, after the NY Fed just completed the first such operation since the dark days of summer 2011. As a reminder, the last time the Fed did these was back in August 2011 which cemented the market's plunge as it gave the market the impression that at least superficially no more money was coming in (intuitively it makes no sense to have Reverse Repos running at the same time as incremental liquidity), even as the reliquification baton was quietly being passed to the ECB. Today, reverse repos resume, as the Fed pays Primary Dealers an annualized rate of 0.17% in exchange for lending out $100 million in Treasurys. Will this continue? It depends entirely on what the economy, pardon, the Russell 2000 does. After all, that is the third and only mandate of the Fed that matter. And if the market considers this an indicator that QE3 really is delayed indefinitely, the FRBNY will mostly likely be forced to reassess.

Европейская команда MS отвечает на наиболее часто дискутируемые вопросы, касающиеся QE.

Morgan Stanley's European Economics Team asks and answers five of the most frequently discussed questions with regard quantitative easing. From whether QE has worked to inflation fears and concerns over policy normalization and what happens if the public lose confidence in central bank liabilities, we suspect these questions, rather dovishly answered by the MS team, will reappear sooner rather than later, and as they interestingly note, the deployment of central bank balance sheets is, in essence, a confidence trick.

Греки сейчас делают две основные вещи: они бастуют и забирают деньги из банков

Just like the housing market in the US, following the modest blip higher in December Greek bank deposits, immediately the great unwashed took to calling an end of the Greek deposit outflow and seeing a glorious renaissance for the country's bank industry. Well look again. According to just released data from the Bank of Greece, January saw Greeks doing what they do best (in addition to striking of course): pulling their money from local banks, after a near record €5.3 billion, or the third highest on record, was withdrawn from the local banking system. As a result, total bank cash has now dropped to just €169 billion, down from €174 billion in December, and the lowest since 2006. This is an 18% decline from a year ago, or €37 billion less than the €206 billion last January, and is a whopping 30% lower than the all time deposit highs from 2007, as nearly €70 billion in cash has quietly either left the country or been parked deep in the local mattress bank.

Странный во многих отношениях график, который предоставил Peter Tchir

Everyone and their mum knows by now that Italian bonds have rallied since the first LTRO and we are told that this is symptomatic of 'improvement'. While we hate to steal the jam from that doughnut, we note Peter Tchir's interesting chart showing how focused the strength is in the short-end of the bond curve (which we know is thanks to the ECB's SMP program preference and the LTRO skew) but more notably the significantly less ebullient performance of the less manipulated and more fast-money, mark-to-market reality CDS market as we suspect, like him, the CDS is pricing in the longer-term subordination and termed out insolvency risk much more clearly than the illiquid bond market does, and perhaps bears closer scrutiny for a sense of what real risk sentiment really looks like.

Рынок CDS показывает риск неплатежеспособности гораздо более отчетливо, чем рынок бондов.

Back in late November (pre LTRO and more SMP), the CDS spread was lower than the bond yield across the board (we could look at Italian bond spread to German bunds, or Italy CDS spread to German CDS). We have seen a very big move in bond yields. Yields have moved lower across the board, with the front end outperforming. CDS has moved tighter, but not by as much, and the curve when from slightly inverted, to slightly steep.

In fact, CDS spreads are now higher than bond yields (significantly so) in the 1 to 3 year range.

It would tell me that the less manipulated market, less subject to non mark to market accounting, has been less convinced by the move. I would hate to say “smart” money vs “dumb” money, but a bigger % of investors in the bond market are not subject to mark to market and are not subject to being right in the short term (or with all the bailouts – being right at all). We have also seen evidence in Greece, that the ECB’s SMP program likes the short end more than the long end, creating another artificial buyer, and they are DEFINITELY senior. So maybe CDS with less manipulation is a better assessment of risk. Since that tends to be fast money and mark to market money, it is interesting to see how much above bond yields they are willing to pay (though liquidity is low in sovereign CDS too). Maybe the CDS market is already pricing in the subordination that will occur if there is another crisis. The bond market can’t help but be pulled to the level of the ECB bid (though SMP has been quiet for 3 weeks), whereas CDS can anticipate the impact of subordination if things get bad again?

I’m not really sure what the answer is, but think this is worth watching (though in this market, the ECB will now finally get permission to sell CDS, or ban it, because who wants anything out there not fully controlled by the central banks).

ZH с обычным сарказмом пишет о статистических данных.

Earlier today, when forecasting the Chicago PMI, we warned to "expect another massive beat courtesy of consumers confident that they can have Apple apps, if not so much food, since they still don't pay their mortgages." Sure enough, the economic data is now straight out of China, with the Chicago PMI not only trouncing expectations, printing at 64, on consensus of 61 (the highest since last April when the peak of the liquidity bubble popped and the stock market rolled over), but, wait for it, the Employment index came at 64.2, up from 54.7, which was the highest employment print since April 1984! At this point it is no longer worth commenting on economic data, as between this, the NAR, the consumer confidence, it was all become farce of a blur. we now expect February unemployment to print negative as the labor participation rate slides to 50%, and seasonal adjustments and birth/date fixtures account for 5 million "additions" to jobs. One thing that is sure. There will be no more easing for a looooooooong time. Kiss any hope of more trillions in central bank liquidity goodbye.

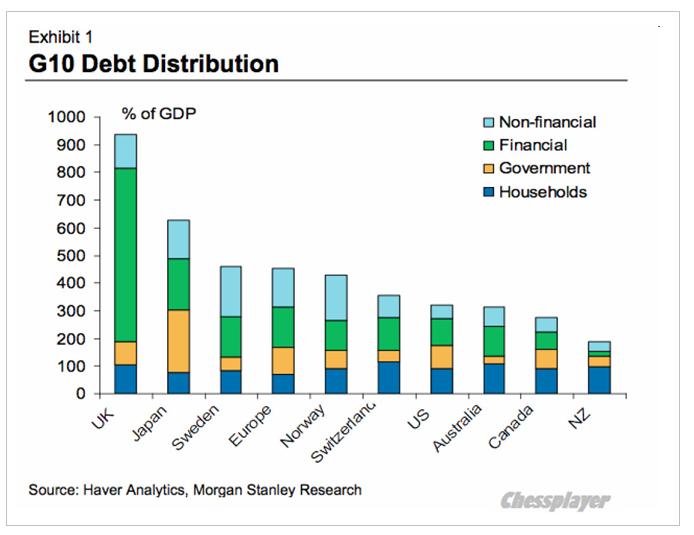

Три графика, которые показывают, что несмотря на накачку экономики деньгами, доля кредита сокращается.

While the narrower spreads in Europe created the unintended consequence of perversely reducing the urgency for banks to delever their over-stuffed balance sheets (and in fact in many cases likely make them worse thanks to the ECB), the US Household continues to (sensibly) slowly but surely reduce their leverage. As today's Bloomberg Brief notes though, the slow pace of deleveraging will continue to weigh on growth over the next few years - even as they have drawn down debt as a percentage of personal income from its peak in June 2009 at 114.76% to 101.1% at the end of 2012. There is a long way to go to the apparent Maginot line of supposedly sustainable 90% and with wage growth stagnant, the bulk will come from debt reduction in true balance-sheet-recession style - putting still more pressure on a perniciously polarized government to do anything about it.

У португальских банков нет такого покровителя, как Драги, и покупать португальский долг некому....

As the ECB has stopped its SMP bond-buying and now the LTROs are all done (until the next one of course), Portuguese bond spreads have been increasing rapidly and post-LTRO today even more so. While broadly speaking European sovereign risk is modestly higher this week (and notably steeper across the curve) leaving funding costs still very high for most nations, Portugal has exploded over 100bps wider (and almost 70bps of that today post-LTRO) to back over 1200bps wider than Bunds. Only Italian bonds are better and even there they are leaking back to unch from pre-LTRO. Perhaps, shockingly, more debt did not solve the problem of too much debt and with growth and deficits being questioned in Ireland and Portugal (and Spain), it's clear the newly collateralized loan cash the banks have received won't be extended to the medium-term maturities in sovereign bonds.

Налоговый климат в Америке в 2013 году обещает быть очень сложным.

As he notes the radically changed taxation climate in 2013 and beyond will have an impact on all economic participants as they will probably opt to bolster their cash reserves in the second half of the year in preparation for the proverbial rainy day.

As the chart below, which highlights some of the biggest and most notable holders of US paper, shows, in the period December 31, 2010 to December 31, 2011, there have been two very distinct shifts: those who are going all in on the ponzi, and those who are gradually shifting away from the greenback, and just as quietly, and without much fanfare of their own, reinvesting their trade surplus in something distinctly other than US paper. The latter two: China and Russia, as we have noted in the past. Yet these are more than offset by... well, we'll let the readers look at the chart below based on TIC data and figure out it.

Про состоявшийся аукцион по размещению 2-year US notes: ничего примечательного

Tim Geithner just sold $32 billion in 2 year bonds at a rate of 0.31%, right on top of the When Issued, which was the highest yield since August 2011, yet nothing too dramatic. Since this is the short end of the curve where Bernanke is fully in control, the range in recent auctions has fluctuated from 0.222% to 0.31%. Yet as noted last week, the biggest "beneficiary" of short-end purchases have been Primary Dealers - are they starting to choke on thier holdings? And who will they sell to this paper which yields absolutely nothing. The auction internals were a snooze - the Bid To Cover was 3.54, a drop from January's 3.75, but higher than the TTM average of 3.42. Dealers took down 54.66%, in line with the average, Indirects left holding 35.84%, and 9.5% for the direct. Overall, nothing to write home about, and the bottom line is that the US just added another $32 billion to its net debt of $15.413 trillion, or a new record high debt/GDP ratio of 101%. It is going much higher.

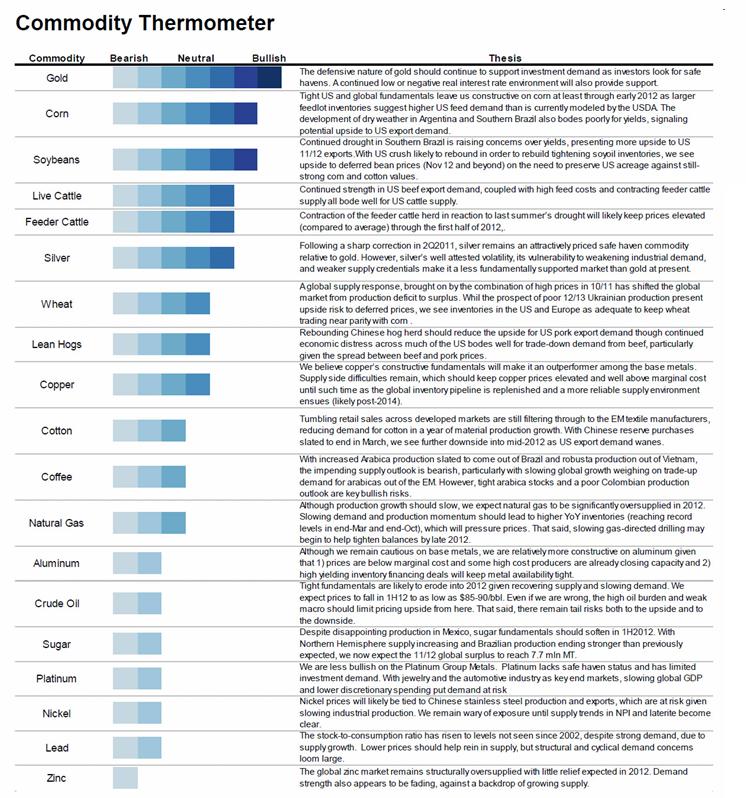

Представляем Commodity Thermometer от Morgan Stanley

По сути это прогноз на 2012 год.

...here is a simple way to gauge relative commodity strengths and weakness courtesy of Morgan Stanley's "Commodity Thermometer" which shows what products MS is bullish and bearish on, and why.

Это интересно! Если плохо видно - можно пройти по ссылке!

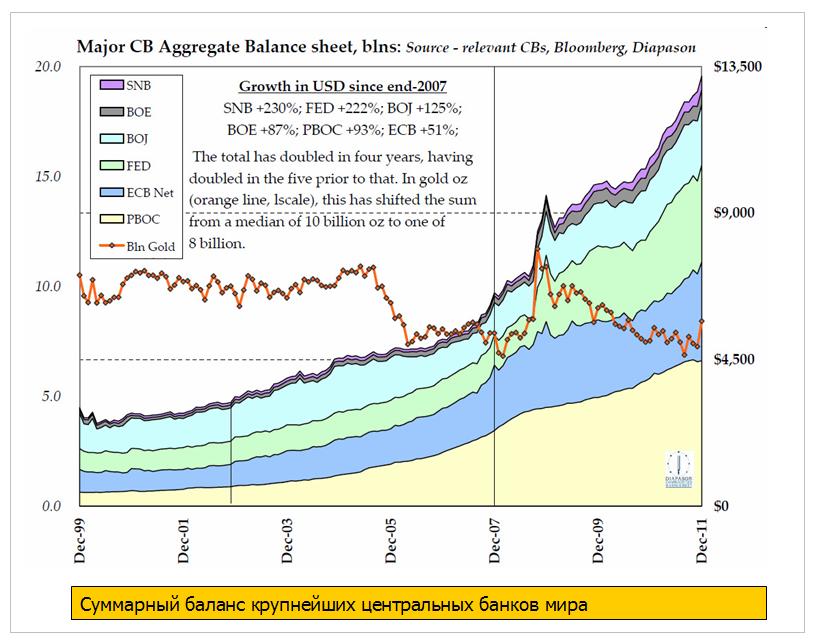

Wondering why the DJIA just passed 13K again? Wonder no more: as the chart below shows it is entirely due to the nearly $7 trillion pumped by global central banks into the world stock markets just in the past 4 years. As Sean Corrigan from Diapason notes, the aggregate global central bank balance sheet has doubled in four years, after doubling in the 5 years before that.

The European Central Bank wants its second offer of cheap ultra-long funds next week to be its last, putting the onus back on governments to secure the euro zone's longer-term future.

Powerful members of the central bank's 23-man governing council are privately hoping demand at the February 29 auction will fall well short of the 1 trillion euros some expect, backing their view that it should be the last.

Central bank sources say they are worried that banks will become too reliant on ECB funds, removing the incentive to restart lending between themselves.

Given the expectations priced into stocks (and remember credit has rallied but has recently started to weaken notably), any more hints by the ECB that LTRO 2 will be the last and that the liquidity spout is being shut down for now - leaving governments more responsible for growth - will not be taken well by the market.

Второй план помощи Греции: сроки, условия и ближайшие шаги

Successful PSI operation a necessary condition for a success of the program: now this is an issue, since the PSI will almost certainly fail and CACs will have to be enforced which bring up our question - is the usage of CACs in the "bailout" a Material Adverse Change clause, and is thus the loophole for collapsing the deal altogether?

Ближайшие шаги

German parliament will seek to approve deal Feb. 27

Finland expects to discuss bailout in week of March 12

Dutch Finance Minister Jan Kees de Jager has mooted possibility of waiting until after Greek elections (expected April 8), according to Rabobank

Увеличилась вероятность срабатывания CDS и условий CAC: это привдет к усилению волатильности

Позитивные моменты

Progress on Greek PSI: Relative to the tensions last week, progress has been made towards a substantial reduction of Greek debt through the PSI (estimated at EUR107bn, or 50% of 2011 GDP, will be pardoned), and a mutualisation of the remaining portion on the Euro area’s official sector’s balance sheet. As we have noted in the past, after the liability management exercise, the share of Greek liabilities still in private hands will be substantially reduced (and estimated to be roughly 25% by end-2014, including the part relating to the EFSF guarantee on new Greek debt).

Reduced risk of disorderly default: The introduction of a segregated account in which each quarter’s debt service will be paid in advance, together with a national law giving priority to debt servicing payments, should reduce the risk of a disorderly default and thus the systemic relevance of Greece.

Негативные моменты

Growth concerns: In its communiqué, the Euro group insists that the agreement is conditional on Greece fully implementing a revised adjustment program (official details of which, including crucial assumptions on expected nominal growth, are not yet available). To this end, surveillance by the ECB/EU/IMF ‘troika’ is strengthened. But with ongoing economic duress and the upcoming general elections, uncertainty remains around how fast the country will be able to bring its non-interest deficit (estimated at 2.5% of GDP in 2011) into surplus of at least 1.5% of GDP. And the slow progress so far in delivering politically unpopular structural reforms and privatizations are not reassuring. This may lead to further frictions with EMU partners, leaving the risk of Greece's EMU exit in place.

Increased likelihood of CDS: Moreover, higher losses inflicted on the private sector, involving the likely activation of CACs and the triggering of CDS, represent sources of near-term volatility.

Здесь также довольно подробно приводятся подробности участия официального и частного сектора

Между тем Китай переходит от валютных войн к торговым войнам

China just escalated currency wars into outright trade wars. Because as China Daily reports, "Chinese exports are set to get a tax boost." Translated: even as China pushes the CNY higher in infinitesimal and irrelevant increments to appease US Congress, it has just taken out the trade stimulus bazooka. Why? "Export tax rebates will be increased this year in response to an export decline triggered by the European debt crisis. The move, which Commerce Ministry officials said will be implemented when the time is appropriate, will be the first increase since 2009." Still think Europe is fixed? China's answer: nope.