S&P500 вчера всего чуть-чуть не дошел до 1400 пунктов (максимум составил 1399,63) и коснулся верхней ленты Боллинджера. Американские трейдеры обычно чутко реагируют на этот технический сигнал перекупленности. Вероятность выйти за пределы лент Боллинджера составляет всего порядка 11%.

Put/call-коэффициент равен 0,80 – очень бычье значение. Это согласуется с настроением на Ticker Sense, где Bullish/Bearish (Быки/Медведи)=52/28

Опрос, напомню, проводится по четвергам.

Приближается еще одна техническая модель – двойная вершина. Полагаю, что в районе 1410 пунктов по индексу S&P500 эта фигура уже будет очень сильно сказываться, ведя к массированным продажам.

Так, например, рассуждал вчера ставший популярным в последнее время очень адекватный Peter Tchir (публикующий регулярно свою диспозицию активов) :

For now I remain long, but a bit cautious as we have had such a big run. I think U.S. CDS has incredible room to tighten and offers even better value than bonds. I like Spain and Italy, both stocks and bonds, but am small as these remain high beta. Banks should do well. The LIBOR hangover is still there, but with Europe possibly getting fixed and CDS doing better and housing showing signs of improvement, the banking sector should outperform, and the reality that LIBOR lawsuits will be complex and take a long time also helps on banks. I will be out of any S&P by 1,410 and likely to be short by 1,425, if not sooner.

Основные идеи:

Пока я остаюсь в лонге, но при этом становлюсь более осторожен, поскольку мы совершили такое сильное движение...

Мне нравятся Испания и Италия, как акции, так и бонды, но у меня маленькая позиция, т.к. здесь сохраняется слишком высокая бета (волатильность). Банки смотрятся хорошо.

Но, наиболее важно наверно следующее:

Я выйду изо всех акций в S&P500 к 1410 пунктам, и вероятно уже к 1425 пунктам буду в шорте, если не раньше.

Полагаю, что подобная оценка рыночной ситуации является сейчас типичной.

Рынок сейчас очень тонкий, и находится целиком во власти крупных игроков – маркетмейкеров.

Судя по настроениям инвесторов и put/call-коэффициенту, многие еще остаются в лонгах.

Не думаю, что выше 1420 пунктов по индексу S&P500 кто-то будет активно стопить свои короткие позиции. Следовательно, маркетмейкерам нет смысла тащить рынок в эту область, давая возможность Peter Tchir и другим опытным трейдерам возможность сдать свои лонги и открыть практически безрисковые короткие позиции.

Сегодня 7 августа и до традиционной встречи банкиров в Джексонхолле остается меньше двух недель.

Для меня лично совершено нелепой представляется идея отыгрывать запуск QE3 в сентябре при значениях индекса S&P500 выше 1400 пунктов.

Дерево вариантов на эту неделю.

1.Максимум, что может сделать рынок – выйти в район 1420 пунктов. Но, вероятность этого мала – не более 20-30%.

2.Гораздо более вероятна коррекция с последующей консолидацией в диапазоне 1360-1400 пунктов. Вероятность – порядка 50%.

3.Разворот и начало последующего (продолжительного) движения вниз. Это будет среднесрочный тренд, который уведет индекс S&P500 в течение ближайших 1-1,5 месяцев примерно в район 1220-1240 пунктов. Вероятность – порядка 20-30%.

Такая коррекция, если она случится, станет хорошей предпосылкой для запуска новой программы QE в конце года.

На этой неделе вариант 3 во многих случаях может совпасть с вариантом 2.

Единственное, что может толкнуть рынки вверх помимо беспочвенных ожиданий QE3 – это какой-то позитив относительно решения европейского долгового кризиса.

Но, учитывая, что сейчас здесь, после двух выступлений Драги наступила разрядка, вероятность, что власти еврозоны предпримут какие-то шаги – очень мала.

Им свойственно что-то предпринимать только когда сложилась критическая ситуация.

На уровнях 1400 пунктов по индексу S&P500 и выше вербальные интервенции малоэффективны и едва ли нужны.

ЦБ Кореи снизил долю американского доллара в своих ЗВР до минимального уровня с 2007 г., когда началась публикация подобной статистики.

Корея снижает долю долларов и евро в своих ЗВР и покупает юани

Доллар занимает 60,5% от общего объема ЗВР Южной Кореи, которые на начало 2012 г. составляли $306,4 млрд. Годом раньше в долларах хранилось 63,7% от всех запасов.

Монетарные власти Кореи взяли курс на повышение разнообразия валют: за последний год они увеличили доли австралийского доллара и китайского юаня, в то время как количество долларов и евро уменьшилось.

ЦБ Кореи увеличил долю акций в своем портфеле с 3,8% в начале 2011 г. до 5,4% в начале 2012 г. Доля гособлигаций увеличилась на 1% до 36,8%.

Дефляция постепенно отступает: индекс потребительских цен впервые за последние 5 месяцев демонстрирует положительную динамику. Он увеличился на 0,2% м/м и на 0,1% г/г.

По прогнозам экспертов статистического отдела Министерства внутренних дел Японии, в марте промпроизводство вырастет на 2,6% и на 0,7% в апреле. Последний прогноз ОЭСР указывает на то, что темпы роста японской экономики станут самыми заметными среди развитых стран. В I квартале ВВП страны увеличится на 3,4%.

Республиканец Jeff Sessions нашел разрыв в доходах и расходах по социальным статьям в 17 трлн. долларов.

That someone is Republican Jeff Sessions who after actually running the numbers has uncovered that the true long-term funding gap is a mind-boggling $17 trillion, just a tad more than the original sub $1 trillion forecast. This latest revelation means that total underfunded US welfare liabilities: Medicare, Medicaid and social security now amount to $99 trillion! Add to this total US debt which in 2 months will be $16 trillion, and one can see why Japan, which is about to breach 1 quadrillion in total debt (yen, but who's counting), may want to start looking in the rearview mirror for up and comer competitors. And while Obama may have been taking creative license with a number that is greater than total US GDP, he was most certainly correct when saying that Obamacare would not add a penny to US debt. Because the second the US government comes to market to fund a true total debt/GDP ratio of 750%, it is game over, and the Fed will have its hands full selling Treasury puts every waking nanosecond to have any time left for the daily 3pm stock market ramp.

Региональный долг Испании значительно увеличился в последнее время

Spanish regional debt currently stands at 13% of GDP and has surged from EUR60bn in 2006 to over EUR140bn currently. As Credit Suisse points out, the top four regions account for the majority of GDP, two-thirds of regional debt, and, with the exception of Madrid, substantially missed their deficit targets. What is more worrisome is the heavily front-loaded nature of the maturing debt with substantial refinancing needs in the next 2 years and this regional debt is split between bonds and loans - with many of the latter from Spanish banks - yet another illustration of the interconnected contagion that is building more rapidly. The growing crisis in refinancing (liquidity and costs) for regional debt developed the idea of Ponzibonos 'Hispabonos' - debt issued by regions but guaranteed by the central government. The conditionality of these guarantees with regard to deficit targets wil be critical but once they are issued, the risk is that the regions are unable to get their finances under control, the Spanish debtload increases, and there is no longer the flexibility for a regional debt restructuring, should one be necessary.

Банки так загружены акциями, что у них нет другого выбора, как продолжать ралли.

Yup - the banks are so loaded up with toxic stocks that they have NO CHOICE but to keep the ramp accelerating higher and higher until "stupid" retail comes back in and distribution happens, leaving the retail investor holding the hollow bag again. Alas, there were no inflows this week either. Which means that just like Italian banks, the meltup could well accelerate even more from here.

European Sovereign Yields have been under pressure for most of the last month...seems the market doesn't buy the firewall idea...

Почему не работает идея EFSF/ESM?

So at some point in the near future there will be about €40 billion of money sitting in the ESM and a bunch of promises from countries failing to live up to existing debt obligations, and that is the big firewall? The correlation between who is providing the guarantees and who will need them cannot be ignored. This new €500 billion number doesn’t exist, it’s not just meaningless, it’s non-existent if Italy or Spain needs money.

People can take away whatever they want, but unlike LTRO which had real injections of liquidity, this is just like the July plans from last year and the November “grand” plans. It sounds great, especially when too many people are willing to blindly follow what the politicians want them to, but it doesn’t work in practice.

Все разговоры о размерах фондов EFSF/ESM – обман с целью отвлечь внимание. Это лишь обещание заплатить, а не сами деньги.

When considering the financial condition of each and every country in the European Union there are certain facts that are left out and left out on purpose. In our opinion, the structural deformity of the European Union is, in itself, one of the main reasons that any attempt at a fiscal or economic fix never seems to work. Whether some proposed firewall is $760 billion or $1.3 Trillion or $13 Trillion makes no difference as in zero, nada, nothing and null. It is an IOU, a promise to pay and it is not counted in any European sovereign debt numbers nor is it counted in the figures for the European Union’s debt. It will not stop Spain or Portugal or Italy from asking for or needing money. This whole discussion is a head fake, a deception and a ruse carefully plotted out for investors in one more attempt to mislead the entire world. If you wish to be a statistic in the Greater Fool Theory be my guest but I refuse to be apart of this unadulterated scam.

Германский Бундесбанк отказался принимать в залог бонды, гарантированные государствами, получившими помощь от Евросоюза и МВФ

Germany’s Bundesbank is the first of the 17 euro-area central banks to refuse to accept as collateral bank bonds guaranteed by member states receiving aid from the European Union and the International Monetary Fund, Frankfurter Allgemeine Zeitung reported.

And what happens then? Since it is inevitable that Spain and Italy will be next on the bailout wagon, what happens when over $2 trillion in bonds suddenly become ineligible for cash collateral from the only solvent central bank in the world (aside for that modest, little TARGET2 issue of course). Will it force the ECB to be ever more lenient with collateral, and how long until the plebs finally realize that the ECB has been doing nothing but outright printing in the past 5 months? What happens to inflationary expectations then?

Джим Грант критикует политику Федрезерва. Очень классная статья!

I can’t help but feel slightly hypocritical in dressing you down. What passes for sound doctrine in 21st-century central banking—so-called financial repression, interest-rate manipulation, stock-price levitation and money printing under the frosted-glass term “quantitative easing”—presents us at Grant’s with a nearly endless supply of good copy.

....

One can think of the original Federal Reserve note as a kind of derivative. It derived its value chiefly from gold, into which it was lawfully exchangeable. Now that the Federal Reserve note is exchangeable into nothing except small change, it is a derivative without an underlier. Or, at a stretch, one might say it is a derivative that secures its value from the wisdom of Congress and the foresight and judgment of the monetary scholars at the Federal Reserve. Either way, we would seem to be in dangerous, uncharted waters.

.................................

As you prepare to mark the Fed’s centenary, may I urge you to reflect on just how far you have wandered from the intentions of the founders? The institution they envisioned would operate passively, through the discount window. It would not create credit but rather liquefy the existing stock of credit by turning good-quality commercial bills into cash— temporarily. This it would do according to the demands of the seasons and the cycle. The Fed would respond to the community, not try to anticipate or lead it. It would not override the price mechanism— as today’s Fed seems to do at every available opportunity—but yield to it.

Ladies and gentlemen, such stability as might be imposed on a dynamic capitalist economy is the kind that eventually comes around to bite the stabilizer.

..............................

“Price stability” is a case in point. It is your mandate, or half of your mandate, I realize, but it does grievous harm, as defined. For reasons you never exactlyspell out, you pledge to resist “deflation.” You won’t put up with it, you keep on saying—something about Japan’s lost decade or the Great Depression. But you never say what deflation really is. Let me attempt a definition. Deflation is a derangement of debt, a symptom of which is falling prices. In a credit crisis, when inventories become unfinanceable, merchandise is thrown on the market and prices fall. That’s deflation.

What deflation is not is a drop in prices caused by a technology-enhanced decline in the costs of production. That’s called progress.

............................................

Much the same sentiments, and much the same circumstances, apply today, but with a difference. Digital technology and a globalized labor force have brought down production costs. But, the central bankers declare, prices must not fall. On the contrary, they must rise by 2% a year. To engineer this up-creep, the Bernankes, the Kings, the Draghis—and yes, sadly, even the Dudleys—of the world monetize assets and push down interest rates. They do this to conquer deflation.

But note, please, that the suppression of interest rates and the conjuring of liquidity set in motion waves of speculative lending and borrowing. This artificially induced activity serves to lift the prices of a favored class of asset—houses, for instance, or Mitt Romney’s portfolio of leveraged companies. And when the central bank-financed bubble bursts, credit contracts, leveraged businesses teeter, inventories are liquidated and prices weaken. In short, a process is set in motion resembling a real deflation, which then calls forth a new bout of monetary intervention. By trying to forestall an imagined deflation, the Federal Reserve comes perilously close to instigating the real thing.

Структурные проблемы предстоит еще решать, а экономике восстанавливаться после приема «чрезвычайных медицинских средств».

In his latest note published in Project Syndicate, El-Erian says there are structural problems that need to be addressed. He cautions against complacency and says the economy needs to recover from the "extreme medicine it received" i.e. fiscal stimulus and other policies enacted by the Fed:

But legendary value investor Doug Kass isn't having any of it. He goes so far as to exclaim, "I can't help but think that Goldman Sachs might have rung the bell that the market has topped in the near term!" in an editorial published by The Street today.

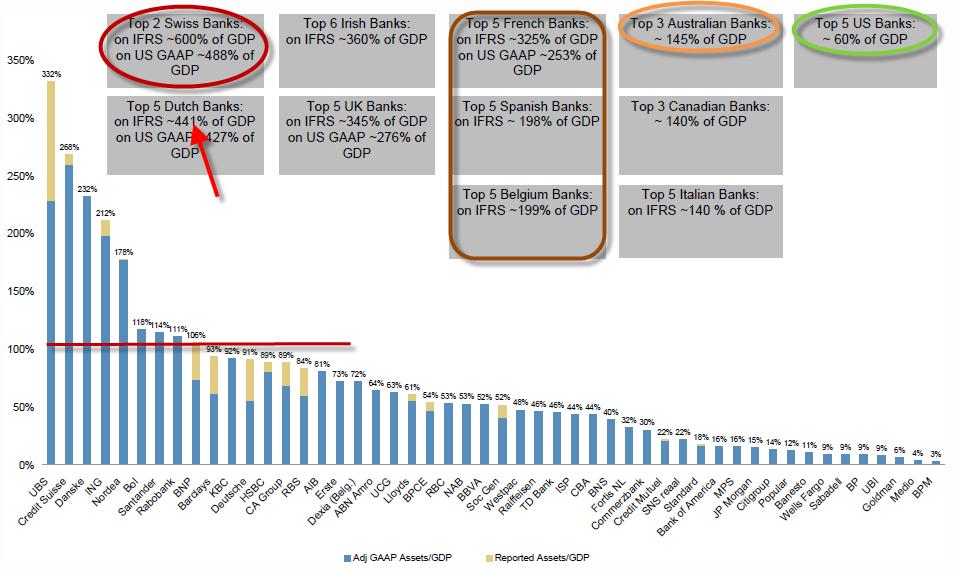

Три графика, которые показывают, что еврокризис никогда не закончится

If ever there were banks that were truly Too-Big-Too-Fail, Europe has them - is it any wonder the Greek Bailout was so focused on rescuing the bank balance sheets. Swiss banks dominate the worst end of the spectrum along with Dutch banks (huge covered bond markets) but the French, Spanish, and Belgian banks are all around two times their nations GDP! Of course this assumes the asset values are 'correctly priced' and not some non-MtM dream and while they are deleveraging (which itself causes aggregate credit supply issues for the real economy and overhangs for the financial economy), LTRO has done nothing but slow the efforts in a false-sense-of-security way. We could add a bonus chart here on European bank reliance of ECB funding - that shows Italy and Spain nearing Portugal's level of aggregate reliance - not exactly a resounding success.

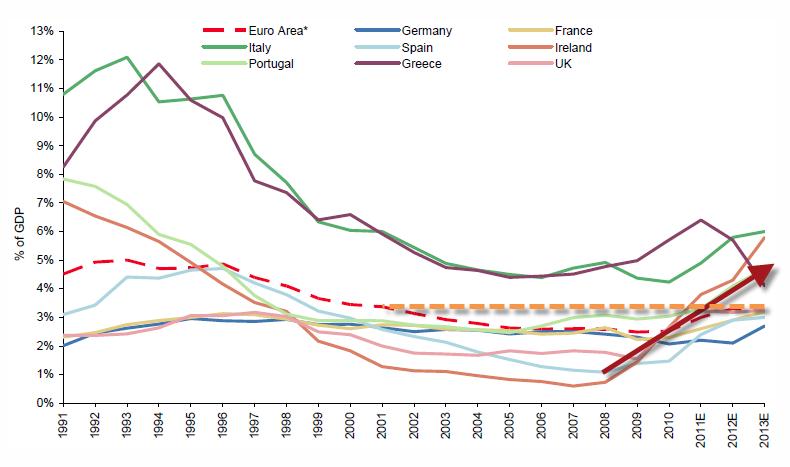

Отношение процентных платежей к производственным доходам экономики быстро растет.

Perhaps the cleanest measure of 'stress' or service-ability for the currency-using sovereigns shows that the amount European sovereigns pay in interest relative to their productive gains as an economy is rising rapidly and forecast to rise even faster. This will obviously get worse as the recession deepens from both rising costs (as post-LTRO rate normalize) and lower GDP (as austerity and balance sheet recession impacts come home to roost).

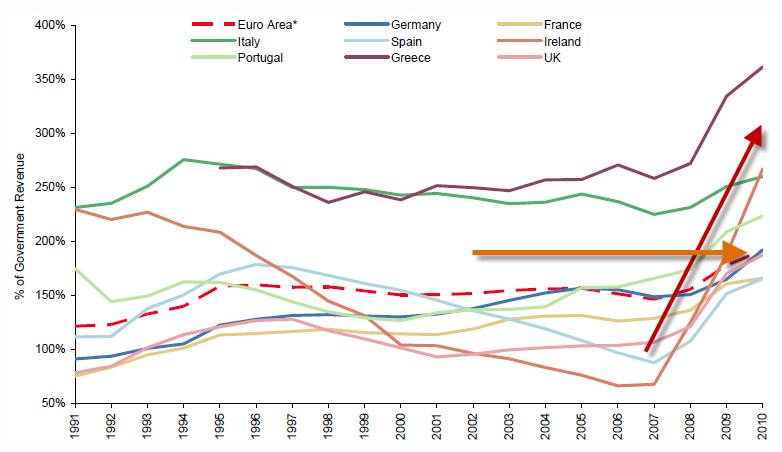

Левередж находится на 20-летних максимумах.

The 'leverage' of the Euro-Area has never been higher. Across every nation, we are at over 20 year highs in terms of this measure of leverage. To impact this via the fiscal compact by raising taxes and deleveraging at the aggregate level can only exaggerate the recessionary pressure Europeans will feel.

While yields have indeed dropped, the reflexive response that ergo - Europe is fixed - is simply nonsense as nothing has changed and in fact the concentration and contagion stress is worse than it ever was. This time may be different as this time, the ECB is really in a box to fix the next risk flare without outright money-printing and Zee Germans vill not like zat!

Новые греческие бонды драматически упали за последние два дня.

Well that didn't take long. New Greek bonds (GGB2) have dropped dramatically in the last 2 days. The 2023 bond has fallen from over EUR29.5 on Wednesday to under EUR25.5 this morning, prices have dropped an incredible 14% and down a painful 17.5% from its opening break highs of just 2 weeks ago. Yields have broken back above 20% for the first time for this new 10Y as it appears reality is sinking in that Greek Bailout III will come sooner rather than later. Eurosis is back.

So the reality is, the only banks that might buy long dated Spanish bonds are Spanish banks, and they are already pretty full of Spanish debt and even they much prefer to buy the short end. In theory, that special little subset of Spanish banks, the Caja’s, might do as they are told, but since they are already on life support, that is hardly a deep pocket investor.

Испанские банки и другие финансовые организации, и они уже под завязку загрузились испанским долгом

Banks always tended to buy 5 year and in. 10 year bond never fit banks as well as shorter dated bonds, so they were never the core buyer of this part of the curve. This desire to be in shorter maturities has been accentuated by the LTRO. LTRO encourages banks to buy 3 year and in paper for 2 reasons – i) no funding mismatch at maturity of LTRO, and ii) since LTRO is collateralized, far less risk of having to post variation margin on short duration bonds (at least until the whole curve inverts). So banks across the board have many incentives to participate in the short end which was their natural tendency to begin with. So banks as a whole do not like the long end, and foreign banks will dislike it even more. It is very hard for a non-Spanish bank to justify long term positions in Spain. There is $100 billion of debt in the Spanish system where banks issued bonds to themselves, got it guaranteed by Spain, and are using those bonds to get central bank money. As a non-Spanish bank, you have to look at that cozy relationship and be nervous. If, and when, the Spanish financials deteriorate, it is hard to expect fair treatment as a foreign bank when it is so clear that Spanish banks and the government have become very interconnected.

Иностранцам покупать долгосрочный долг Испании очень рискованно.

Officials can talk about the low debt to GDP in Spain, but professional investors have to look at all the contingent and hidden debt. Spain has implicitly and explicitly guaranteed the municipal debt. The Spanish government is in up to its eyeballs in helping the Caja’s. They have participated in the LTRO ponzi bond scheme even more than Italy has on a relative basis. These contingent liabilities will make insurance companies more reluctant, but that would still be part of the “fundamental” analysis.

There are relatively few natural buyers of Spanish long dated bonds here. Fast money is likely caught long, and it will take a potentially reluctant ECB and some already overly exposed Spanish institutions to step up and stop the slide. It may happen, but many of the policies that “bailed out” Greece created very bad precedents for bondholders, and some of those are coming home to roost, as is the understanding that LTRO ensures that banks can access liquidity, but does nothing to fix any problem at the sovereign level.

За 3 последних года публичный долг США был увеличен на 20 трлн. долларов и нет никакого быстрого роста ВВП.

In only three more years you're talking $20 trillion in public debt for the USA and a GDP going nowhere fast. Add to this that demographics are not encouraging and taxes of all sorts will have to rise. Cuts will be symbolic because the political pain will be unbearable. Without productive new investment, then debt service soon outstrips income growth and the economy enters a death spiral of declining productive investment, ever expanding debt and ever higher debt service costs.

Как он будет обслуживаться в быстроменяющейся экономической обстановке?

Опубликован Бюллетень Центрального Банка Швейцарии

We would like to note, there is a slightly optimistic tone in the report. As risks have remained marginally unchanged, the bulletin notes improvements in the financial markets and mixed developments on the global growth front. While the SNB still views the overvalued CHF as a "challenge to the economy", they mentioned "growing indications that Switzerland's economy is stabilizing." The SNB goes on to state that the minimum exchange rate has reduced volatility and allowed businesses to plan with greater certainty. "For 2012, the forecast shows an inflation rate of -0.6%. For 2013, the SNB is expecting inflation of 0.3% and for 2014, of 0.6%". While the 2012 inflation path was adjusted downwards, from Dec 2011 forecast, it still represents a trough. Heading progressively higher in Q2 2012 saying "SNB expects the CPI to move over the next three years". Interestingly, the SNB forecast assumptions are based on Brent at $110 and EURUSD at 1.29. It's looking highly unlikely that a shift in the minimal exchange rate is coming anytime soon, but this report will clearly reignite debates on the likely timing of the exit. We are currently seeing CHF appreciation against both the USD and EUR.

На следующей неделе будет обсуждаться будущее фондов EFSF и ESM

The European Commission has published a short paper outlining three options for the eurozone rescue programme, ahead of eurozone and EU finance ministers’ meetings next week.

But... Germany wants to avoid anything that requires parliamentary approval and is extremely unlikely to go with this to the Bundestag.

Which leaves option 2, in which the two funds run concurrently until mid-2013, which would make €740bn available — but only until next year. That, the EC says, might be enough to persuade the G20 etc.

Соединение слабой экономики и сильной валюты – это очень странная вещь.

The combination of a weak economy and strong currency are always suspect. But it has lasted for so long that even foreigners take it for granted. I think this is some sort of mass hysteria. Most people only remember a strong yen. On the other hand, most people haven't seen rising property or stock markets either.

Сильная йена – это психологический феномен.

Japanese culture is group-oriented. Individuals usually embrace group activities. This psyche was the reason that Japan's property bubble became so big in the 1980s. In terms of value above the normal level, Japan's bubble was five to six times the size of the bubble in the United States. After the property bubble, the group psyche shifted its power to a strong yen, pushing Japan's economy onto the path of a rising yen, deflation and rising government debt.

Japan's paralyzed political system is the reason the government has accommodated the deflation path by running up national debt. The Japanese people, on the other hand, buy the debt because deflation makes property or stocks bad investments and a strong yen discourages them from buying foreign assets and deflation.

Despite the fact Japan has had a bad economy for so long, the yen has remained strong. It reinforces the Japanese psyche on the issue. The strong yen has become a cult.

Противоречия внутри Коммунистической партии Китая, информация о которых практически все время оставалась достаточно закрытой, стали достоянием широкой общественности. ЦК Компартии приняло решение об отстранении от должности одного из самых популярных китайских политиков, члена Политбюро Центрального Комитета КПК, руководителя парторганизации города Чунцин Бо Силая.

"...We know how much money has been flowing into those bonds funds over the last three or four years. All of a sudden they might get a little nervous and say where am i going to go? Where can i get some yield and also some protection against inflation and growth? and that's when I think we're going to see people fleeing the bond market moving into stocks."

Goldman Sachs вешает лапшу на уши клиентам: прогнозирует QE3 уже в апреле

Confused why every asset class is up again today (yes, even gold), despite the pundit interpretation by the media of the FOMC statement that the Fed has halted more easing? Simple - as we said yesterday, there is $3.6 trillion more in QE coming. But while we are too humble to take credit for moving something as idiotic as the market, the fact that just today, none other than Goldman Sachs' Jan Hatzius came out, roughly at the same time as its call to buy Russell 2000, and said that the Fed would announce THE NEW QETM, as soon as next month, and as late as June.

Что нужно делать.

As for Goldman, if one ignores all of the below, the only thing to remember is that Goldman is now selling stocks to, and buying bonds from the muppets.

Вопросы и ответы: с помощью которых GS пытается своих клиентов убедить, что QE3 будет уже возможно на следующем заседании ФОМС в апреле.

Q: What is your current forecast for Fed policy?

A: It has definitely become a closer call, but we still expect another asset purchase program that involves purchases of both mortgage-backed securities and Treasuries. This would expand the Fed's balance sheet, but its impact on the monetary base would likely be "sterilized." We expect this program to be announced in the second quarter, either at the April 24-25 FOMC meeting or the June 19-20 meeting. The argument for April is that this would leave more time before the end of the long-term bond purchases under Operation Twist (more formally known as the Maturity Extension Program), and would thereby reduce the risk of market disruptions as uncertainty about the Fed's role in the market rose. The argument for June is that this would allow Fed officials a bit more time to assess the state of the economy. After June, we believe the hurdle for more action rises, not so much because of the impending presidential election but more because a decision to wait until after the end of Operation Twist would signal greater comfort on the Fed's part with denying the economy additional stimulus.

Peter Tchir of TF Market Advisors про итальянские банки и рынок госдолга

So Italian banks have issued about $100 billion of these ponzi bonds and even in this day, that is a big number.

Banks issue bonds to themselves. Then they get an Italian government guarantee. Then they take those bonds to the ECB and get money, which I assume they use to pay down other debt mostly.

The Italian banks and Italian sovereign debt markets are essentially becoming one and the same. The sovereign has added 100 billion of risk to the banks (that today no one is focused on) and the banks and ECB would have to come up with some new gimmick if the sovereign had problems.

Рынки банковского долга и суверенного долга Италии стали практически одно и то же.

These ponzi bonds ensure that Italian sovereign and bank spreads become 100% correlated over time. The fact that LTRO has daily variation margin adds to the death spiral. The fact that the ECB's outright holdings will be made senior to other holders is also an issue. I have lost track of what the EFSF or ESM are currently doing, or plan to do, but some money is being used up on the latest Greek bailouts, and the reluctance to pre-fund it, means that risk of the market rejecting EFSF or ESM bonds at times of crisis remains high.

Шансы, что рынки откажутся от бондов EFSF и ESM в момент кризиса остаются велики.

PeterTchirofTFMarketAdvisors пишет про различные сегменты рынка бондов

Without a doubt, retail has fallen in love with corporate bonds. Fund flows were originally into mutual funds, and have shifted more and more into the ETF’s. The ETF’s are gaining a greater institutional following as well – their daily trading volumes cannot be ignored, and for the high yield space, many hedgers believe it mimics their portfolio far better than the CDS indices.

The investment grade market looks extremely dangerous right now as the rationale for investing in corporate bonds – spreads are cheap – and the investment vehicles – yield based products.

И про рынок казначейских облигаций

I do not like the move in treasuries. ZIRP can hold down the short end of the curve. Operation Twist can help keep the longer end anchored and focused on the short end, but that is more difficult to accomplish. The further out the curve, the less control the Fed has. With LQD having a very long duration and trading at a premium to NAV, I think there is room for more weakness here. Investors will learn that investment grade bond investments can lose money even as spreads tighten.

В этом месяце наблюдается значительный рост волатильности юаня. Что это означает для экономики и рынков?

This month has brought signals of a subtle regime change in the People‟s Bank of China‟s (PBoC‟s) management of the external value of the Chinese yuan (CNY). We have seen a considerable upturn in the volatility of the daily PBoC fixes for USD-CNY and, more specifically, two sharp fix-to-fix CNY losses.

By and large, that China’s highly manipulated currency market is on the verge of ‘equilibrium’.

That’s to say, the country is no longer attracting enough dollar inflows to justify its long-orchestrated currency manipulation, a.k.a Treasury buying... a.k.a Chinese-led US quantitative easing.

Китай сократил покупку американского госдолга. Кто теперь будет его покупать?

As a result of the shrinking trade surplus and the need to import expensive crude, China does not have the investable dollars it once had. So it is no longer buying US Treasuries at the previous fast pace. At the same time, the US Treasury is issuing debt at the rate of $100B a month. If the Chinese aren’t buying debt, then it must be sold to other dollar holders.

The Australian dollar has long been seen as a China/commodities trade, but Macquarie’s Brian Redican reckons that’s no longer the case. The currency is increasingly influenced by external factors, rather than the country’s own ever-growing mining sector, or its monetary and fiscal policy.

And this, he says, is a momentous shift — so much so that Macquarie now sees the AUD remaining around its current levels for several years, and only gradually sliding to $1.05 by 2015. Their previous forecast was a fall below USD parity by the end of this year.

75% австралийского выпуска бондов находится за рубежом

It’s now reached the point where 75 per cent of national government bond issuance is held offshore. And yields are high against other AAA sovereign bonds: close to 4 per cent for 10-year maturities.

В дополнение темы: речь заместителя главы ЦБ Австралии

Last night we noted the very concerning rise in margin calls for European banks thanks to collateral degradation at the ECB. This story has become very popular as traders try to figure out which assets were deteriorating rapidly and which banks face immediate cash calls. One thing that came to mind for us was - what about Gold? Coincidentally or not, the last time we saw a big surge in collateral margin calls by the ECB (in September of last year), not only did Gold lease rates explode (implode) but Gold prices fell off a cliff as the squeeze came on from gold liquidity providers pushing prices down to exacerbate the negative lease rates on the gold collateral. The point here is that as margin calls come in from the ECB, we wonder whether banks will be forced to liquidate their gold (last quality collateral standing) to meet the ECB's risk standards. The key will be to watch gold lease rates (as we explained here and here) and ECB Margin calls to see if Gold is merely suffering a short-term dip from USD strength derisking or if this is a more broad based meeting of collateral desperation need that might have legs - only to be bought back later. MtM losses combined with collateral calls (as we noted earlier) was never a recipe for success and we will be watching closely

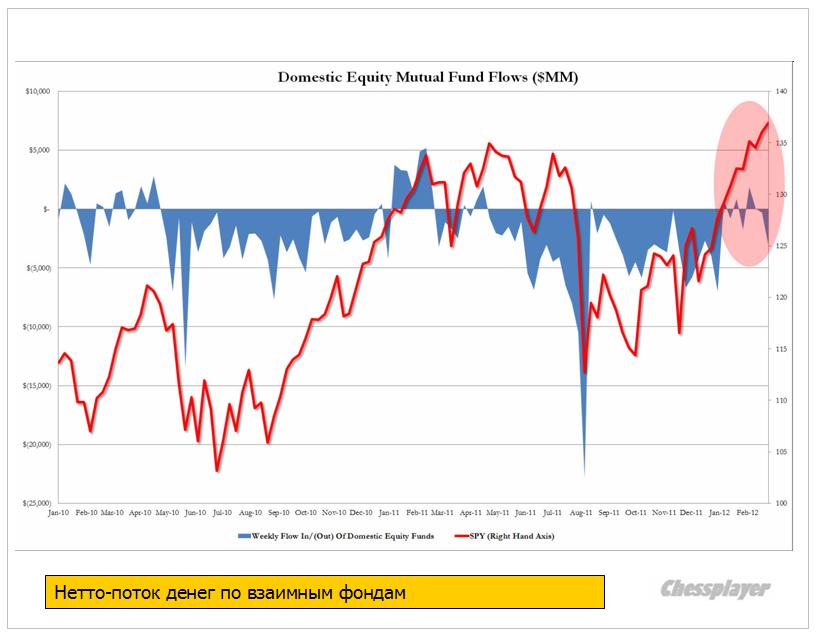

На этот раз мощное ралли с конца октября не привело к заметному притоку «глупых денег» (розничных клиентов), Мало того, они уже сейчас начали разгружаться от лонгов. Кому «умные деньги» будут сдавать свои лонги?

In what should come as no surprise to anyone who has a frontal lobe, yet will come as a total shock to the central planners of the world and their media marionettes, the latest attempt to sucker in retail investors courtesy of a completely artificial 20% stock market ramp over the past 4 months driven entirely by the global liquidity tsunami discussed extensively here in past weeks and months, has suffered a massive failure. Exhibit 1 and only: as ICI shows today, following what is now a 20% ramp in the stock market, not only have retail investors continued to pull out cash from domestic equity mutual funds (about $66 billion since the recent lows in October, the bulk of which has gone into bonds and hard commodities), but the week of February 29, when the market peaked so far in 2012, saw the biggest weekly outflow of 2012 to date, at -$3 billion. Alas, this means that the traditional happy ending for the authoritarian regime, whereby stocks get offloaded from Primary Dealers, and GETCO's subsidiaries, to the retail investor, is not coming, and soon the scramble for the exits among the so-called "smart money" will be a sight to behold.

Розничные инвесторы массово последние три года покидают рынок акций и не видно, что их могло бы остановить.

On Wall Street, risk is suddenly a four-letter word. Retail investors can't stomach it. Pension plan sponsors are allocating away from it.

That's bad news for stocks. Volume has been dropping almost nonstop for three years and shows no signs of improvement. The situation is worse than it was following the crash of 2000. It's worse than it was after the crash of 1987. Fearful of the future and still wincing from 2008, investors are moving funds into bonds, commodities, cash, private equity, hedge funds and even foreign securities-anything but U.S. stocks.

Рынки разрушены вмешательством монетарных властей и новыми технологиями.

Есть несколько причин, которые связывают высокие уровни госдолга с последующими низкими темпами роста

There are several reasons why high levels of public debt may be associated with lower growth outcomes. The first is simply that at some point debt needs to be repaid. After periods of significant debt accumulation, fiscal consolidation will usually be needed to ensure that the debt path is sustainable. As we have shown elsewhere, fiscal consolidation tends, on average, to be a drag on growth. So the price for delivering sustained tighter fiscal policy may be a period where growth is weaker.

Второй раунд количественного смягчения вынет из карманов пенсионных фондов Великобритании 90 млрд. фунтов стерлингов.

A second round of quantitative easing in the UK will leave the country's pension funds £90 billion ($141 billion) out of pocket, the National Association of Pension Funds (NAPF) announced on the third anniversary of QE in the UK.

QE hurts pension funds especially by making government bonds more expensive, forcing buyers onto more risky investments — which, due to their nature, pension funds tend to avoid.

NAPF says that an average person with a pension pot of £26,000 pounds can now expect 22 percent less income than four years ago at a loss of 440 pounds a year.

Reuters reports that Bank policy maker David Miles has argued that those about to retire should find their costs offset by a rise in their investment funds.

NAPF estimates the first round of QE cost pension funds £180 billion ($283 billion), the BBC reports.

Программы QE разрушают пенсионную систему

“Businesses running final salary pensions are being clouted by QE. Deficits that were already big now look even bigger because of its artificial distortions.

“Pension funds want a stronger economy, so they are on board with the QE project for now. But the latest bout of £125bn of money printing has blown a £90bn hole in their side. We need help in managing that. Pension funds cannot be left holding the baby.

“Firms are legally obliged to fill the deficits, and that diverts money away from jobs and investment, and will lead to further closures of final salary pensions in the private sector. Retirees trying to get a good annuity are feeling the pain too – they are getting a fifth less than they would before QE started.

“We need to see stronger action from the authorities on this massive issue, which will hurt pension schemes for some time yet. And there is always the possibility of QE3.”

Роберт Шиллер признает, что, возможно, цены на недвижимость США достигли дна.

Anyone who follows Robert Shiller closely knows that it's hard to get him to commit to calling a bottom in the housing market, which continues to see prices fall.

"I just don't see any scientific way to be assured what it's going to do," he told CNBC in an interview today. This is coming from the same economist who predicted the housing bubble in the second edition of his book Irrational Exuberance.

However, his tone seems to have turned a bit more optimistic.

"It could turn around," Shiller told CNBC's Brian Sullivan. "We're seeing some good news now. Starts, permits, confidence, the NAHB housing index is strikingly up. It's still low, but it's up."

Грядут изменения в расчете процентной ставки LIBOR

The British Bankers’ Association, the century-old lobby group that oversees the rate, last week deleted references from its website referring to its role in setting Libor. This week, it met regulators and bank executives to review the future of the benchmark. Under one option, the Bank of England’s proposed Prudential Regulation Authority would take responsibility for policing the rate, said a person with knowledge of the talks who asked to remain anonymous because discussions are private. The BBA says it isn’t seeking to cede oversight to the regulator.

Peter Tchir из TF Market Advisors акцентирует внимание на некоторых деталях, относящихся к проведенным тендерам LTRO

1. эти займы через год могут быть погашены

2.плавающая ставка

The loans have a 3 year maturity, but it seems as though the rate paid will be reset periodically in a way that should track the ECB overnight rate. That isn’t exactly how it is described, but seems to be the jist of it. With the Fed on hold until 2014 and the ECB under Draghi much more accommodative, it seems likely the rate will remain low, but it isn’t guaranteed. That puts a slight damper on the “carry trade” enthusiasts. Italian 2 year bonds yielding 1.78% aren’t that appealing, especially if the funding cost can increase.

3. От банков потребуется довносить залог в том случае, если стоимость обеспечения снизиться.

Variation Margin

Zerohedge pointed out a spike in additional collateral being posted at the ECB. According to some documents, the ECB is required to impose variation margins on its financing operations. This means that the collateral posted is not a one-time deal. If the collateral a bank has posted declines in value, the banks would have to post additional collateral. This is a big deal. Somehow the world seems to have an image that banks can borrow 3 year money at 1%, pledge an asset against it, and let the carry take effect with no other consequences. That is far from the truth if variation margins are being used.

Вот это действительно важно.

Having to post variation changes the product a lot. Buying longer dated bonds becomes very risky. They remain volatile and although banks could hold them in non mark to market books to avoid that volatility hitting their P&L, it wouldn’t save them from posting variation margin if the holdings decline in value. That helps explain why the curves are so steep, and really will limit the ability of banks to hold down longer term yields if we get another round of weakness, the death spiral risk is too scary.

Покупать долгосрочный спектр облигаций рискованно, поскольку они гораздо более волатильны. И хотя банки могут их держать за балансом, это все-равно не избавит их от нелбходимости показывать изменение вариационной маржи.

Это в какой-то степени объясняет, почему происходит уплощение кривой доходности по европейским долговым бумагам

Это может стать в какой-то момент причиной раскручивания новой долговой спирали

Portuguese banks should be of particular concern – again. The 2 year Portuguese bonds have jumped from a price in the low 80’s to the low 90’s. If banks bought these bonds as LTRO the potential for death spirals is on. As the bonds start declining in value, the banks would have to post collateral. Since the Portuguese banks are surviving almost exclusively on central bank money, their only choice would be to pledge some unpledged assets (if they have any), or sell the bonds and try and repay some of the LTRO. Selling bonds would put additional pressure on a then weak market. So the banks will pledge more assets. This does nothing to stop the slide in the underlying bonds, but would subordinate senior unsecured debt holders further. Senior unsecured debtholders will run for the hills again. They will see assets being taken out of the general pool – where they have a claim – and get shifted to the ECB, where ECB has the first rights.

Особенно уязвимыми в этом отношении являются португальские облигации.

Like anything else, once this becomes a concern in Portugal, the contagion fear is likely to raise it’s head. With €1 trillion of assets part of the LTRO program, even a 2% decline in assets pledged, would require banks to pledge 20 billion of additional collateral. Italian 2 year bonds have jumped 10 points since LTRO. Is that sustainable? Is there no risk they drift down again? Variation margin is leverage at the extreme. It creates risk to the mark to market of the underlying assets, and makes the “carry trade” option far less interesting, or more scary for any institution that has prudent risk management. Ah, yes, that explains why LTRO dependent banks and those most interested in playing the “carry” game are trading weaker than their peers – they are demonstrating that they are not prudent.

Имея активов более чем на 1 трлн. EURO (уточню - на самом деле их больше, как минимум 1,3-1,4 трлн, поскольку многие активы, особенно во время LTRO-2 принимались с дисконтом), даже снижение их стоимости на 2% повлечет за собой изъятие у банков 20 млрд. EURO.

Таким образом ликвидность в еврозоне стала очень чувствительна к доходности долговых бумаг долгосрочного спектра.

случае уменьшения стоимости банки должны увеличивать залог под взятые кредиты.

This 'Deposits Related to Margin Calls' line item on the ECB's balance sheet will likely now become the most-watched 'indicator' of stress as we note the dramatic acceleration from an average well under EUR200 million to well over EUR17 billion since the LTRO began. The rapid deterioration in collateral asset quality is extremely worrisome (GGBs? European financial sub debt? Papandreou's Kebab Shop unsecured 2nd lien notes?) as it forces the banks who took the collateralized loans to come up with more 'precious' cash or assets(unwind existing profitable trades such as sovereign carry, delever further by selling assets, or subordinate more of the capital structure via pledging more assets - to cover these collateral shortfalls) or pay-down the loan in part. This could very quickly become a self-fulfilling vicious circle - especially given the leverage in both the ECB and the already-insolvent banks that took LTRO loans that now back the main Italian, Spanish, and Portuguese sovereign bond markets.

Теперь строка «'Deposits Related to Margin Calls' в еженедельном стейтменте приобретает особое значение.

What should also start to worry the Germans is the fact a 37x levered hedge-fund central bank with EUR3 trillion balance sheet that has extended credit in a 'risk-managed' approach on what appears to be an ever dwindling supply of performing collateral is starting to see dramatic 'gaps' in its asset-liability exposure (but rest assured Bernanke told us that our FX Swaps are safe as houses).

А каковы перспективы LTRO3?

One last point should be noted - the hopes of an LTRO3 or some such are surely now out of the window as clearly banks have run dry of any and all reasonable collateral or can the sovereign bonds purchased using LTRO1 and LTRO2 funds be lodged once again in a rehypothecated miasma circling the drain?

Очень проблематично, в т.ч. и потому, что банки уже исчерпали все стоящие залоги

Большая статья Peter Tchir о перипетиях переговоров по греческому долгу.

The situation in Greece should create some big headlines this week. The bond exchange “invitation” is set to expire at 3pm EST on Thursday March 8th. This is the so-called Private Sector Involvement or PSI. Greece has other steps to take during the week, and ultimately the Troika will determine how to proceed with the bailout, but not until the results of the PSI are known.

What a no-brainer to suck at the teat and go long some very transparent and liquid debt that matures in less than three years (how can there not be a rally in global risk assets when Europe's central bank pumps a combined $1.3 trillion into the financial system? Not to mention a second bailout for Greece we were told a year ago there wouldn't be any!). This must be the safest carry trade ever, or at least that is the perception (1% LTRO loan for a 5% Italian bond or a 2% short-term note even ... back up the truck!). Put up a tiny bit of capital and lever it up. It is incredible that we live in a world where the difference between going out of business as a bank and prosperity lies with cheap money being accessed from the central bank balance sheet.

Если LTRO-1 еще можно рассматривать как способ уберечь систему от разрушения, то LTRO-2 означает переход от роли кредитора в последней инстанции к роли «кредитора по первому вызову», как это назвал Peter Tchir.

At least LTRO1 was dealing with a possible breakdown of the system since the banks weren't lending to each other. LTRO2 is clearly an overt policy move from the traditional central bank role of being the lender of last resort (which even LTRO1 was to a point) to being the lender of first call, as Peter Tchir aptly puts it. There is no such thing as a free lunch, but there is such a thing as the law of unintended consequences. I can't say I know for sure what they will be or when they will show up, but there are going to be repercussions from a central bank morphing from a bona fide lender of last resort to a gift-giving institution.

ЕЦБ движется от роли традиционного центрального банка к роли учреждения, осуществляющего квазибюджетную политику.

Somehow a long gold, short euro barbell looks really good here. Bernanke, after all, now seems reluctant to embark on QE3 barring a renewed economic turndown while the ECB is moving further away from the role of a traditional central bank to take on the role of quasi fiscal policymaking, The German central bank, after all, is responsible for 25% of any losses that would ever be incurred by the massive Draghi balance sheet expansion. Why would anyone want to be long a currency representing a region with a 10.7% unemployment rate, rising inflation rates and free money? Mind you — the same can be said for the US (where U-6 jobless rate is even higher), which is why the best currency may be physical gold (or the producers that trade very inexpensively here and you pickup some leverage).

Дэвид Розенберг предлагает входить в лонг по золоту и шорт по EURO.

ISDA Determinations Committee Accepts Question Related to a Potential Hellenic Republic Credit Event

LONDON, February 28, 2012 – The International Swaps and Derivatives Association, Inc. (ISDA), as secretary to the Determinations Committees (the DCs), today announced that a question relating to a potential credit event with respect to the Hellenic Republic has been submitted to, and subsequently accepted for consideration by, the EMEA Determinations Committee.

Заседание ISDA состоится 1 марта в 15.00 мск

In accordance with the Determinations Committee Rules, a meeting will be held at 11AM GMT on Thursday, March 1 to determine whether a credit event has occurred.

Further information regarding the question is available at www.isda.org/credit.

Поддерживать Грецию Германии становится все труднее

Chancellor Merkel failed to get her Chancellor Majority (310 votes in 620 member chamber) but did secure the passing of the EFSF with 305 votes.

Commentators are now busy talking about how she is increasingly finding it hard to negotiate with the Parliament and deal with overall German public opinion. There are several reasons for this:

She and her government told Parliament last year that Germany would be on the hook for a maximum EUR 211 billion. Now fast forward to today and the IMF is insisting that that EU increase the fire-power of bailout mechanisms to 700-750 bln. EUR.

This would mean the German contribution will rise to above 300 bln. EUR - in itself a problem politically (as she promised 211 was the absolute max) but add to this that the German Constitutional Court has already told the Parliament that any support for bailouts in excess of the current German budget (306 bln. in 2012) is risky and destablising. Get the picture? Indeed, the EU Summit this week will be interesting. It seems to me that Merkel will be forced to dig-in her heels on this issue and this will consequently risk the PSI deal and Greece in the process. The stakes are clearly rising.

Citigroup's Buiter put it very elegantly in his Global economic View (27. February 2012 - Why does the ECB not put its mouth where its money is? The ECB as lender of last resort for Euro area sovereign and banks):

'EU policy makers prefer support to fiscally weak Euro Area sovereigns under attack by markets to be provided through the ECB, since that support is off-budget and off-balance sheet, unlike the contributions to the EFSF, ESM'.

This is the key political driver! There is no budget, no balance sheet impact from having Draghi pretend he is the great saviour of everything European (read: banks) but if the ESM, EFSF should need additional capital, then there will need to be a vote - heaven forbid!

The divergence is in the accountability. The ECB is already violating its mandate and the Treaty but they are not up for vote or even accountability so far, hence they will fold their cards first in this game of poker and have done so, again, again and again.

Через ЕЦБ по ряду причин делать это гораздо сподручнее

S&P downgraded Greece to Selective Default (SD) from ‘CC’. S&P said that the downgrade followed the Greek government's retroactive insertion of collective action clauses (CACs). However, if the debt exchange is completed as expected, S&P will raise Greece’s credit rating to ‘CCC’. (RTRS)

-S&P have said they believe Greece would face imminent outright payment default if an insufficient number of bondholders accept the exchange offer.

The EFSF outlook was changed to negative from developing by S&P; 'AA+' ratings affirmed. (RTRS) S&P concluded that credit enhancements sufficient to offset what they view as the reduced creditworthiness of EFSF guarantors are not likely to be forthcoming. The negative outlook on the long-term rating also mirrors the negative outlooks of France and Austria.

The is to make a decision on Greece CDS triggers by 1700 GMT, Wednesday February 29. (FT Alphaville-More) The ISDA announced that a question relating to the Hellenic Republic has been submitted to the EMEA Determinations Committee. The ISDA will decide whether to accept the question for deliberation or reject it.

The ECB have temporarily suspended the use of Greek debt as collateral, reflecting the Greek debt ratings in the light of the PSI agreements. (Sources)

Standard & Poor’s Managing Director Kraemer has commented that the outlook on the Eurozone remains negative, adding that the ECB’s LTRO is not a substitute for reforms, but it does help in the immediate term. (Sources)

The ECB’s Nowotny has said there is no need for ECB’s key interest rate to move below 1% at the moment, adding that the ECB is concerned about the long-term effects of loans. (Sources)

Очень выборочно:

ЕЦБ приостановил принимать облигации Греции в качестве залога.

Важно: ISDA будет принимать решение по поводу контрактов CDS by 1700 GMT, Wednesday February 29 – в среду в 21.00 по Москве

LONDON, February 27, 2012 – The International Swaps and Derivatives Association, Inc. (ISDA), as secretary to the Determinations Committees (the DCs), today announced that a question relating to the Hellenic Republic has been submitted to the EMEA Determinations Committee.

In accordance with the Determinations Committee process, the EMEA Determinations Committee will decide whether to accept the question for deliberation or reject it and this decision will be made by 5PM GMT on Wednesday, February 29, 2012.

В среду пока лишь будет решаться вопрос, принимать ли этот вопрос к рассмотрению.

Суть вопроса:

Does the announcement of the passage by the Greek parliament of legislation that approves the implementation of an exchange offer and vote providing for collective action clauses (“CACs”) that impose a “haircut amounting to 53.5%” (MINFIN Announcement, 2.21.2012) that “shall bind the entirety of the Bondholders [of eligible instruments]” (First Article, Section 9), constitute a Restructuring Credit Event in accordance with Section 4.7 of the 2003 ISDA Credit Derivatives Definitions (as amended by the 2009 ISDA Credit Derivatives Determinations Committees, Auction Settlement and Restructuring Supplement to the 2003 ISDA Credit Derivatives Definitions, published on July 14, 2009) because (i) the European Central Bank and National Central Banks benefitted from “a change in the ranking in priority of payment” as a result of the Hellenic Republic exclusively offering them the ability to exchange out of their “eligible instruments” prior to the exchange and implementation of the CACs, thereby effectively “causing the Subordination” of all remaining holders of eligible instruments, and (ii) this announcement results directly or indirectly from a deterioration in the creditworthiness or financial condition of the Hellenic Republic?

As for what the final size of the LTRO will be, just ask your hotdog vendor: he has as much guidance as anyone else. Regardless of the size outcome, one thing is certain - the banks that are found to use the ECB's Discount Window should prepare for major stock pain, as the market, devoid of easy targets, focuses on them next as the European stigma trade becomes the hedge fund divergence trade du jour. After all there is a reason why the Fed's Discount Window expansion lasted for all of 3 months, and ended up hurting the participating banks (ahem Dexia) more than any other Fed concoction during the early stages of the Depression.

Дисконтное окно Феда просуществовало всего 3 месяца, поскольку пользование им для банков имело слишком сильные репутационные издержки. Вот и на этот раз, те, кто в полной мере воспользуется предлагаемым ЕЦБ LTRO, рискуют надолго получить черную метку и проблемы на межбанке...

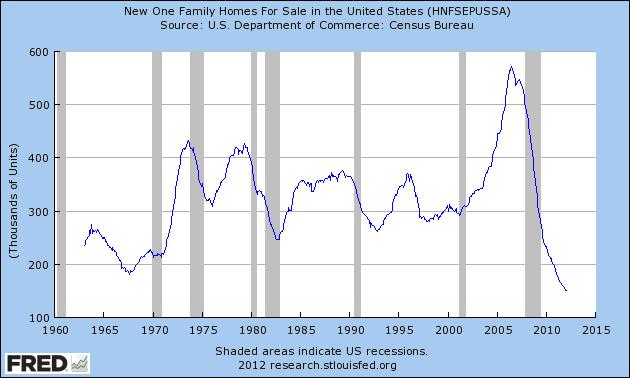

Case Shiller продемонстрировал 8-й подряд месяц снижения цен на дома.

The December Case Shiller came, saw, and shut up all those who keep calling for a home price recovery. The Index printed at 136.71 on expectations of 137.11, with the prior revised to 138.24. The top 20 City composite was down -0.5% on expectations of a 0.35% drop. 18 out of 20 MSAs saw monthly declines in December over November, with just the worst of the worst - Miami and Phoenix - posting a dead cat bounce, rising 0.2% and 0.8% respectively. And granted the data is delayed, but the fact that we have now had 8 consecutive months of home price declines even with mortgage rates persistently at record lows, and the double dip in housing more than obvious, can we finally shut up about a housing bottom? Because as Case Shiller's David Blitzer says: "If anything it looks like we might have reentered a period of decline as we begin 2012.

Двойное дно по рынку недвижимости более, чем очевидно и пока не видно признаков, что рынок начинает выбираться из этого дна.

То, что цифры соответствуют текущей обстановке, уже никого не удивляет.

Начинается переход к режиму QE3 –экономического разочарования, - язвительно замечает Zero Hedge.

После LTRO от ЕЦБ следующая очередь за Федом .

And so the transition to the QE3 "economic disappointment" regime begins. Because after the ECB is done with the LTRO it's over for global QEasing, and the Fed is next. Remember- Bernanke's semiannual testimony to Congress is tomorrow. Whatever will he say....

Headline Durable Goods plunges from +3.2 to -4% on expectations of -1%

More painfully, Durable goods non-defense ex aircraft down a whopping -4.5% on Exp of -1.3%, down from +3.4%.

Visually, this is the lowest Durable Goods number since January 2009

Дефолт Греции можно считать почти состоявшимся. Но никакого волнения не ощущается. До 20 марта мы скорее увидим кредитное событие и срабатывание CAC

So far there are no dramatic consequences of the Greek default. The ECB did say they couldn’t accept it as collateral, but national central banks (including Greece’s somehow solvent NCB) can, so no real change. We will likely get a Credit Event prior to March 20th once CAC’s are used to get the deal fully done. Will the market respond much to that? Probably not, though there is a higher risk of unforeseen consequences from that, than there was from the S&P downgrade. It just strikes us that Europe wasted a year or more, and has created a less stable system than it had before. Tomorrow’s LTRO is definitely interesting. It seems like every outcome is now bullish – big take up is bullish because of the “carry” trade. Low take up is bullish because “banks are okay”. Any weak bank looking to borrow from the LTRO to buy sovereign debt would be insane to buy bonds longer than 3 years and take the roll risk, but on the other hand, the weakest and most insolvent, got there by doing insane things in the first place.

Любой исход завтрашнего LTRO будет позитивен для рынков.

Большой спрос – позитивен из-за кэрритрейда. Маленький спрос – потому-что у банков все ок.

Последнее ралли – это какое-то непрекращающееся шоу под названием «День сурка». Рынок отыгрывает вновь и вновь по много раз одно и то же событие. Но когда-то эта магия должна закончиться!

Когда в Москве уже была глубокая ночь, с евросаммита из Брюсселя поступило, наконец, сообщение о завершении переговоров и заключении соглашения. Прессконференция несколько раз переносилась на час из-за затягивания саммита.

На объявлении результатов евросаммита последовал очередной импульс вверх: американский фьючерс S&P500 и евро обновили максимумы. Евро сумел пробить барьер 1,40, американский фьюч очень сильно плюсует.

Таким образом объявлено о QE еврозоны, или точнее TARP еврозоны ( TARP – американская программа помощи банкам в 2008 году). Всего 1 трлн. евро, хотя, помнится, Гардиан нам предсказывала 2 трлн (одна из рыночных манипуляций последнего времени).

Размер списания по долгам частным кредиторам – или как это называют – участие частных инвесторов - будет 50%.

Судя по всему, многие детали важного заключенного соглашения станут известны только к встрече двадцатки в Каннах или даже позже. До этого момента участники рынка будут в неведении.

Не вызовет ли это хаос на европейском долговом рынке?

Все это уже неоднократно отыграно рынками и заложено в цены. Напомню, что текущий уровень S&P500, если исходить из американского фьючерса, является рекордным месячным ростом за последние 11 лет. Об этом было здесь:

Индекс S&P500 сейчас показывает рекордный месячный рост

Индекс S&P500 сейчас опять подошел к этим уровням.

Рост в ноябре может быть и продолжится, хотя я очень в этом не уверен. Но какой-то фикс после такого мощного ралли должен все-таки состоятся.

На то, чтобы исправить это «недоразумение», а я полагаю, что оно будет исправлено, остается всего 3 дня.

Таким образом, мы имеем списание части долга – по сути дефолт Греции.

Как я и писал больше месяца назад: что дефолт Греции произойдет в период 15 октября – 15 ноября.

Дефолт необычный: не со всех кредиторов списываются займы. Известно, что не списывается с ЕЦБ. Может быть появятся еще какие-то кредиторы, с кого не будут списываться займы. Например, греческий пенсионный фонд.

Это может послужить «кредитным событием» и вызвать срабатывание CDS. Пока неясно, произойдет это или нет нет. Это зависит от регулирующей этот рынок ISDA.

Peter Tchir из TF Markets Advisors считает, что это не станет «кредитным событием». Поскольку не подпадает под юридическое определение «кредитного события» в ISDA документации.

В то же время банк Barclays, который входит в комитет ISDA, считает, что это вызовет «кредитное событие».

Другое последствие: примеру Греции могут последовать Ирландия, Португалия, Испания и Италия. Они тоже могут попросить списать часть своего долга. Создан опасный прецедент.

Осталось много вопросов и деталей, на которые пока нет ответов.

Согласились ли банки на 50% списание греческих долгов?

Непонятно, какое влияние это окажет на весь европейский рынок суверенных долгов.

Интересно, направят ли банки деньги из полученной сегодня 12-месячной кредитной линии на покупку европейских облигаций.

Есть еще много вопросов. Будут ли все банки в этом участвовать? Коснется ли списание бондов, находящихся в распоряжении греческого пенсионного фонда. Будут ли после списания 50% греческого долга покупать греческие бумаги?

Индикаторы

Евро

Интересное совпадение: значение 1,40 по EUROUSD сейчас соответствует в точности 200-дневной скользящей средней по индексу доллара. Совпадение двух очень важных уровней.

Многие активы вышли к важным уровням сопротивления. Индекс Dow тоже находится вблизи 200-дневной средней скользящей. AUDUSD торгуется большую часть последние 4 сессии выше 200-дневной MA, хотя и закрывался там лишь один раз.

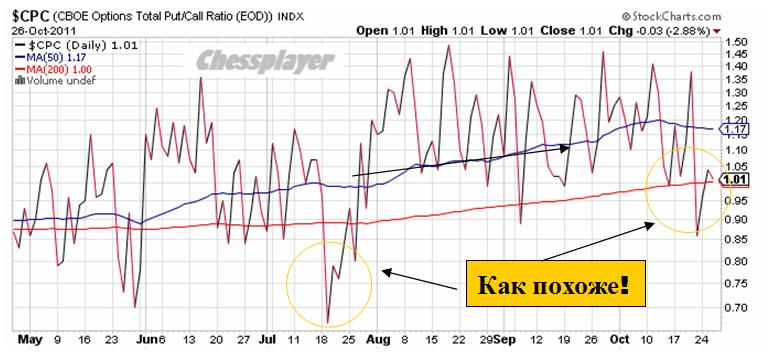

Put/call коэффициент

Даю рисунок без комментариев

Краткие выводы:

Неопределенность условий заключенного соглашения создает очень нервозную обстановку на рынке. Поэтому торговля будет оставаться очень волатильной.

Однако, на мой взгляд, в ближайшие дни, по крайней мере до конца месяца, будет определенный уклон вниз.

Вряд ли подробности сделки, которые будут постепенно раскрываться, окажутся столь позитивны, что улучшат ее восприятие в глазах рынка.

Поэтому не исключено, что сегодня мы получим максимумы рынка на достаточно длительную перспективу.

Неожиданно появился новый претендент на то, чтобы повторить судьбу Lehman Brothers.

Morgan Stanley (MS), который владеет крупнейшим в мире ритейлерским брокерским бизнесом, оценивается с точки зрения CDS как менее кредитоспособный, чем многие банки США и Европы и хуже с этой точки зрения чем BAC и даже злополучный SocGen.

На графике внизу показаны CDS MS вместе с CDS SocGen, Франции и Китая. CDS SocGen заметно снизились за последние 2 недели. Зато рост CDS MS почти совпадает с ростом CDS Китая.

По-видимому, какие-то проблемы с вложениями MS в Китае.

В последнее время очень много разговоров по поводу единых европейских облигаций. Эта тема сейчас стала камнем преткновения между Францией и Германией. Германия категорически возражает против их выпуска до того момента, пока все страны в еврозоне будут вести единую бюджетную политику. На мой взгляд, это в принципе невозможно.

Как–то я обещал остановиться на этой теме подробнее. Что сейчас и сделаю.

Здесь есть три важных вопроса:

1) какова будет процентная доходность этих бондов

2) как они будут рейтинговаться.

Но самый важный третий вопрос: каковы будут гарантии по этим бондам?

Многие суверенные эмитенты долга способны увеличивать свои долговые обязательства, поскольку они гарантируют выплату из налогов, которые они соберут в будущем.

По крайней мере, так оно работает в теории. Что касается эмитента единых европейских облигаций, то непонятно: какие будущие поступления гарантируют его обязательства?

Юридическое лицо, выпускающее евробонды, гарантирует их лишь трансферными платежами или гарантиями стран-участниц.

Если эмитент евробондов будет работать по принципам EFSF, в котором вклад зависит от уровня рейтинга, и гарантиями главным образом являются обязательства ААА-стран, то из главных гарантов в скором времени может остаться одна Германия.

Одно дело, когда нужно гарантировать 275 млрд. евро. Тяжелее получить согласие гарантировать 440 млрд.евро. Совсем страшно для Германии должно быть дать согласие гарантировать 600 млрд. евро, 1 трлн. евро и т.д.

Всех нужно спасать. А спасать кроме Германии некому.

Другой важный вопрос: как будет осуществляться фондирование фонда единых еврооблигаций и на каких условиях.

Peter Tchir из TF Market Advisors обращает внимание на следующий момент. Страны, имеющие более низкие уровни доходности по облигациям, фактически будут субсидировать участников, имеющих более высокие уровни доходности суверенных облигаций.

Решение о выпуске евробондов хорошо выглядит на бумаге, но его трудно исполнить в реальности. Возникающие из-за появляющихся на эту тему сообщений ралли быстро затухают.

Риск, который берут на себя ведущие страны еврозоны , продолжит расти и может выйти из под контроля.

Для Франции, хотя она выступает за создание евробондов, это тоже чревато, когда ее растущий госдолг приведет к понижению суверенного рейтинга.

Последние переговоры между Меркель и Саркози показали, что имеется еще много нерешенных вопросов относительно единых европейских облигаций.

Саркози после этой встречи сказал: Единые европейские облигации можно представить однажды, но случиться это в конце европейского процесса интеграции, а не в начале. Оба лидера стран, и Меркель и Саркози, считают, что фонда EFSF вполне достаточно, чтобы защитить евро.

Так что тема выпуска единых европейских бондов скорее всего продолжит оставаться лишь идеей.