LINKS-ДАЙДЖЕСТ 27.02.2012

SocGen о предстоящем LTRO

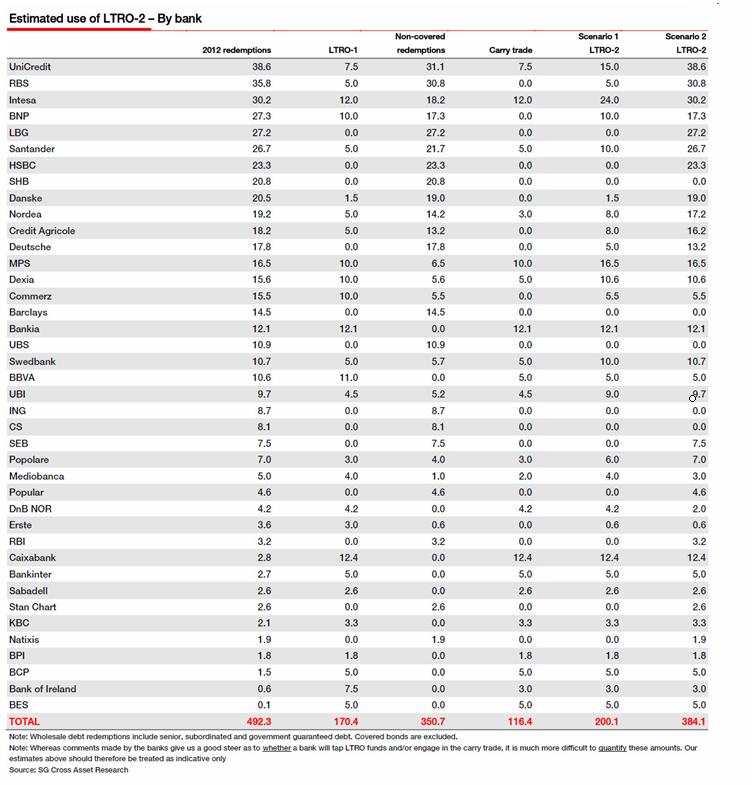

SocGen provides a comprehensive top-down analysis of the drivers of LTRO demand, the likely uses of those funds, and estimates how much of this will be used to finance the carry trade (placebo or no placebo). Italian (25%) and Spanish (20%) banks are unsurprisingly at the forefront in their take-up of ECB liquidity (likely undertaking the M.A.D. reach-around carry trade ) and have been since long before the first LTRO. On the other side, German banks have dramatically reduced their collective share of ECB liquidity from 30% to only 6%. SocGen skews their detailed forecast to EUR300-400bn, disappointing relative to the near EUR500bn consensus - and so likely modestly bad news for risk assets. Furthermore, they expect around EUR116bn of this to be used for carry trade 'revenue' production which will however lead to only a 0.6% improvement in sectoral equity levels (though some banks will benefit more than others), as they discuss the misunderstanding of LTRO-to-ECB-deposit facility rotation. We, however, remind readers that collateralized (and self-subordinating) debt is not a substitute for capital and if the ECB adamantly defines this as the last enhanced LTRO (until the next one of course) then European banks face an uphill battle without that crutch - whether or not they even have collateral to post. Its further important to note that LTRO 2 cannot be wholly disentangled from the March 1-2 EU Summit event risk and we fear expectations, priced into markets, are a little excessive.

[ZH: What we do note is that this is unlikely to be a Goldilocks moment. Too small an uptake, as SocGen expects will lead to risk-off and disappoint markets. Too large an uptake, in our view, will also shock the market - the greater stigma and rising subordination of assets via collateralization will hurt senior unsecured credit and implicitly cost of funding medium-term (shutting private funding channels and increasing public funding dependencies) - leading to risk off. Unless we see EUR475-EUR525bn - just right - then we suspect we will see risk-off either way.]

LTRO 2 102: Projected LTRO Take Up By Bank

Запросы банков на предстоящий LTRO №2

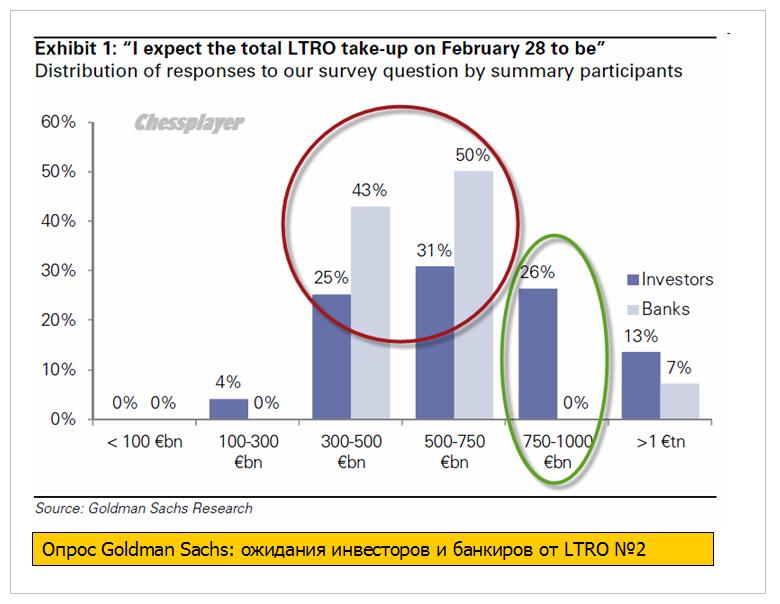

Here Is Why Someone Will Be Disappointed By The LTRO

Gaming out the impact of this week's LTRO2 demand on global risk assets is complicated by the ability of banks to mobilize collateral (how much can they pledge to the ECB and how much of that will be 'optimal' given the implicit subordination of senior unsecured debt holders), the use of those funds (carry trade economics are considerably lower and refinancing needs remain high), and the market's expectations (just how much more back-door QE is priced into European - and for that matter - US asset prices). Goldman Sachs surveyed its clients and found a gaping divide between banks and investors with the latter expecting considerably more than the banks - it seems someone will be disappointed - investors hope for more and banks expect to do less.

Ожидания банкиров и инвесторов относительно размера предстоящего LTRO №»2 разительно отличаются. Банкиры ждут гораздо меньшего: по-видимому они гораздо лучше осведомлены о способности банков предоставить подходящий залог.

"Дешевые деньги" ЕЦБ: соблазн велик, риски несущественны?

Банк Англии может продолжить стимулирование

Банк Англии может еще расширить программу выкупа активов, размер которой сейчас составляет 325 млрд фунтов, заявил председатель комитета по монетарной политике Пол Фишер.

"В этом вопросе необходимо сохранять не зашоренный взгляд на вещи, что мы и делаем. Скорее всего, мы подождем до мая, когда мы подготовим новый экономический прогноз, и, основываясь на нем, примем соответствующее решение. Мы можем в будущем столкнуться с любыми сюрпризами, как положительными, так и с негативными", - заявил он в интервью телеканалу Sky News.

Overnight Sentiment Negative Following Failure To Boost IMF Rescue Fund

Двадцатка министров финансов отказалась увеличивать фонды МВФ.

And below are some of the key excerpts from the G-20 communique (source)

We are reviewing options, as requested by leaders, to ensure resources for the IMF could be mobilized in a timely manner. We reaffirmed our commitment that the IMF should remain a quota-based institution and agreed that a feasible way to increase IMF resources in the short-run is through bilateral borrowing and note purchase agreements with a broad range of IMF members. These resources will be available for the whole membership of the IMF, and not earmarked for any particular region. Adequate risk mitigation features and conditionality would apply, as approved by the IMF Board. Progress on this strategy will be reviewed at the next ministerial meeting in April. Other options mentioned by leaders in Cannes such as SDRs are under review."

Очень обтекаемо...

Автор статьи Peter Tchir сравнивает последние меры по лечению европейского долгового кризиса с таблетками с эффектом плацебо.

Пациенту временно становится лучше, но эффект очень кратковременен и реального лечения болезни нет.

Making it even more difficult to determine if a policy is working is the “placebo” effect. The market is being fed a lot of medicine (pun intended). LTRO and Greek “resolution” being the latest medicines. But are these treatments really working or are we rallying on a diet of pablum?

The LTRO was designed to support the market, the market is up, so the LTRO must be working. That at least is the logic many investors are applying. They see the improvement in sovereign debt yields, the avalanche of “positive” (if unfounded) headlines, and the relentless march higher of the stock market. So the plan is working? Not so fast. The treatment was designed to help the stock market. The stock market is encouraged by that and believes it is getting better. That price action in turn convinces more people that things are better or fixed, and creates further demand for stocks. But is it real or are we just in another “Placebo Effect” stock market rally? The problem with the patients who get better on the placebo, is that the effect tends to be short-lived since nothing is actually fixed.

Live Blogging The Second Greek Bailout At The German Bundestag